-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

BYD (1211.HK) - Ups and Downs in Segments` Business; Awaiting Further Good News

Wednesday, April 12, 2017  19397

19397

BYD(1211)

| Recommendation | Accumulate |

| Price on Recommendation Date | $45.100 |

| Target Price | $51.900 |

Weekly Special - 3306 JNBY Design Limited

Financial Data Summary

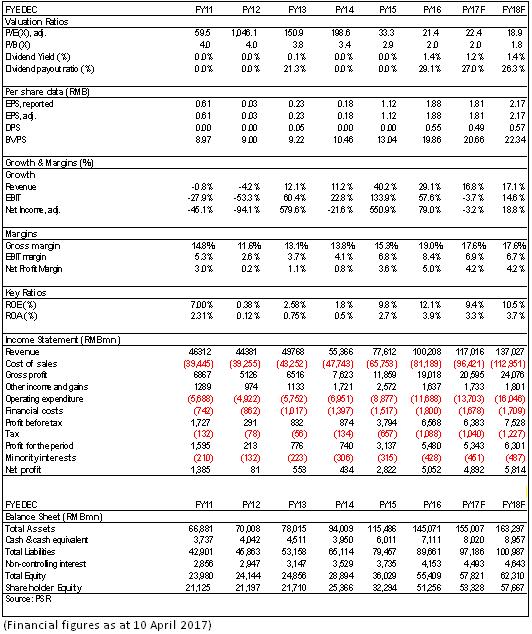

BYD reported its revenue of RMB100.21 billion in 2016, up 29.1% yoy. Profits attributable to parent company owners were RMB5.052 billion, up 78.94% yoy, with EPS of RMB1.88, DPS of RMB0.178, interim dividends of RMB0.367, total dividends of RMB0.545, and dividend payout ratio of 29%, respectively. The performance was basically in line with expectations, at the lower part of the range of 1.85 to 1.93 expected in the preliminary results.

New-energy auto-mobiles and metal cellphone components are the highlight of the annual report

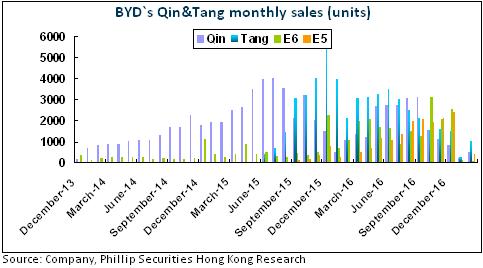

Affected by subsidy fraud investigations and policy changes, the growth in Chinese new-energy auto-mobiles declined slightly in 2016, but was still obvious. The sales of EV and PHEV witnessed an increase of 65% and 17% yoy, amounting to 409 thousand units and 98 thousand units, respectively. BYD's sales in 2016 amounted to 422 thousand units, with 326 thousand traditional fuel auto-mobiles, remaining basically unchanged; sales of new-energy auto-mobiles, amounting to 96 thousand units, up 69.85% yoy, retained its No. 1 title in the world. The annual revenue from new-energy auto-mobiles in 2016 was approx. RMB34.1 billion, exceeding traditional fuel auto-mobiles by approx. 60%, an increase of 80.97% over 2015, accounting for 34.02% of the Group's total revenue, and has become one of the core pillars of performance. BYD will continue to develop new cars in the future and expand domestic and oversea customer markets. Qin 100 and Tang 100 were put into market in February this year, including a couple of new cars that will come to market as well, such as Song phev and Yuan phev. We hold that the extended mileage will enhance the competitiveness of our products.

In the cellphone industry, the output of domestic local smart cellphones continues to be strong, and the manufacturing techniques of metal components become more mature with a gradual drop of costs, which dominates the industry trend. In 2016, the revenue of BYD cellphone components and assembly business was nearly RMB38.083 billion, up 15.65% yoy, with metal components business increasing sharply, witnessing an increase of approx. 50%.

In the rechargeable battery field, the traditional battery market develops smoothly. The development of distributed photovoltaic cells quickens obviously, the costs of components continue to decrease, and the photovoltaic cell industry see signs of sustained recovery. Competition however remains fierce. The revenue of rechargeable battery and photovoltaic cell industry is approx. RMB7.103 billion, up 23.53% yoy. It is noteworthy that the increase of this business is mainly from rechargeable batteries. The photovoltaic cell industry is still losing money in 2016.

Financial conditions improved after the accomplishment of private placement

During this period, BYD has completed private placement of A share, introduced China Advanced Manufacturing Fund and strategic investment from Samsung Group, and successfully raised approx. RMB14.473billion which enhanced its capital strength significantly. The asset-liability ratio has been reduced to 74% from 109% in 2015, and cash in hand also has increased from MRB6.3 billion to RMB7.3 billion, which provide financial support for follow-up development. However, we also notice that the account receivable jumped to RMB45.7 billion sharply owing to the longer payback period of new-energy auto-mobiles, and the payment have been prolonged by 16 days to 132 days.

New-energy auto-mobile business will face adjustment and cellphone business continues to develop fast

The company is forecasting a net profit decline of 23.6% to 35.4% in 2017. The main reasons: affected by the changes in government subsidy policies for new-energy auto-mobiles in Q1 2017, there will be adjustments in the new-energy auto-mobile industry in a short time, and this business should withstand a certain amount of stress, with a predicted drop of sales and profits. In the cellphone business, the company will continue to enlarge the output of metal shells and take great pains to develop 3D glass techniques in terms of new materials application so as to achieve sustainable increase of business. We hold the flux of auto-mobile and cellphone business will contribute to the fluctuation in company's performance.

In the downstream market, the company officially launched the straddle-type light rail products named "Yungui", hence breaking into the urban rail market. Currently, it has received orders from the Shantou municipal government and billions of revenues are projected in the next few years.

Investment Thesis

We adjusted the expected EPS of 2017/2018 to RMB1.81 / RMB 2.17 and revise the target price to HKD51.9, which corresponded to 25.8/21.8x P/E and 2.3/2.1x P/B ratio for 2016/2017. We give the rating of “Accumulate”. (Closing price as at 10 April 2017)

Risk

Sales of new energy vehicles is not as good as expected

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()