-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Geely Automobile (175.HK) - Cold export, warmer domestic

Tuesday, October 28, 2014  15021

15021

Geely Automobile(175)

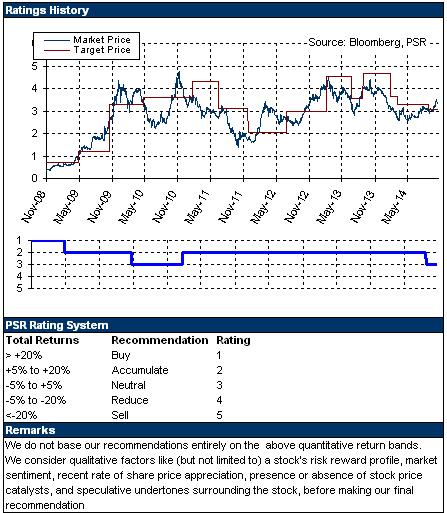

| Recommendation | Buy |

| Price on Recommendation Date | $3.330 |

| Target Price | $4.000 |

Weekly Special - 000157.SZ Zoomlion

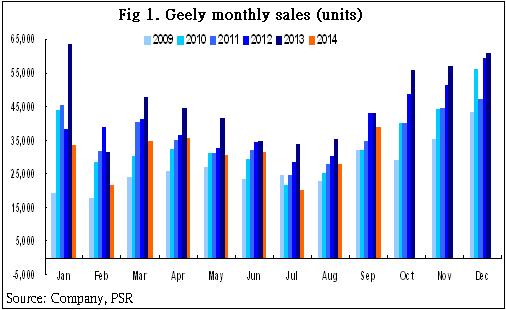

-September saw 39019 sales units, down by 9% YoY, which sharply narrowed from the double-digit decline rate before, but up by 41% MoM.

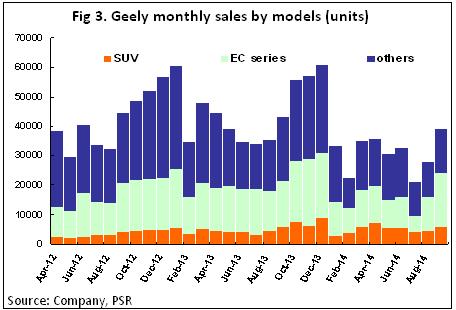

-Seen from the MoM sales, the sales of New Emgrand and SUV have contributed to nearly 70% of the incremental sales.

-The Company had a total sales volume of 86819 cars in the third quarter, which was 22.7% less than that of last year's same period.

-The sales volume of the first three quarters totalled 274005 cars with YoY decline rate of 27%, which achieved 64% of its annual goal. It means that in order to reach the goal successfully, the average monthly sales volume have to reach as high as 52000 cars for the remaining three months of this year.

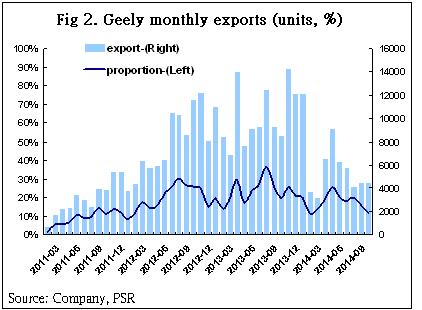

-Export sales reported 4677 cars in September, down by 45% YoY, still had a big distance to the average monthly sales of 10000 in last year.

-The domestic sales volume had clearly rebounded and the YoY decline rate downed to 1%, while the MoM rate had a significant rebound of 48%.

-In Sep., Geely signed a letter of intent for cooperation with Corun, a leader in the Ni-MH battery technology field in China, and planned to set up a JV.

How we view this

Through adjustment over most of this year, Geely has shown an increasingly clear brand strategy. The government finally launched a new national policy in September this year, which obviously indicated the intention to support self-owned brands. Geely has 6 car models that were included, accounting for more than 60% of the last year’s total sales volume of the company. The restart of the new national policies will help the sales volume of the company to speed up again.

As the models co-produced by Geely and Volvo has to wait until after 2016, the result of Geely in recent 2 years would be constrained by the limitation of popular models; the future sales volume of its new energy vehicles is also subjected to the promotion and development of the domestic new energy vehicles market. However, the acceleration of the new energy vehicle commercialization will stimulate the market expectation and the level of its valuation.

