-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

IGG (8002.HK) - Surged income from Castle Clash probably brings more than double revenue

Monday, June 16, 2014  7893

7893

IGG(8002)

| Recommendation | Buy |

| Price on Recommendation Date | $5.520 |

| Target Price | $7.180 |

Weekly Special - 002050 Sanhua

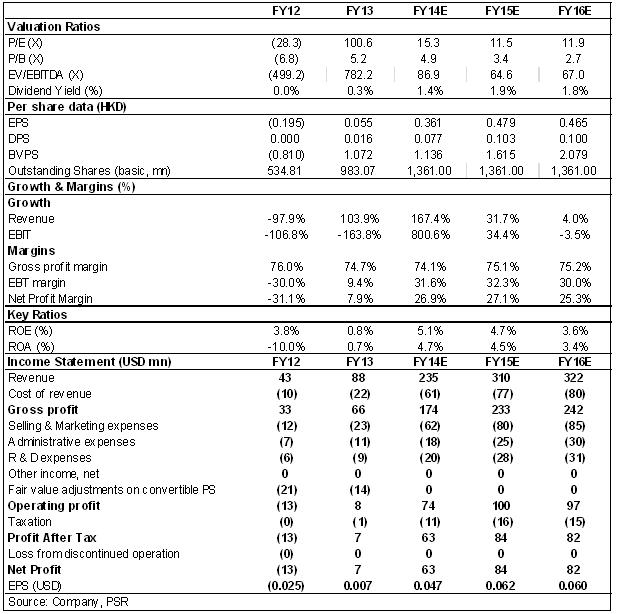

-IGG‘s 1Q14 revenue of US$ 44.1 millions, grew 205.5% yoy, equals over 50% of its 2013 total turnover. Among that, 84% is contributed by its flagship game “Castle Clash” (CC) launched in July 2013. Profit attributable to shareholders turnarounds to US$ 13.6millions profit, already exceeded the total 2013 net profit of US$ 6.9millions. Earnings per share amounted to US$ 1 cent.

-With cooperation with Tencent in promoting CC, it is expected IGG could further enhance its market share in PRC. Only 22.3% of the revenue from CC comes from IOS as at 1Q14, there is still a large room to grow.

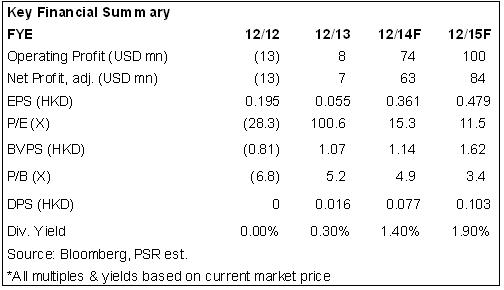

-We give IGG an initial rating of “BUY” with target price HK$ 7.18, equivalent to 19.9x/15x of 2014 and 2015 forecasted EPS.

Financial Highlights

IGG has announced its 1Q14 result with revenue of US$ 44.1 millions, grew 205.5% yoy, and which is already accounted for over 50% of its 2013 total turnover. Among that, US$ 29.2millions is contributed by its flagship game “Castle Clash” launched in July 2013, which accounted for 84% of the mobile games income. Profit attributable to shareholders turnarounds from 1Q13’s US$ 3.9millions loss to US$ 13.6millions profit, which is already exceeded the total 2013 net profit of US$ 6.9millions. Basic earnings per share amounted to US$ 1 cent.

How we view this

IGG has obtained a very handsome FY13 and 1Q14 performance, which is mainly due to “Castle Clash” (CC). After its cooperation with Tencent, it is expected IGG could further enhance its market share in PRC. On the other hand, only 22.3% of the revenue from CC comes from IOS as at 1Q14, which IOS is launched 3 months later than Android. Although the revenue from IOS already increases 124.1% to US$ 6.5millions in 1Q14 compared with US$ 2.9millions in 2013, there is still a large room to grow.

Investment Action

Therefore, based on the high growth on CC and more new games will be launched this year, together with the potential benefit brings by the cooperation with Dynam (6889.HK) to develop pachinko machines. We give IGG an initial rating of “BUY” with target price HK$ 7.18, equivalent to 19.9x/15x of 2014 and 2015 forecasted EPS.

