-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

GWM (2333.HK) - Sales Volume Bucks the Trend

Monday, May 20, 2019  12217

12217

GWM(2333)

| Recommendation | Accumulate |

| Price on Recommendation Date | $5.960 |

| Target Price | $6.590 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

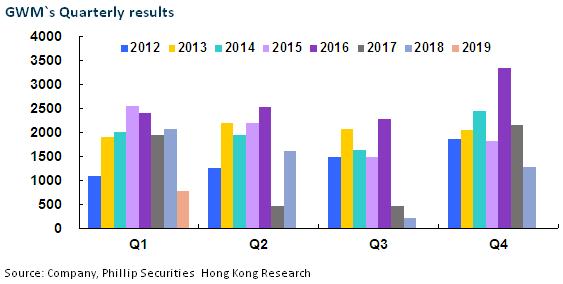

Sales Volume Bucks the Trend, and Rises 6.5% yoy in the First Four Months

Great Wall Motor (GWM)'s sales figures for April showed a 2.5% yoy increase to 83,800 units, continuing to buck the trend (-16% for the industry). The sales volume of SUV series decreased 3.6% yoy to 65,700 units, dropping from a proportion of nearly 90% to 78.4%; the sales volume of Pickup Wingle is 13,099 units, increasing by 1.1% yoy and staying stable; the sales volume of sedans is 5,002 units, increasing by 680% yoy, mainly owing to the sales volume of new energy vehicle sub-brand ORA of 4,614 units.

In terms of SUV, Haval series sold 58,444 units in total, increasing by 6.2% yoy, with 3,295, 2,294, 28,045 and 1,084 units for H2, H4, H6 and H9, respectively, dropping by 56%, 55%, 18% and 17% yoy, and 10,004, 10,140 and 2,034 units for M6, F7 and F5, respectively, which attributed most to the increase. The price drop of M6 has stimulated the demand, and the launch of F7 has received a sound market response, with a stable monthly sales volume of above 10,000 units. High-end brand WEY was still in the running-in stage, and its total sales volume dropped by 44.5% yoy to 7,293 units.

In the first four months, the accumulated sales volume of GWM recorded 368,000 units, increasing by 8.65% yoy, with SUVs accounting for 81%, with 298394/49595/19671 units for SUV/Pickup/Sedan, respectively, up by 2.3%/11%/858% yoy,.

Net Profit Edges Up 4% in 2018

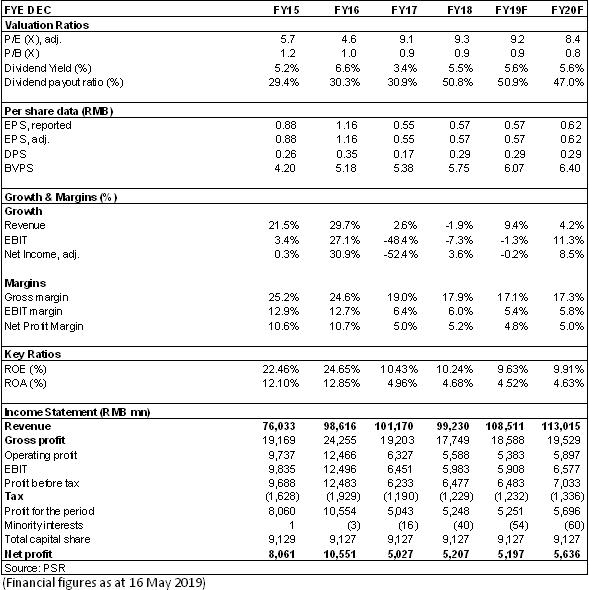

In 2018, GWM recorded a revenue of RMB99.23 billion, dropping by 1.92% yoy, a net profit of RMB 5,248 million, increasing by 4.07% yoy, and a net profit after deducting non-recurring profits and losses of RMB3,889 million, dropping by 9.53% yoy. He non-recurring revenue was RMB1,319 million, increasing by RMB590 million when compared to that of the same period in 2017, which was attributed to the interest revenue from performance bond. EPS stood 0.57yuan, with 0.29-yuan DPS. The dividend payout ratio reached 50%.