Investment Action

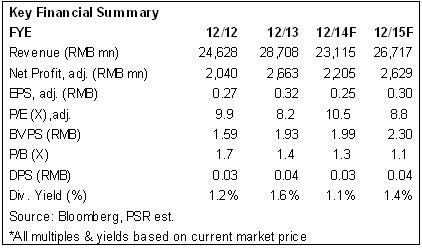

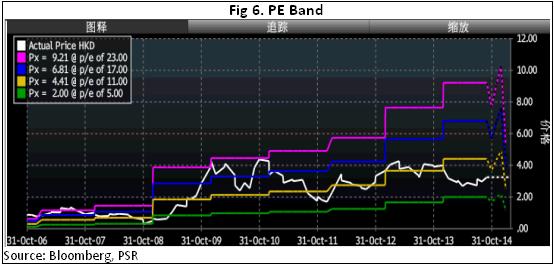

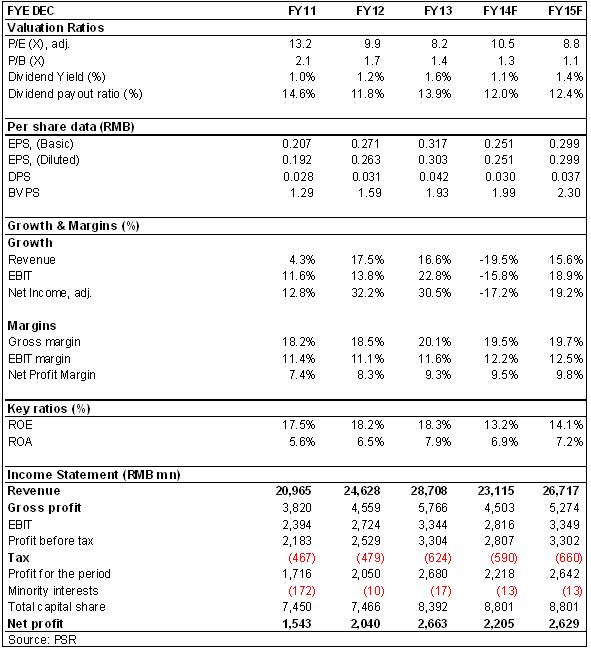

From our unrevised financial forecast, we lift our target price to HK$4.00, based on 12.6/10.5xP/E in 2014/2015, and the suggestions of “Buy” rating be given.

The YoY decline rate of sales volume in September narrowed down, while its MoM rate rebounded significantly

In September, the sales of Geely had a record of 39019 cars with a YoY decline rate of 9%, which sharply narrowed from the double-digit decline rate before. As for the MoM growth rate, it had a significant rebound of 41% compared with the previous month. The New Emgrand launched in the end of July performs strongly and is the main driving force, whose sales in September reached 13794 cars with MoM growth rate of 92%. Moreover, SUV cars showed the tendency of bottoming out, the total sales of which in September were 5766 cars, and remained the same YoY, while rose by 26% MOM. Seen from the MoM sales, both the above have contributed to nearly 70% of the incremental sales.

The export remains in the downturn, while domestic sales show signs of getting warmer

Affected by the unstable political situation of the main export market, Geely had an export sales volume of 4677 cars in September. The YoY decline rate was 45%, while MoM rate increased slightly by 5%. It still had a big distance to the average monthly sales of last year, which were 10000 cars. The domestic sales volume had clearly rebounded and the YoY decline rate downed to 1%, while the MoM rate had a significant rebound of 48%.

The Company had a total sales volume of 86819 cars in the third quarter, which was 22.7% less than that of last year's same period. The sales volume of the first three quarters totalled 274005 cars with YoY decline rate of 27%, which achieved 64% of its annual goal. It means that in order to reach the goal successfully, the average monthly sales volume have to reach as high as 52000 cars for the remaining three months of this year.

Brand adjustment is getting clear day by day, and reapplying the new round of national policies helps speed up the sales of the Company

Through adjustment over most of this year, Geely has shown an increasingly clear brand strategy: after cancelling three sub-brands and integrating them into one Geely brand, the products of the company will be mainly classified into five product lines in the future, namely KC Series, Emgrand Series, Vision Series, Kingkong Series and Panda Series, while the subsequent integration of dealer channels is expected to be completed within 1 to 2 years.

The state subsidies for saving energy and benefiting people aiming at small emission economical cars has expired since last year October, while new policies delaying being published restrain the consumer demand on part of low-end cars, especially those self-owned brands, facing the challenge that joint-venture automobile enterprises have launched more competitive low-end car models successively, and the market share of self-owned brands has declined for 12 consecutive months. The government finally launched a new national policy in September this year, which obviously indicated the intention to support self-owned brands. Geely has 6 car models that were included, accounting for more than 60% of the last year’s total sales volume of the company. The restart of the new national policies will help the sales volume of the company to speed up again.

HEV technology commercialization stepping into a fast development period

During the Beijing Auto Expo in 2014 April, Geely launched the deep HEV model of Emgrand EC7 and the plug-in HEV model of Emgrand Cross, which is expected to be launched at the end of this year and 2015H2 respectively. In September of this year, Geely signed a letter of intent for cooperation with Corun, a leader in the Ni-MH battery technology field in China, and planned to set up a joint venture company. Geely would contribute assets like HEV powertrain system CHS, etc., while Corun would contribute assets like automobile power battery management system BPS, etc. This joint venture company might break the patent block of Toyota's THS technology. With ability to compete with the international HEV giants, its subsequent extensible space is expansive. In addition, the joint venture company may attract more automobile manufacturers to buy the shares in order to promote technology platformization and mass production, thus to lower the production cost and improve product competitiveness.

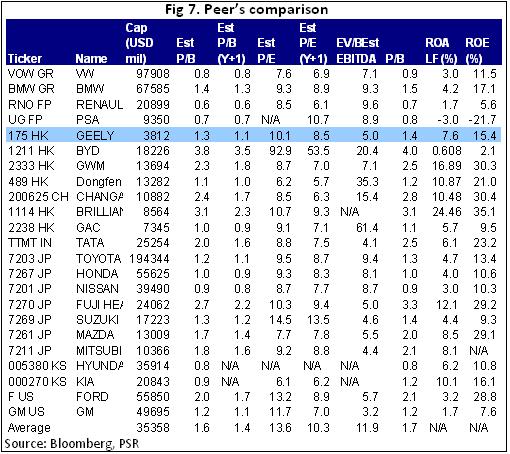

Valuation and Rating

As the models co-produced by Geely and Volvo has to wait until after 2016, the performance of Geely in recent 2 years would be constrained by the limitation of popular models; the future sales volume of its new energy vehicles is also subjected to the promotion and development of the domestic new energy vehicles market. However, the acceleration of the new energy vehicle commercialization will stimulate the market expectation and the level of its valuation.

From our unrevised financial forecast, we lift our target price to HK$4.00, based on 12.6/10.5xP/E in 2014/2015, and the suggestions of “Buy” rating be given.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()