-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CR Pharmaceutical (3320.HK) - Manufacturing business developed quickly and distribution segment consolidated leading position

Thursday, September 6, 2018  10741

10741

CR Pharmaceutical(3320)

| Recommendation | BUY |

| Price on Recommendation Date | $12.720 |

| Target Price | $15.200 |

Weekly Special - 1171 YANKUANG ENERGY GROUP COMPANY LIMITED

Investment Highlights

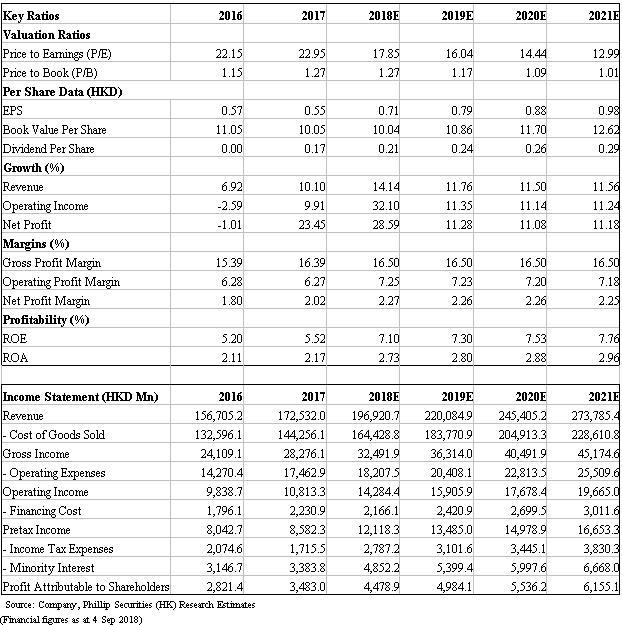

During 18H1, we see that revenue from three main segments, namely distribution, manufacturing and retail, increased by 10.2%/32.9%/16.7% yoy, respectively. We highlight that the company 1) continues to be optimize the distribution network, 2) integrates R&D capabilities on generics and innovative drugs, 3) places importance on biopharmaceuticals, and 4) boosts chemical and TCM drugs through external mergers and acquisitions. Considering impacts form two-invoice system will mitigate in 18H2 and lead to better operating results, we thus raise TP to HK$15.2, implying 19x PE for FY18. (Closing price at 4 Sep 2018)

Business Overview

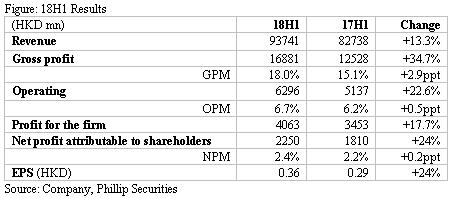

18H1 results. The company achieved revenue of HK$93,741mn, up by 13.3% yoy. Gross profit climbed by 34.7% to HK$16,881mn with GPM up by 2.9ppt to 18%. Operating profit increased by 22.6% to HK$6,296mn, while OPM increased by 0.5ppt. Significantly increased expenses is resulting from the implementation of two-invoice system, given selling expenses as a percentage of revenue increased from 6.7% in 17H1 to 9% in 18H1. Net profit attributable to shareholders increased by 24.3% yoy with NPM up by 0.2ppt.

Manufacturing business. This segment reported income of HK$16,874.5mn (+32.9% yoy). GPM was up by 3.6ppt to 63.7%, mainly due to the continuous improvement of product mix and production process. By product, 1) Chemicals recorded a revenue of HK$8,039.1mn, a rapid yoy increase of 50.9%, mainly benefiting from the increase in income from anti-infectives, infusion products, and chronic diseases and specialist drugs; 2) TCM records sales of HK$7,496.5mn, up by 19.9% yoy, attributable to the sales hike of OTC products and prescription TCM products for cardiovascular and cerebrovascular diseases, and TCM formula pellets; 3) Biopharmaceutical products generated sales of HK$88.5mn, affected by selling model adjustment, increased by 39.1% yoy; 4) Nutrition and health products benefited from the continuous enrichment of product categories thus recorded revenue of HK$306.9mn, up by 93.6% yoy.

Distribution business. In 18H1, distribution business achieved revenue of HK$77,60mn, a yoy increase of 10.2%. GPM was 7.4% up by 1.0ppt, mainly due to the direct revenue from medical institutions taking a larger portion in distribution income. For the upstream, the company speeds up the introduction of quality products, expands the import of value-added services, and optimizes product structure, as well as vigorously promotes medical device distribution business. For downstream network, it enhances distribution network in blank provinces of western China and strengthens the downstream terminal control by further infiltrating the grassroots market. Its distribution network had covered 27 provinces and municipalities across the country, including 5,857 second- and third-level hospitals, 38,954 primary-level medical institutions, and 28,916 retail pharmacies.