The flagship game “Castle Clash” contributes most of the growth

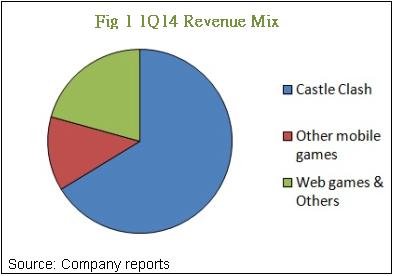

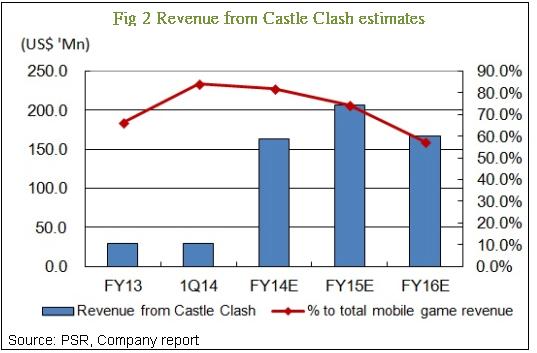

According to IGG’s financial report, the revenue from its flagship mobile game “Castle Clash” (CC) accounted 84% of the total mobile game revenue and 66.3% of the total turnover. CC was launched in July 2013 and with less than a year time, the Monthly Active Users (MAU) grew to 9.4 millions.

It is expected the growth on revenue would continue in 2014 since IGG has cooperated with Tencent to launch CC exclusively in Tencent mobile game platform and Tencent will be solely responsible for its marketing and promotion in PRC. However, since the product life is comparatively short for mobile games, it is expected the growth momentum will shift to other mobile games after 2015 and revenue from CC begins to drop. The company plans to launch 35-40 new games this year.

Before the launch of CC, web games contributed for US$ 32.6 millions, 75.6% of the total revenue of in 2012 and mobile games just accounted for 5.1% of the total turnover. Situation changed after IGG turned its focus on mobile games development and operation. At the end of 2013, mobile games accounted for 49.7% of the total revenue. As at Mar 31 2014, mobile games accounts for 79.3% of the total revenue. It is expected the portion would continue to grow and the income from web games and others would shrink conversely.

Business scattered around the world

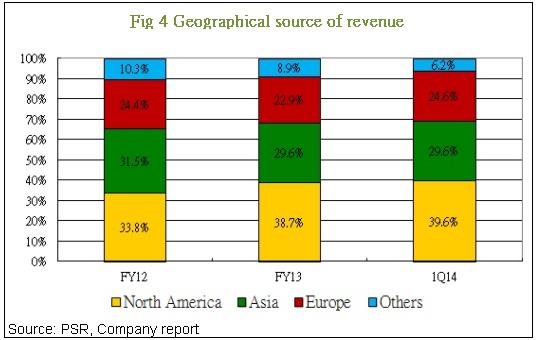

As at March 31 2014, IGG has over 147 millions registered player accounts and 14.5 million MAU around 180 countries in the world. The company has work offices in US, Canada, China and Philippine, and placed a large portion of its development staffs in China to lower the personnel cost. As at the first quarter of 2014, 39.6% of total revenue comes from North America, while 29.6% and 24.6% come from Asia and Europe respectively. The largest part of revenue comes from North America, which continues to grow from 33.8% in 2012, but revenue from Asia and other countries besides Europe pull back. However, with the marketing cooperation with Tencent and the launch of CC in Tencent mobile games platform, we believe the revenue from Asia would grow in 2014.

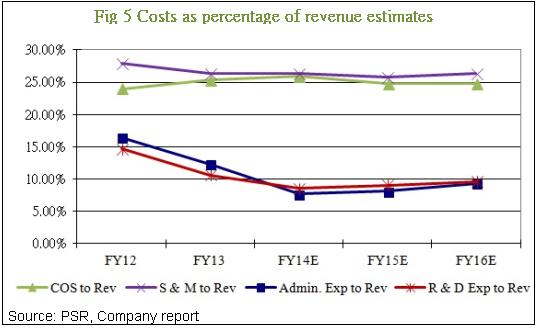

Cost stays, expenses have not follow the rapid raise of revenue

The 1Q14 cost of sales and selling & distribution expense increases around 255%, to US$ 11.1millions and US$ 11.9millions respectively. COS and Selling expense are expected to maintain at around 25% to 26% of revenue. However, the administration and R&D expenses are not able to catch up with the rapid revenue grows during a short period. Both of the ratio are expected to drop from 15% in 2012 to below 10%, lead to a better EBIT margin this year.

Valuation

IGG has obtained a very handsome FY13 and 1Q14 performance, which is mainly due to “Castle Clash” (CC). After its cooperation with Tencent, it is expected IGG could further enhance its market share in PRC. On the other hand, only 22.3% of the revenue from CC comes from IOS as at 1Q14, which IOS is launched 3 months later than Android. Although the revenue from IOS already increases 124.1% to US$ 6.5millions in 1Q14 compared with US$ 2.9millions in 2013, there is still a large room to grow. Therefore, based on the high growth on CC and more new games will be launched this year, together with the potential benefit brings by the cooperation with Dynam (6889.HK) to develop pachinko machines. We give IGG an initial rating of “BUY” with target price HK$ 7.18, equivalent to 19.9x/15x of 2014 and 2015 forecasted EPS.

Potential Risks

The growth on Castle Clash slow down;

Fail to carry on the growth with new games;

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

E-Check

Login

![]()

![]()

![]()

![]()