-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Samsonite International SA (1910.HK) - Performance in 2015Q1 was achieved strongly

Thursday, June 11, 2015  7808

7808

Samsonite International SA(1910)

| Recommendation | Accumulate |

| Price on Recommendation Date | $26.050 |

| Target Price | $30.000 |

Weekly Special - 3306 JNBY Design Limited

Summary

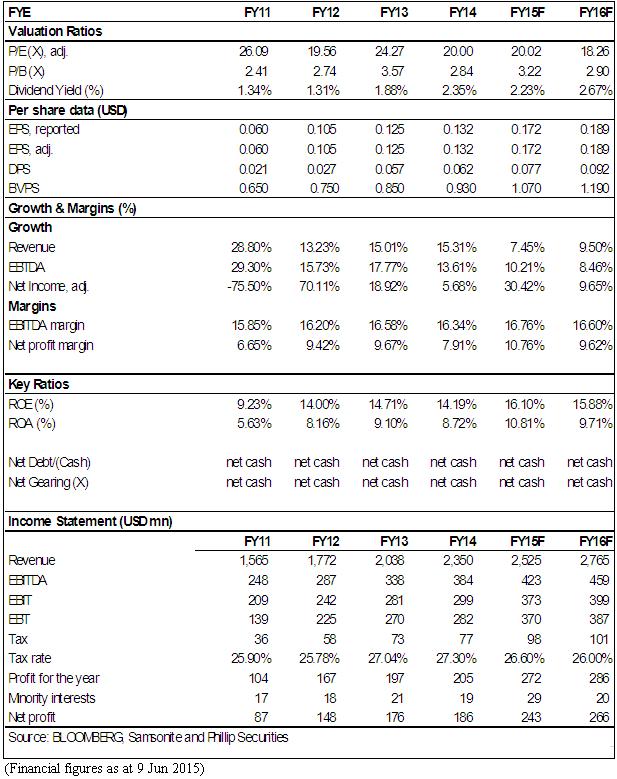

-2015Q1 saw Samsonite achieve the net sales growth by 10.8% yoy up to US$567 million, and if excluding the currency exchange rate, its consolidated net sales in Q1 rose by 18.5% yoy. During this period, calculated at a fixed currency benchmark, the Company's net sales achieved in Asia went up by 18% to US$232 million, up by 25.3% to US$183 million in North America, up by 13.6% to US$112 million in Europe and up by 11.5% to US$37 million in Latin America.

-The sales growth in Q1 met our expectation and continued to rise at a double digit rate (fixed exchange rate) in the four continental markets, indicating that the Company has had strong endogenous capability. In particular, the growth in Asia and North America was higher than in Europe and Latin America, being of more significance in supporting the continuing sales growth in the future.

-From early Q2, a few factors have had positive effects on Samsonite's operation and business. First, the acquisition of Rolling Luggage is expected to push up its sales. The second one is exchange rate. After hitting 100 mark in Q1, the US Dollar Index (USDX) fluctuates around 95-100. It is believed that the end of strong US Dollar has a positive significance to its sales in Asia, Europe and Latin America.

-Samsonite has completed the acquisitions of three brands in 2014. We can see that Samsonite is walking forward firmly on the road of diversification of products and brands, which provides potential power for the business development and result growth of the company in emerging markets. In finance, the three transactions` takeover price altogether equals to about 200 million dollars. In 2014, 110 million dollars of revenue and 1.1 million dollars of profit were made. Although it is hard to describe the acquisition price is cheap, it is good for rising the enterprise's value and establishing more advantages in competitions.

-In 2014, the liability scale of Samsonite increased and the total liability was amount to 67 million by the end of the period, which grew 346% compared to the 15 million at the end of 2013; mostly on account of the remarkable rising short-term liability, the leverage ratio increased from 1.3% in 2013 to 5.2%; however, due to that the liability scale is relatively small, the whole is still in the state of net cash. At the end, the company's cash dropped from 225 million to 140 million dollars.

-Samsonite continuously carries out acquisition to make its product and brand combinations diverse and effectively expand its "defense river" for competition. Yet, the company's steady balance sheet benefits from lower financial leverage, limited capital costs and sufficient cash flow; it is good for helping the company to establish more advantages in competitions. Organic growth and denotative expansion drive Samsonite's continuous and healthy growth. We maintain Samsonite's "Accumulate" rating with 30HKD target price for 12 months, equivalent to 20 times and 18 times of 2014 and 2015's prospective PE ratio. (Closing price as at 9 June 2015)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()