Retail business. This segment recorded sales of HK$2,470.4mn (+16.7% yoy), GPM was 16.3%, a drop of 0.9ppt from 17H1 level, mainly due to the rapid growth of the high-value drug direct delivery service (DTP) which has relatively low profit margin. The company further integrates retail resources in terms of brands, drug products and information systems, enriches product categories, and actively develops innovative business models such as DTP and chronic disease management. At present, the company has 812 retail pharmacies and 94 DTP pharmacies covering more than 50 cities in China.

Pipeline. R&D efforts focus on fields like cardiovascular, anti-tumor, digestive tract and metabolism, central nervous system, immune system, etc. R&D expenditure reached HK$649mn in 18H1, up by 63.5% yoy, accounting for 3.8% of manufacturing income. There are 37 existing innovative drugs in pipeline, among which one anti-tumor drug is in phase II of clinical stage. We highlight that one respiratory system drug has been initiated in China and US, and 19 projects are in registration and approval stage. Four products, including polyethylene glycol recombinant human erythropoietin injection, obtained clinical approvals. Meanwhile Baixiaoan injection and other three products obtained production approvals. These further enrich the product line for future growth. Besides, the company actively process the consistency evaluation work, given now more than 40 evaluation projects are undergoing and several projects have carried out bioequivalence clinical trials. In July, amlodipine besylate tablets (5 mg) passed the consistency evaluation.

Boost biopharmaceuticals business. The company integrates resources involving R&D, production and marketing to boost biopharmaceutical business. In June, the company and CR biopharmaceutical firm jointly funded the reorganization of a biopharma subsidiary (Angde Biotech) and shared 51% of Angde's ownership, with injection of two products of their owns. Founded in 2001, Angde was originally a wholly-owned subsidiary of Dong`e Ejiao, and has a good foundation in R&D and production capacity of recombinant protein biopharmaceuticals. The two products injected belong to recombinant protein products for diabetes, which own great market potential. It is expected to form a complete product portfolio together with Angde's own pipeline product (one insulin), and enjoy synergies involving capital, tech and distribution channel, etc. At present, there are recombinant human erythropoietin and reteplase for injection in biopharma pipeline, focusing on anti-tumor, immune, cardiovascular and cerebrovascular fields. Meanwhile, the company is to accelerate the acquisition of high-quality drugs, introduction of bio-products as well as international cooperation, in order to enhance its overall strength in biopharmaceutical field.

External M&A underpin chemical and Chinese medicine sectors. The company implements a handful of M&A projects with respect to TCM and chemical medicine segments, to enrich product portfolio and expand business layout. 1) TCM. The company will reorganize Jiangzhong Group to acquire 51% of shares of Jiangzhong Group, which owns 43.03% of Jiangzhong Pharma shares. Jiangzhong Pharma is a leading OTC product manufacturer in China. It has a high brand awareness and market share in the gastrointestinal and oropharynx fields. It is expected to cooperate with CR Pharma in various aspects such as brands, products, productions, R&D and sales network. 2) Chemical sector. In May, CR Double Crane (its chemical product platform) announced the acquisition of a 45% stake in Xiangzhong Pharma, to enrich the psychiatric and neurological drug product lines, and strengthen sales capacity towards psychiatric hospitals. In Aug, CR Double Crane announced the further acquisition of 40.65% equity of Xiangzhong Pharmaceutical. When completed, CR Double Crane will hold a total of 85.65% equity of Xiangzhong Pharma. These M&A will enhance CR Pharma's control and integration of industry chain.

Valuation and Risks

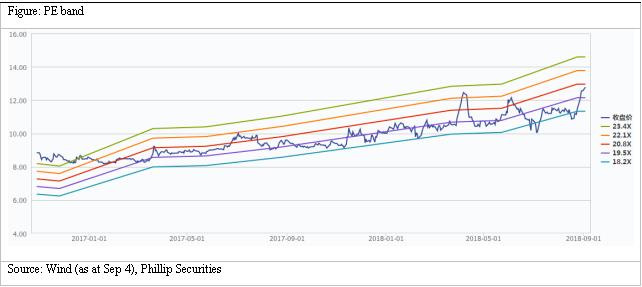

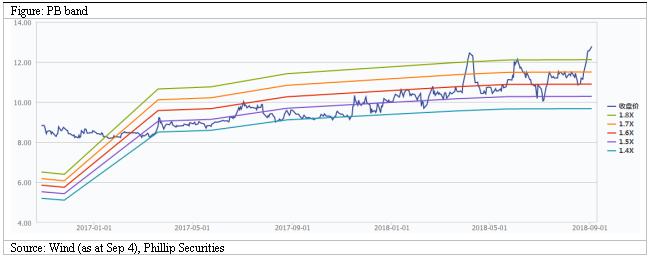

We raise our target price to HK$15.2. We forecast revenue growth rates for 18E/19E to be 18%/12%, corresponding to EPS estimates of HK$0.71/0.79 respectively. Based on a 19x target P/E, we get target price of HK$15.2. Downside risks include: R&D failure risk; distribution business growth is less than expected; policy risk.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()