-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Cathay Pacific (293.HK) - Transformation plan begins to make progress

Monday, July 16, 2018  14804

14804

Cathay Pacific(293)

| Recommendation | Accumulate |

| Price on Recommendation Date | $12.080 |

| Target Price | $14.300 |

Weekly Special - 3306 JNBY Design Limited

Investment summary

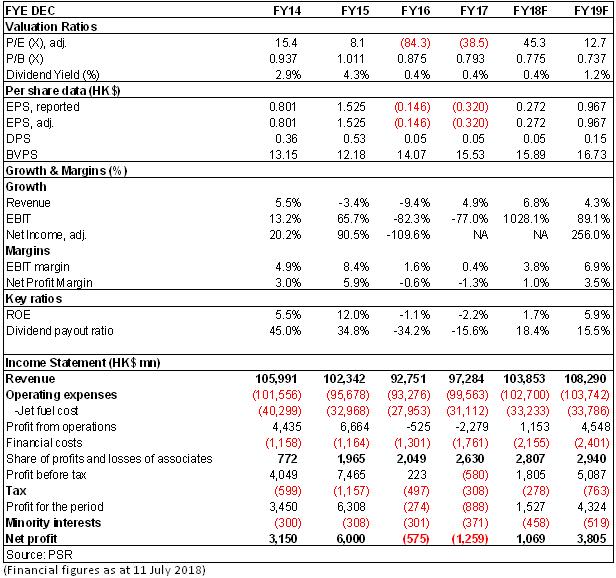

We expect overall demand of Cathay to recover moderately, while cost reductions continue to work, but rising financial expenditure might erode some of the savings. Based on the latest profit forecast, we will give the company a 12-month target price of HK$14.3, corresponding to an expected P/B of 0.9/0.85 times for 2018/2019, and upgrade to the “accumulate” rating. (Closing price as at 11 July 2018)

2017 Result Updates

Cathay Pacific recorded a loss of HK$1,259 million in 2017, which is double the annual loss in the previous year, with a loss of 32 cents per share, maintaining a dividend of 5 cents per share. The results represented a loss but was better than market expectations. This was particularly marked in the second half of last year when the profit went out of the red, earning HK$792 million.

Oil prices rose, but fuel hedging losses decreased. Fuel costs increased by 11.3% during the period as the average aviation gasoline price went up by 23% and the fuel consumption by 2.9%. However, some of the increase was offset by a 24.6% reduction in fuel hedging losses.

Financial expenditure grew fast while JVs contributed more earnings. The net financial expenditure increased by 35% to HK$1.76 billion, mainly due to the interest expenses for the financing of newly introduced aircraft. In 2017, the company received 12 A350 aircraft. In 2018, it plans to receive a further 10. Currently, the company holds 84 aircraft orders, including 32 new orders added in September 2017. Its attributable profits from the affiliated companies climbed by 28% to HK$2.63 billion, which was an important driver of the recovery in 2017H2, primarily due to the increase in attributable profit contributed by Air China Cargo and Air China.

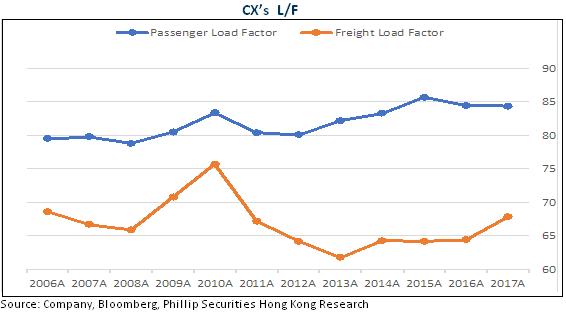

The passenger yield is still under pressure. During the period, the revenue from passenger transport fell by 0.8% YoY to HK$66,408 million, reflecting the ongoing intense competition in the market, but the decline was narrowed. The passenger yield of most routes of Cathay Pacific is still squeezed. North American (-5%), Southwest Pacific (-3.2%) and North Asian routes (-2.8%) have weaker yields, but good performances in first-class and business class cabins partially offset the drop in the economy class cabins. The overall passenger yield declined by 3.3% YoY to HK$52.3 cents, and the passenger load factor dropped slightly by 0.1 ppts to 84.4% YoY.

Cargo business rebounded strongly. The company's cargo business finally recovered from a two-year decline. Its revenue rose 19% YoY to HK$23,903 million, which reflected the increase in demand from mainland China, and restoration of fuel surcharges in Hong Kong. The freight yield increased 11.3% to HK$1.77, and the fright loan factor increased by 3.4 ppts to 67.8%. The company is raising the number of freight flights to seize the growth opportunities in the freight market. We expect cargo business will go on to enjoy an optimistic prospect based on the continued recovery of the global economy.

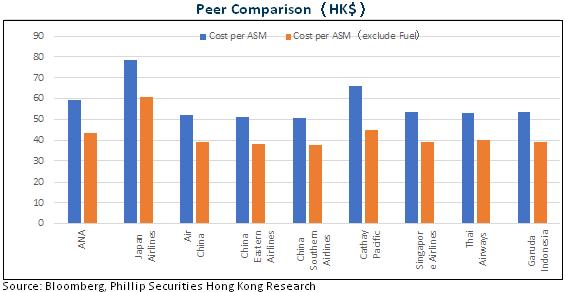

The three-year transformation plan begins to make progressIn response to the competition, Cathay Pacific officially set in motion a three-year corporate transformation plan from 2017H1, including reducing cost redundancy, improving efficiency and strengthening brand status. The goal is to become a more streamlined and more profitable airline with a view to keeping a long-term rebound in profit performances. The positive results of the corporate transformation plan began to emerge in 2017H2. The cost per ATK (excluding fuel) increased by only 0.9%, from HK$2.12 to HK$2.14.

Valuation and Rating

In the first five months of 2018, Cathay Pacific's operating data showed that the passenger load factor of the mainland China and North America routes increased by 2.2 and 2.5 ppts respectively, while the passenger load factor of the Australia/Europe/South Asia route decreased by 2.5-3.4 ppts. Except mainland Chian routes, other routes are basically in line with the distribution of capacity. For the cargo business, the F L/F rate increased by 2 ppts to 67.8%, and demand growth continued to be stronger than capacity.

So we expect overall demand of Cathay to recover moderately, while cost reductions continue to work, but rising financial expenditure might erode some of the savings. Based on the latest profit forecast, we will give the company a 12-month target price of HK$14.3, corresponding to an expected P/B of 0.9/0.85 times for 2018/2019, and upgrade to the “accumulate” rating. (Closing price as at 11 July 2018)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()