-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Nine Dragons Paper (2689.HK) - Responding to imported waste paper restrictions with overseas recycled pulp, and focus on overseas markets and production capacity for future development

Tuesday, November 20, 2018  10980

10980

Nine Dragons Paper(2689)

| Recommendation | BUY |

| Price on Recommendation Date | $7.890 |

| Target Price | $12.100 |

Weekly Special - 3993 CMOC Group Limited

Investment Summary

-Revenue of FY2018 increased by 34.5% y.o.y. to RMB25.378 billion, but the sales volume was flat at 13 million tons compared to last year which means that revenue growth is entirely dependent on the increase in selling price. There were several price hikes after Luna New Year, but the price per ton in 2H was still lower than 1H, but the annual increase was nearly 20%. Since June this year, the market sentiment in China has become more cautious as the Sino-US trade war heating up. However, according to the management team, sales volume during last July to August performed well. In September, prices of finished and waste paper in some regions have been reduced. It believes that it was only short-term fluctuations. With the arrival of peak season, it expects there will be price hikes in the coming months.This year's peak season is not prosperous. In the middle and late October, prices of waste and finished paper declined, reflecting the sluggish downstream demand. Although Alibaba's online shopping platform Tmall has record high in sales during 11th November, growth rate is the lowest ever. The market still has doubts about the authenticity of the data. Near the end of the year, the price of finished paper rebounded slightly, but price cuts continued in some areas. Chinese government has gradually relaxed its macro policy recently, but the results remain to be seen. We expect that the industry will face challenges in short-term .

- Due to the tightening of import waste paper policy, was mainly focus on the requirements on the purity of waste paper, the management team revealed that it has started to import thousands of tons of recycled pulp (OCC, processed waste paper with higher purity) in the Malaysian factory. It plans to further increase the amount of OCC to 1 million tons per year. It has suggested the acquisition of Fairmont in USA which is with the production capacity of 250,000tons of OCC. If it can complete the acquisition by the end of October, Fairmont can directly provide the company with OCC. At the same time, it plans to raise the production capacity of 300,000 to 400,000 tons of OCC in Malaysian production base, and the same amount of OCC in USA. Both are currently awaiting approval from local governments. According to our preliminary estimates, the current tariff of imported OCC from US is 20%, which is lower than waste paper (25%). The cost of waste paper in US is relatively low. With processing and logistic costs, as well as tariffs, the total cost is still about USD100 per ton less than China's domestic waste paper, and can also avoid the limitation on the import of waste paper from US.

- In terms of domestic production capacity in China, Nine Dragons` 3 out of the 6 new production lines planned were intended to be postponed. We believe that this reflects the government's tightening of new capacity approval and environmental protection policies. In addition, this also implies that after the new capacity deployment in the early years, the company has not been able to obtain new land and approval for expansion after 2020. On the positive side, as the leading enterprise to delay the production capacity expansion, coupled with the policy to accelerate the elimination of disqualified production capacity, we believe all these can help the industry's supply and demand to balance, which bringing support to the final price. Compared with China, the company plans to focus more on overseas production capacity and market expansion in the future, including continuing to pay attention to suitable M&A projects with the location not limiting to the US and Southeast Asia. We maintain Nine Dragons Buy rating, forecasted PE ratio 6.5 times, the target price is lowered to HKD12.1. (current price as of November 16, 2018)

Business Overview

2018 financial year performance review

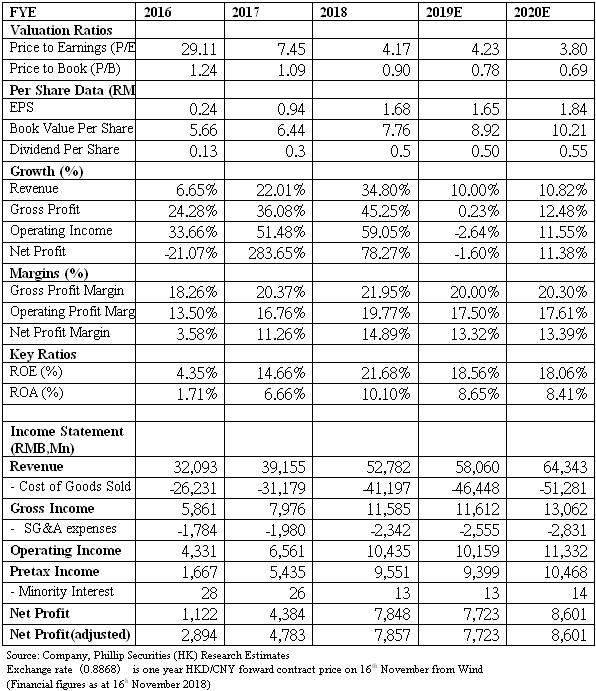

The gross profit margin(GPM) for FY 2018 was slightly lower than our expectation, which rising only 1.58 percentage points y.o.y. to 21.95%. That means GPM in the 2H of the year has narrowed to 19.52% from 24.52% in 1H. Marketing and administrative expenses accounted for 4.4% of the total revenue, down 0.6 ppt y.o.y., reflecting effective cost control strategies which meets our expectations. The operating profit margin improved by 3.01 ppt y.o.y. to 19.77%. After adjustment, the net profit per ton of paper increased significantly to RMB605.

