-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Vitasoy (345.HK) - Continuing expanding production capacity and channels in China market, double-digit growth is expected for the next three to five years

Wednesday, March 20, 2019  21557

21557

Vitasoy(345)

| Recommendation | Accumulate |

| Price on Recommendation Date | $35.950 |

| Target Price | $38.500 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Revenue increased 22% to HK$4448million, compared to 23% of last year's growth. As the main contributor to the company, revenue of Vitasoy China increased 33%, whereas Hong Kong Operation increased 4%. Vitasoy China experienced strong growth in recently years, we believe the reasons behind include the recognition of its soya milk and lemon tea products has been improved. At the same time, deepening of the sales channels in South China market, and the opening up of new markets.

According to the management team, compared to lemon tea products, more resources will be invested in the soya milk business, as the market base of the latter is small and thus the growth is relatively fast. Currently, the market size of soya milk in China is one tenth of the tea beverage market. The company relaunched its premium high nutrition VITASOY Health Plus range, which target high-end market and differentiated from the main competitors Yili and Mengniu. The company also intends to continue to develop in the middle and high-end market in the future.

In fact, in the more mature Hong Kong market, the annual intake of soy milk is 12 kilograms per person, which is only 1 kilogram in China, reflecting the huge room of development. Vitasoy currently owns and runs four production plants in China, and the production capacity has reached 100%. The company has kept upgrading the machinery every year to improve production efficiency. It also plans to build 20 new production lines in Dongguan, and expects to go into operation in 2021.

With the capacity expansion, improvements of channels and branding, we expect that the Vitasoy's China business and overall revenue to maintain mid-teens growth in the next three to five years, which will be mainly driven by sales volume. If raw material costs can maintain stable and the gross profit margin can also be further improved. At the same time, Hong Kong business is expected to maintain relatively stable growth due to its maturity.

Vitasoy currently ranks first in the soya milk market in Hong Kong, with a market share of 70% and lemon tea with 30%. In the first half of the fiscal year, its China business accounted for 67% of total revenue, this figure is expected to increase further in the future.

In the short term, considering the large base in the same period last year, we expect the growth of overall revenue and China business in the second half to be more moderate than the first half. According to the management team, the Chinese economy has been affected by the Sino-US trade war and the downside risks have increased, it has not seen a big impact on sales, and the company has no plans to increase the discount promotion.

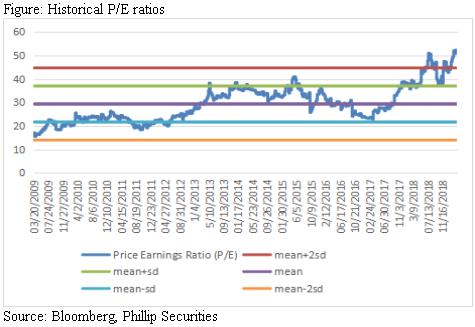

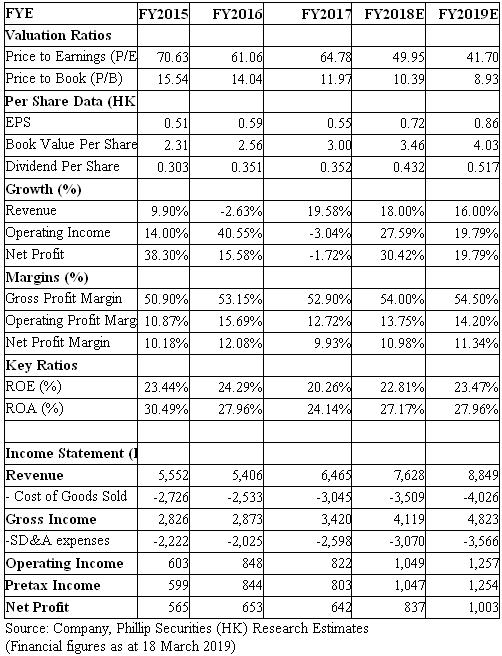

We expect EPS of FY2019 will be RMB0.77, with target price HKD38.5,and target price-earnings ratio 44.7 times . (Closing price at 18 March 2019)