In 2018, the Company sold 1,053,000 units of vehicles in total, dropping by 1.60% yoy, and above the industry average of -5.8%; among which, Haval series sold 766,100 units, dropping by 10.07% yoy; WEY series sold 139,500 units, increasing by 61.39% yoy; ORA series sold 3,515 units; and Wingle series sold 138,000 units, increasing by 15.16% yoy. During 2018, in the descending SUV market, the Company bucked the trend and increased its market share by significant official price drop and promotions to scale up the sales volume. However, its profitability was damaged, with the gross margin being 16.7%, dropping by 1.7ppts when compared to that of 2017. RMB3.96 billion was spent on R&D, of which 56% was capitalized. ROE dropped by 0.31ppts, to 9.91%.

Pricing Impulse Strategy Continues in 2019, and First-quarter Net Revenue Falls 63% yoy

In 2019Q1, GWM recorded a total revenue of RMB22.63 billion, dropping by 14.8% yoy, and a net profit attributable to the parent company of RMB770 million, dropping by 62.8% yoy and 40% qoq to the fourth quarter of 2018. In 2019Q1, the Company recorded a gross margin of 15.8%, dropping by 6.7ppts yoy and increasing by 1.4% qoq to the last quarter, with the yoy drop mainly attributed to the Company's continuing its pricing impulse strategy from 2018H2 and the qoq increase attributed to the rose sales proportion of new F-series vehicles and pickups that improved the sales structure.

Price Pressure Remains in Auto Market, SUV Stock Market Share Increases Steadily, and Segment Expects Break-through

In 2019, GWM will launch new models including Haval F7x, WEYVV7GT, WEYP8GT, ORA R2 and high-end pickup Truck-series, aiming at an annual sales target of 1.2 million units, of which around 31% has been completed for now. F7x, powered by a 1.5GDIT/2.0GDIT+7DCT dynamic combination and with a series of intelligent technological configurations, such as a fastback design that highlights youth and a L2-class autonomous driving technology, is expected to gain a share in the increasingly popular sport sedan market. It is expected that the F-series will account for 30% of the total sales volume of Haval series. Meanwhile, by virtue of its superior interior space, driving range and model positioning, ORA R1 showed a burst in end demand, and with the release of capacity, its sales volume is promising in the future. In conclusion, notwithstanding the remaining price pressure in the domestic auto market under the competitive stock pattern, with the break-through in new products and increased proportion of upgraded products in the Company's segment, its market share is expected to maintain a steady rise and its gross margin will improve quarter by quarter.

Investment Thesis

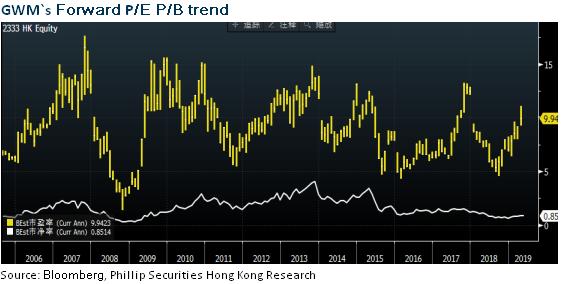

GWM's recent car sales have gone against the peers` trend, and the company's inventory control is better than its peers, but the future car market price is still under pressure. However, the company's transformation and trials are pushing the company's product structure and product scale to rise further. In terms of valuation, we adjust our target price to HK$6.59, equivalent to 10.1/9.3 P/E and 1.0/0.9 P/B ratio in 2019/2020. We maintain the rating of “Accumulate”. (Closing price as at 16 May 2019)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle project is poorer than expectations

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()