-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of November. 2020

Wednesday, December 2, 2020  10192

10192

Report Review of November. 2020

Weekly Special - 3306 JNBY Design Limited

Sectors:

Air & Automobiles (Zhang Jing),

TMT & Education (Kevin Chiu)

Consumer & Property Management (Timothy Chong)

Telecommunication & Technology hardware (Parker Chan)

Automobile & Air (ZhangJing)

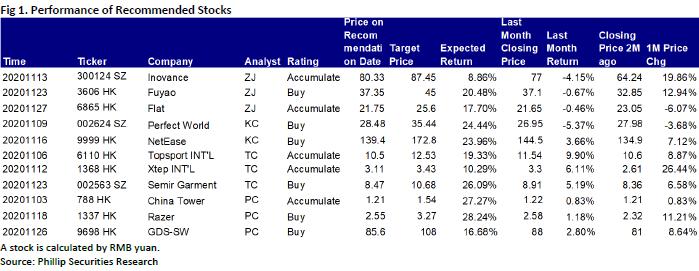

This month I released 3 updated reports of Inovance (300124.CH), Fuyao Glass(3606.HK) and FLAT Glass (6865.HK), which got success by their unique Competitive edge. Among them, we highly recommend FLAT Glass .

In 2020Q3, Flat Glass recorded revenue of RMB1.52 billion, up by 13% yoy and 17.6% qoq. The net profit attributable to the parent company was RMB350 million, up by 42.6% yoy and 42.9% qoq. The profit growth is still beyond the early market consensus. In the first three quarters, the Company's net inflow of operating cash was RMB1.69 billion, which was significantly improved compared with the net inflow of RMB220 million in the same period of last year. The shortage of products caused the price of photovoltaic glass to increase twice in July and September. On the other hand, the cost of raw materials such as soda ash and natural gas remains low, and the profitability of manufacturers has therefore improved significantly. Q4 is the peak season for photovoltaic installed capacity. We expect that the high prosperity of the photovoltaic glass industry is to continue. The average product price will reach RMB46/square meter, and the Company's annual gross profit can exceed above 40%.

Due to the long construction period, we believe that the tight supply and demand pattern of the industry will continue next year, which will be difficult to change in the short term. It is expected that the price will be high and then low, fluctuating around RMB36 on average. The Company's Vietnam production line, Anhui fourth, fifth, and sixth production lines totalling 5,600 tons/day will soon be put into operation this year and next, and it is expected to benefit from the high price range in 2021.

After more than ten years of development, domestic photovoltaics will officially enter the era of affordable Internet in 2021. According to the 14th Five-Year Plan, new energy shall account for 30%, but now it is only 5%, of which photovoltaics account for only 3.5%. In the next five years, the average annual compound growth rate of the photovoltaic industry is expected to reach 20%. In the medium and long term, in order to achieve the 2060 carbon neutrality goal, the photovoltaic industry will be a major driver. The situation of strong demand and tight supply is difficult to reverse, and the market share of leading companies will continue to expand.

TMT & Education (Kevin Chiu)

I have issued 2 initiation reports this month, namely Perfect World (002624.SZ) and NetEase-S (9999.HK). Between them, I highly recommend NetEase.

NetEase's focus of game genre is significantly different to Tencent. Tencent's main games Honor of Kings (王者榮耀) and Game for Peace (和平精英) are both moderate games with social characteristics in them. These games are user friendly to new joiners and suitable for both men and women in nature. Therefore, these games have a very high MAU. In addition, these games are backed by the 2 largest social media platform in China, Wechat and QQ. Hence, these 2 games basically monopolize the light-moderate mobile game markets in China, with very few similar games on the market. On the contrary, NetEase has been deeply focused in R&D of core game genres such as MMORPG genres since its inception. However, due to the high average game time and high spending nature of core games, which in game performance and rankings are hugely affected by the game time and money spent by users, the MAU of core games are significantly lower. But at the same time, core games have characteristics of higher ARPU and longer life cycles. Taking into account Tencent's absolute innate advantages in light and moderate games, the company avoids direct competition with Tencent and focuses on core games is a wise choice.

