-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

HEC Pharm (1558.HK) - Oseltamivir May Become the Heavyweight Variety

Monday, August 8, 2016  13635

13635

HEC Pharm(1558)

| Recommendation | Buy |

| Price on Recommendation Date | $17.060 |

| Target Price | $23.700 |

Weekly Special - 2333 Great Wall Motor

Expecting a 35%+ Growth in 1H16

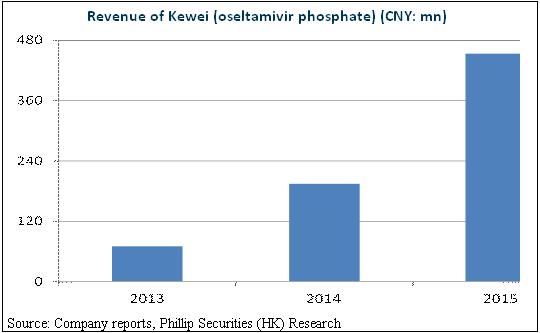

HEC Pharm (1558-HK) recently made a positive announcement. It is estimated that the company will see a no lower than 35% growth in net profit in the first half of the year mainly due to a surge of sales volume of the flagship product Oseltamivir Phosphate (Kewei) and the continuing improvement of marketing and promoting ability of the company on professional academics.

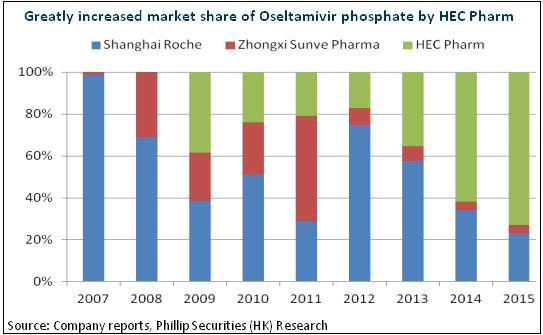

The company mainly engages in the drug production and sales of antiviral, endocrine and metabolic diseases and cardiovascular diseases. Among them, the star is Kewei that, with double growth in each of previous years, contributes 65.5% of the business revenues in 2015. What's worth mentioning is that, HEC Pharm is currently the only licensed company to produce and sell active pharmaceutical ingredients (API), granules and capsules of Oseltamivir. Specifically, Oseltamivir Phosphate Granules is the exclusive product in Chinese pediatric drug market. This exclusive license has made the company the leading enterprise in selling Oseltamivir since 2013. In 2016, the academic promotion and sales team of the company was enlarged to more than 300 people, comparing 196 people in 2015, which supported Oseltamivir to enter the markets of more provinces.

Oseltamivir May Become the Heavyweight Variety

We maintain a positive attitude towards the growth of Kewei, expecting it to be a one-billion class brand. First of all, the capacity of the market of anti-influenza virus drug is approximately RMB4 billion at present, with Amantadine occupying the major part. However, more than 90% of the population will have drug tolerance while Oseltamivir will bring about lower drug tolerance. Thus we expect it to dominate the market gradually. Secondly, there is little side effect of Oseltamivir Phosphate and it could fit in the pediatric drug market and suitable for pregnant women. Owing to its outstanding safety, FDA permitted its use to 2-week old babies. At present, the two-child policy is completely implemented in mainland China.

The speed increase will be as high as 30% in pediatric drug market. What's more, there are only 3 manufacturers producing Oseltamivir in China, which indicates a bright future for the company in the competition landscape. In addition, except HEC Pharm, the other two manufacturers do not take Oseltamivir as their major brand. Therefore, it is likely that HEC Pharm will dominate the field and face a limited competition in the following 3 to 5 years.

R&D Advantage Supports Medium and Long Term Development

According to the strategic cooperation agreement with the controlling shareholder Shenzhen HEC Corporation, the company will gain the preemptive right of the products of HEC Pharm R&D Group. The research team of HEC consists of 1200 researchers, including 4 experts from the Thousand Talents Program of China. Therefore, the R&D system is outside the company but good brands could be brought in the listed company and provide support to the medium and long term development.

At present, there are two premier brands in research worthy of attention in HEC Pharm. First of all, insulin products are under clinical development. It is expected that Gen 2 insulin and recombinant human insulin will successively come to the market in the year 2017 to 2018 and Gen 3 insulin will be present in 2019 to 2020. Due to high technical barrier, there are fewer competitors in the insulin market. Except the traditional international Big Three, only Gan Lee Pharm is approved to produce Gen 3 insulin in China. Dongbao Pharm is the leading manufacturer of Gen 2 insulin. The overall competition landscape is positive. Additionally, the hepatitis C drugs of the company are expected to come to the market at the fastest speed compared to similar products in the year 2019 to 2020.

Valuation

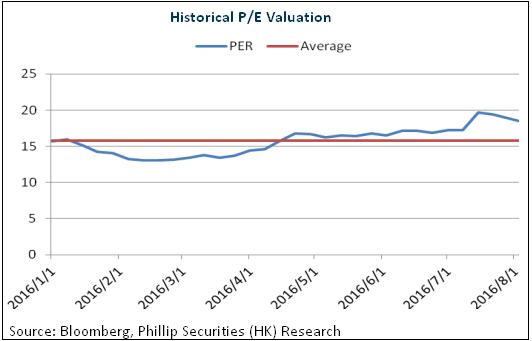

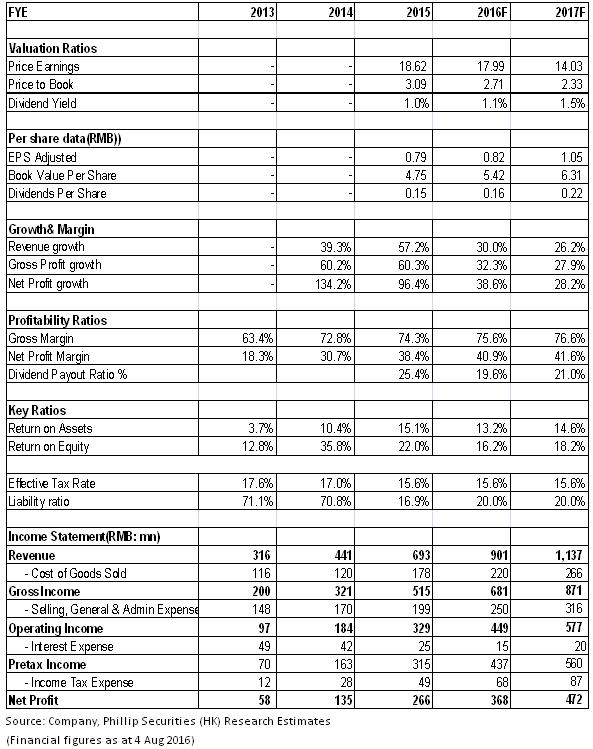

The sales of Kewei increases in main provinces and is expected to be the major driver of the rapid growth in 2016 to 2018 of the company. It is hopeful to reach the scale of one billion in the future. The R&D support to the group and good product pipeline will support the medium and long term development of the company. We give an estimation of 25x EPS in 2016 and the target price is HKD23.7, with the "Buy" rating initially. (Closing price as at 4 Aug 2016)

Risks

Risk of price drop in drugs;

Risk of R&D of new drugs.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()