Thanked for the control of financial expenses, low exchange losses, and effective tax rates, profit attributable to equity holders increased significantly by 79.03% y.o.y. to RMB7.848 billion. Excluding the exchange loss (net of tax) of operating and financing activities of approximately RMB 20.7 million, the profit attributable to equity holders increased by 65.1% to RMB 7.868 billion.

strategy of expanding production capacity and market overseas

The proportion of domestic and imported waste paper in FY18 was 56% to 44%. The management says that it is difficult to estimate the exacted proportion of the next two years in the short term, mainly due to the unpredictability of the policy environment, but it expects that in the long run, probably more than 50% to less than 50%. It would prefer to use as much imported waste paper as possible, as its quality is better and cost is lower than domestic waste paper.

Waste paper accounts for 70% of the total production cost, and raw wood pulp accounts for less than 30%. The company has acquired Rumford and Biron, the two pulp mills in US. They are able to produce high-quality final products from raw wood pulp, and with the addition production capacity of 120,000 tons of raw wood pulp to meet the demand of local market. Nine Dragon plans to raise the production capacity of raw wood pulp of the two pulp mills in the next two years, as well as reduce the supply to existing unprofitable customers, in order to let they get sufficient capacity to export to China.

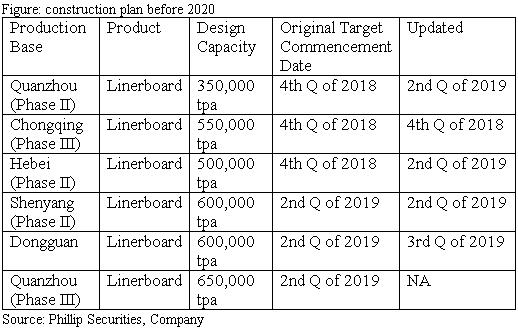

Delay in domestic production capacity

According to the new capacity plan, apart from Chongqing and Shenyang projects (target commencement dates are still Q4 of 2018 and Q2 of 2019 respectively), all others have been delayed. The Quanzhou and Hebei projects, which the target commencement date were originally in Q4 of 2018, both were delayed until the Q2 of 2019, while the Dongguan project was delayed for one quarter to the Q3 of 2019.

The management team also revealed that the cancellation of production line in Quanzhou was mainly due to the tight supply of waste paper, so it plans to move the new paper machine to Southeast Asia.

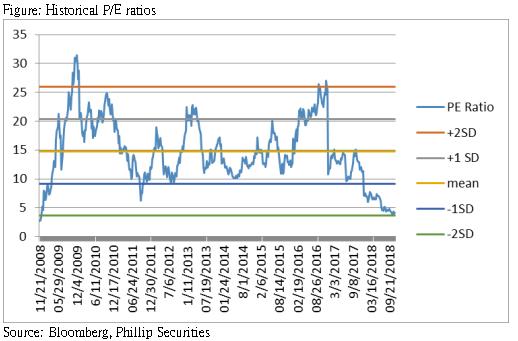

Valuation and risk

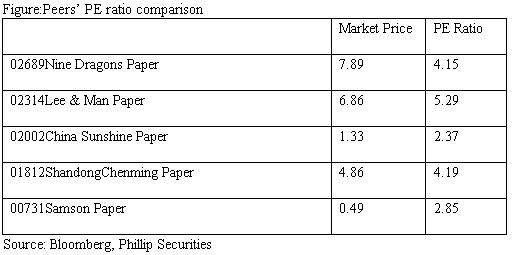

- We believe that in the short term, there are many uncertainties in the market, including the sufficient supply of the industry, the continuing tightening of the import waste paper policy, and the US import tariffs bringing upward pressure on the production cost to the industry. Nine Dragons as the industry leader, its overall performance will still be better than its peers. We also believe that its strategy of expanding production capacity and market overseas will be able to see fruits in medium and long term, including the relief of production costs in China.

We maintain Nine Dragons Buy rating, forecasted PE ratio 6.5 times, the target price is lowered to HKD12.1. Investment risks include waste paper policy changes, domestic waste price drops dramatically, and import quota not granted. (current price as of November 16, 2018)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()