The company has always paid great attention to the product life cycle and scalability. According to Tencent Game Academy, the average life cycle of a PC game is 3-5 years, but the company's PC games Westward Journey (大話西遊) and Fantasy Westward Journey (夢幻西遊) were launched in 2002/2004 respectively. So far, these two games have been operating stably for 18/16 years, which is far higher than the average of a PC game. The long life cycles were mainly due to the company's constant operation and maintenance of the game. Both of these games had launched major upgrades in 2013, prompting gamers to maintain freshness to the game, hence reducing the decline in ARPU. As for mobile games, according to Frost & Sullivan, the average life cycle of Chinese mobile games is 3-12 months, but the company's core mobile games have all operated for 4-5 years, while still maintain stably on the China Top 10 mobile games ranking in terms of revenue generated.

Consumer & Property Management (Timothy Chong)

I have released two update reports covering Topsports INTL. (6110.HK) and Xtep Int`l(1368) and one initiation report covering Semir Garment (002563.SZ) this month. Among them, I highly recommend Semir Garment (002563.SZ).

Semir Group was established in 1996, opened the first Semir brand store in 1997, and started a brand extension strategy in 2002, founded the children's clothing brand "balabala" and established the company's predecessor. The company's mainly engaged in product design, brand management, supply chain management and channel development business. Its brands mainly include adult leisure brand "Semir", children's clothing brand "balabala", "MarColor" and "mini balabala". The company has now developed into a dual-leading position in the domestic casualwear clothing and children's clothing industries. According to the China National Garment Association, the company ranks 8th in the national apparel industry based on 2019 operating income. In addition, according to euromonitor, balabala ranks first in the children's clothing market with 6.9%, which is 5.3 pct higher than the second place, Anta Kid. In 2019, the company's revenue from children's clothing business was approximately RMB 12.66 billion, of which 2.97 billion came from the Kidiliz Group, which was transferred in September, an increase of 43.5% year-on-year, and its casual apparel revenue was RMB 6.54 billion, a YoY decrease of 3.6%.

Semir Apparel has taken a leading position in the domestic children's and casual wear markets. The acquisition of Kidiliz's business in 2018 has brought significant revenue growth to the company, but at the same time it has also significantly increased the company's period expenses. In addition, the epidemic situation in Europe has not improved. Kidiliz The loss brought by the company expanded. The company is expected to improve its profitability after divesting Kidiliz. The company has a leading advantage on the children's clothing track and is expected to bring continuous growth to the company.

Telecommunication & Technology hardware (Parker Chan)

I have released two initiation reports covering Razer (1337.HK) and GDS-SW(9698) and one update report covering China Tower(00788.HK) this month. Among them, I highly recommend GDS-SW(009698.HK).

The IDC industry is a heavy asset industry. The larger the scale, the lower financing costs and economies of scale. As of June 30, 2020, about 98% of the Company's self-developed data centers are located in first-tier markets, such as Shanghai, Beijing, Shenzhen, Guangzhou, Hong Kong, etc. Because these areas have the highest density of Internet users, a high proportion of data and applications are mission-critical and latency-sensitive. In order to meet the needs of clients from financial, industrial, commercial, and communications industries, the Company locates data centers close to major customers area. This makes the Company to be more competitive in serving customers in Tier 1 markets with our existing facilities. The abundant land reserves have laid a solid foundation for the Company's sustainable development, and gradually formed a strategic asset-based economic moat.

China is one of the largest and fastest growing digital economy globally. China's rapid adoption of new technologies such as cloud computing, 5G, artificial intelligence, big data, machine learning, blockchain, IoT, augmented and virtual reality, e-payment and digital currency is expected to increase exponentially the volume of data created, transmitted, processed and stored, much of which will take place within and between data centers. Customers from cloud services accounted for the Company's total contract area (71.8% as of June 30, 2020). According to data from iResearch, the size of China's cloud market is RMB 149 billion in 2019, and is expected to increase at a 34.1% CAGR to reach RMB 645.2 billion in 2024. Cloud computing is the Company's main source of income. Cloud vendors have extremely high data security requirements, so the partnership is stable. The contract period is generally 6-10 years. We expect the Company will directly benefit from the rapid development of cloud computing.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()