-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Zhongheng Group (600252.CH) - Xueshuantong injection will continue the high growth

Monday, January 12, 2015  13525

13525

Zhongheng Group(600252)

| Recommendation | BUY |

| Price on Recommendation Date | $16.650 |

| Target Price | $20.360 |

Weekly Special - 3993 CMOC Group Limited

Xueshuantong injection will continue the high growth

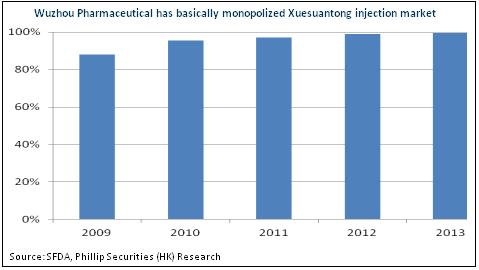

Xueshuantong was continuously selected into National Essential Drug List of the 2009 and 2012 version, and has obtained the separate pricing power from the National Development and Reform Commission with patent protection duration to the year of 2026. Thereby, in recent years, the market shares of Wuzhou Pharmaceutical Co., Ltd has been increasing continuously, and has mainly monopolized the whole Xueshuantong Injection market, becoming the largest single item of traditional Chinese medicine injection. Zhongheng Group also benefited from this. From 2004 to 2013, its revenue and operating profit respectively increased from CNY 150 million and 67 million to CNY 3.64 billion and 726 million Yuan, with the compound annual growth rates of 42.6% and 30.3% separately.

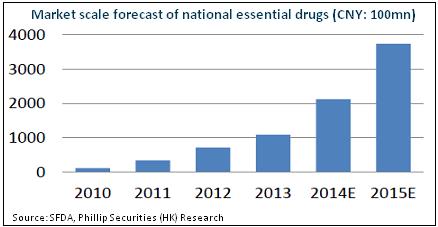

We expect that the high-growth characteristic of Xueshuantong will last. Looking from the cardiovascular and cerebrovascular medicine market that it belongs to, it will not only benefit from the general background of the continuous increase of the rate of cardiovascular disease due to aging of population, but also benefit from the extension of the proportion of essential drugs and the promotion of the rate of seeking medical advice. Regarding traditional Chinese medicine injections, they have characteristics of rapid effect, good effect for treating critical severe cases, and so on. Its clinical prescription rate is very high, even higher than that of general chemical drugs. Compared to the peer, Zhongheng's Xueshuantong is with high proportion of quantifiable ingredients, good solubility and little side effect.

The supervision department has implemented safety reevaluation and strict examination and approval policies on traditional Chinese medicine injections in recent years, and generally presenting the principle of less approval and more elimination. Therefore, traditional Chinese medicine injections with high quality standard and good safety will obtain more market shares in the future, and we believe that Xueshuantong will win more market shares from it.

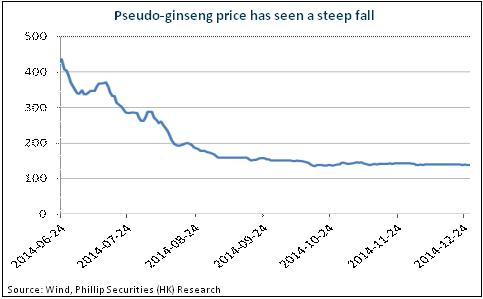

The price of pseudo-ginseng continues falling and benefits the company's profitability. Looking forwards, due to the increase of harvest area and the long planting cycle , it is expected that more pseudo-ginseng will continuously flow into the market, so the price is expected to maintain low, and its contribution to the performance will still increase.

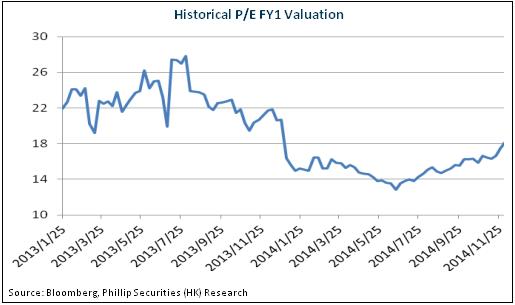

Low valuation from both horizontal and vertical comparisons

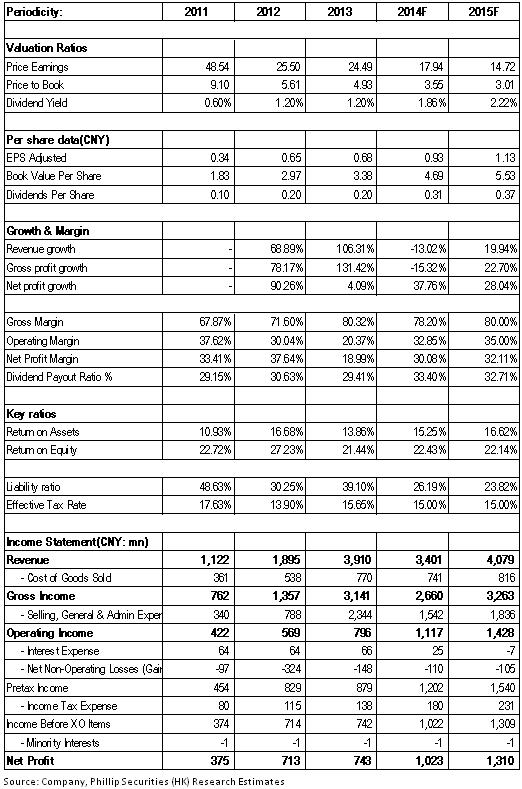

Although the product structure is relatively unitary, Xueshuantong still has pretty large market space, and is hopeful to keep medium and long-term growth. Meanwhile, more than one billion monetary capital will also support the Company to expand extension and acquisitions and cultivate back-up medicine varieties. The valuation of the Company is less than 15X P/E corresponding to 2015 EPS, a low level whether from historical comparison or peer comparison. We grant it 18X 2015EPS, and the target price can be CNY 20.36, with “Buy” rating initially.