Business Overview

About the company

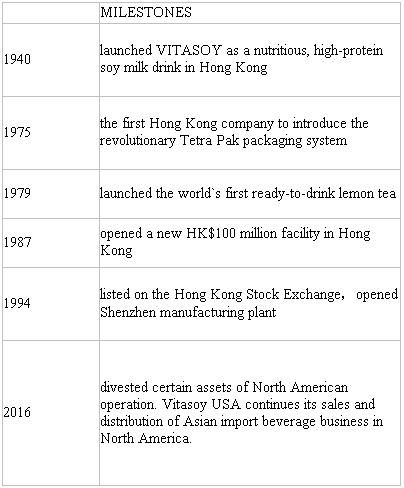

The VITASOY story began in 1940. Its founder, Dr K.S. Lo wanted to help the people of Hong Kong during the war by bringing them a nutritious, protein-rich soymilk drink at an affordable price. In 1979, it launched the ready-to-drink lemon tea. In 1994, it was listed on the Hong Kong Stock Exchange.

China's business is currently based in South China

At present, the Vitasoy business is mainly concentrated in the South China market, accounting for more than 60% of the revenue of China business. Soya milk business in China faces competition mainly from the two dairy giants Yili and Mengniu, while lemon tea business faces competition mainly from Taiwanese brands such as Uni-President and Tingyi.

According to the management team, Vitasoy ranked the third in dairy and soya milk beverage market in Guangdong province in 2018, with a market share of 12%. Yili and Mengniu ranked the first and second, with market share of 28% and 17% respectively. The market share of Vitasoy in Hubei is 9%, whereas that of Yili and Mengniu is 32% and 27% respectively. Vitasoy ranked the 5th in Shanghai with market share of 2.4%. The top four are Bright Dairy, Mengniu, Yili and Coconut Palm, with market share of 42%, 16%, 13% and 2.4% respectively.

For the tea beverage market including lemon tea, Guangdong province is still the best performing market for Vitasoy. It ranked second with market share of 22%. Tingyi ranked the first with market share of 37%. In Shanghai, Vitasoy ranked the fifth with market share of 8.6%. Uni-President ranked the first with market share of 24%. In Hubei, Vitasoy ranked the sixth with market share of 4%. Uni-President ranked the first with market share of 30%.

Interim results review

Revenue of 1H increased 22% to HK$4448million, compared to 23% of last year's growth. As the main contributor to the company, revenue of Vitasoy China increased 33%, whereas Hong Kong Operation increased 4%. Gross profit margin increased by 1ppt y.o.y. to 54%. The performance was driven by high growth in sales volume, favourable material costs and continuous improvements in manufacturing efficiency.

According to the management team, the cost of soybean as one of the key raw materials, will be locked in half a year to one year ago by contract. The company does not import soybeans from the United States, so the Sino-US trade war does not has any impacts on the cost. Soybeans used in China market are mainly sourced in China, for Hong Kong and Singapore markets are purchased from Canada, and for Australia are sourced locally.

Total operation expenses increased 26% y.o.y. in 1H as the company increased investment in brand equity programs, and higher staff-related and logistic expenses. Marketing, selling and distribution expenses increased 32%. Profit attributable to equity shareholders was HK$518million, representing an increase of 30% y.o.y.

Vitasoy China achieved 42% growth in profit. The performance was driven by high growth in sales volume, favourable material costs and continuous improvements in manufacturing efficiency. The appreciation of average Renminbi when comparing to previous interim period had a positive impact on results when reported in HKD.

The company re-launched its premium high nutrition VITASOY Health Plus range. For VITA, it continued to drive expansion of Lemon Tea product across regions and channels. All regions grew strongly, including Guangdong province, and so did all main trading channels. E-commerce operations also continued to grow.

For Hong Kong Operation, revenue increased with broad based growth across all product lines and main channels, across on-the-go and home occasions, with e-commerce registering particularly strong growth from its small base. It has accelerated investments in both core brands VITASOY and VITA, and continued its 2-year internal investment programme in manufacturing and logistic infrastructure. This program is expected to increase spending during second half of this financial year and next financial year.

For other markets, revenue in Australia and New Zealand accelerated to 9% in local currency, and 5% in HKD, due to the appreciation of Australian dollar.

According to the management team, it expects strong but more moderate growth in 2H. China is expected to continue to be fastest growing market, behind a balanced combination of per capita consumption increase in the established markets and geographical expansion.

Valuation and Risk

We expect EPS of FY2019 will be RMB0.77, with target price HKD38.5, and target price-earnings ratio 44.7 times . Potential risks include China market expansion missing expectations, raw material prices fluctuate significantly, and market competition has deteriorated.(Closing price at 18 March 2019)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()