Traditional Chinese medicine injection is the major contributor

Currently Zhongheng Group runs businesses of medicine, health food and real estate. After going through diversified development in previous years, the Company has focused on the development of pharmaceutical manufacturing industry since 2012, and gradually strips the real estate business. Wuzhou Pharmaceutical Co., Ltd, 99.99% shares hold by the Company, is the main source of revenues and profits, and Xueshuantong injection (freeze-drying) is the leading product. In 2013, the revenue and gross margin of Xueshuantong series occupied respectively 87.1% and 94.5% of the total revenue and gross margin of the Company.

It's worth pointing out that the variety was continuously selected into National Essential Drug List of the 2009 and 2012 version, becoming one of the only 8 kinds of traditional Chinese medicine injections. Also, as the exclusive variety of essential drug and Class A medical insurance list, Xueshuantong injection obtained the individual pricing power from the National Development and Reform Commission with patent protection duration to the year of 2026. Depending on this dominant competitive position, the market shares of Wuzhou Pharmaceutical Co., Ltd is increasing continuously, and has mainly monopolized the whole market of Xueshuantong injection, becoming the largest single item of traditional Chinese medicine injection in term of sales volume. The Company also benefited from this. From 2004 to 2013, its revenue and operating profit respectively increased from CNY150 million and 67 million to CNY 3.64 billion Yuan and 726 million, with the CAGR of 42.6% and 30.3%.

The high growth trend will keep on

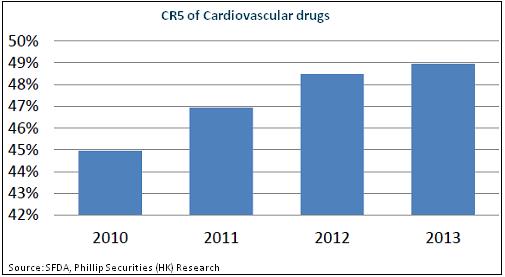

In general, we expect that the high-growth trend of Xueshuantong will last. Looking from the cardiovascular and cerebrovascular medicine market that it belongs to, it will not only benefit from the general background of the continuous increase of the rate of cardiovascular disease due to aging of population, but also benefit from the extension of the proportion of essential drugs and the promotion of the rate of seeking medical advice. Among them, although chemical drugs still holds the dominant position, Chinese patent medicine are being widely used depending on its unique advantages such as multiple targets and little toxic and side effect, and its market shares rise continuously. According to the statistics, the compound annual rate of growth of cardiovascular and cerebrovascular drugs in the market was 21% from 2010 to 2012, among which the compound annual rate of growth of traditional Chinese medicine reached up to 28.8%.

Traditional Chinese medicine injection has characteristics of rapid effect, good effect for treating critical severe cases, and so on. Its clinical prescription rate is very high, even higher than that of general chemical drugs. Among them, Xueshuantong has characteristics of high proportion of quantifiable ingredients, good solubility and little side effect comparing with similar varieties. After the improvement of new process, the quantifiable ingredients reach 97.2%. It is not only the highest level in injections of extracts of pseudo-ginseng kind, but also starts to approach the proportion of quantifiable ingredients of chemical drugs. In addition, as the unique variety of the national essential drugs, Xueshuantong enjoys the individual pricing power. It maintains the terminal price well, and the list prices in the histories of all places were pretty stable, which sets aside more profit margins for channels, and contributes to maintain reasonable sales model.

It is particularly worth mentioning that the supervision department has implemented safety reevaluation and strict examination and approval policies on traditional Chinese medicine injections in recent years, and generally presenting the principle of less approval and more elimination, which will promote the upgrade of the quality standard of this industry. Therefore, traditional Chinese medicine injections with high quality standard and good safety will obtain more market shares in the future, and we believe that Xueshuantong will win more market shares from it. In the first three quarters of 2014, the Company continued the high-growth trend. The sales volume of Xueshuantong reached 207 million with year-on-year growth of 30%. We expect that it will maintain more than 20% of the growth in the following two or three years.

Moreover, the Company is building two production capacities in Nanning and Zhaoqing, which are expected to start to release the production capabilities this year and reach the design capacity in 2018. Therefore, its total production capacity of Xueshuantong will increase 133% to 700 million per year, thereby solving the bottleneck of production capacity, and then supports the medium and long term growth of the Company.

The profitability will benefit from the dropping price of pseudo-ginseng

Pseudo-ginseng is the main raw material of Xueshuantong injection. Since 4Q13 the price of pseudo-ginseng continues falling, and the extent reaches up to 50% to 60%. Therefore, the material cost can reduce significantly and benefit the company's profitability. The sales volume of the Company of the first three quarters increased 30%, meanwhile the net profit excluding extraordinary items increased significantly about 40%. Looking forwards, due to the increase of harvest area and the long planting cycle of pseudo-ginseng, it is expected that new products will continuously flow into the market, and the price of pseudo-ginseng is expected to maintain low, so its contribution to the performance of the Company is expected to increase.

Catalysts

The performance from traditional Chinese medicine injection is beyond expectation;

Advances in epitaxial expansion and acquisition.

Risks

The sharp decrease of the retail price of Xueshuantong;

New production capacity releases less than expected.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()