-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Jiangsu Hengrui Medicine (600276.CH) - To enter into the harvest season as the benchmark of innovation

Wednesday, December 3, 2014  20632

20632

Jiangsu Hengrui Medicine

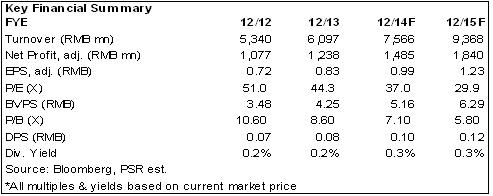

| Recommendation | Accumulate |

| Price on Recommendation Date | $36.750 |

| Target Price | $43.040 |

Weekly Special - 2333 Great Wall Motor

Since its launch, the performance of Jiangsu Hengrui Medicine (Hengrui) has experienced the change from growing rapidly to growing steadily. The Company has adjusted the strategy in time, which has been shifted from "transition from genetic drugs to innovative drugs" in the past into "pay equal attention to both generic drugs and innovative drugs". Numerous new varieties of generic drugs for reserve use have been applied for approval. Since the second half of last year, generic drugs have also entered into a new round of approval-granting climax. It is expected that in the next five years, 3-5 generic drugs of the Company will be approved annually. These varieties do not have a intense market competition, and thus they will assist in enriching the product lines of the Company effectively.

The approval of imrecoxib earlier marked the Company's official entering into the innovative drugs era, while the approval of apatinib in early November is the sign that the Company has fully entered into the harvest stage of innovative drugs, the potential market scale of which in the field of gastric cancer is expected to reach the level of RMB 1 billion. In the meantime, the indication for liver cancer is also in clinical trials. We do not exclude the possibilities that it will permanently be above the level of RMB 2 billion. It is worth mentioning that the approval of apatinib opened a new chapter of the Company's innovative drugs. The subsequent products such as 19K and famitinib are also expected to be approved in succession.

Recently, the cyclophosphamide for injection of the Company has passed the accreditation of U.S. FDA, and it will be available in the U.S. market. This drug has a sound competition pattern. By its good competitive landscape, the Company is expected to increase the sales volume of this alternative drug quickly. The integrated anticipation is that the company's export of preparations will result in a billion Yuan in 2015.

The overseas accreditation for the series products of the Company not only helps the Company to expand the market, but also is propitious for the Company to win a better pricing power in the public bidding for drug products. Plus the bidding rules of the Mainland China tend to be softened in recent years, we expect that in the future, the major products of the Company will have a big probability of not being again under the pressure of sharp price slashing.

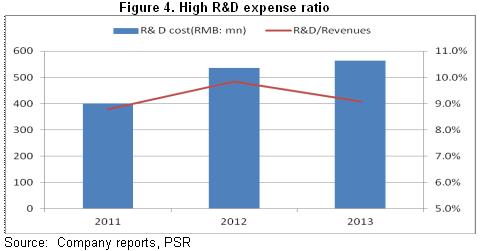

Annually, approximately 10% of the revenue is being used for research and development by the Company, which is basically on a par with that of transnational pharmaceutical enterprises. The R&D strength is outstanding. Moreover, the Company also has a highly qualified professional marketing team, which is actively in promoting moving down the distribution chain closer to consumer. In the future, it will strengthen the efforts of marketing promotion in county hospitals and community hospitals of big cities, so as to provide new growth points for the sales revenue.

Investment Action

Hengrui Medicine is a rare company in this industry that achieved a steady growth. Also it has powerful cash flows and extremely low leverage ratio, which proved the robust management style of the Company. After more than 10 years of research and development investment, several new important drug varieties of the Company are expected to start increasing the sales and overseas markets will also be released, which will speed up the growth of the Company's performance. Regarding the future development, in addition to the leading position in the markets of antitumor and surgery drugs, the Company's in-development products for diabetes, cardiovascular disease and so on will be also on the market, which will enhance its feature of broad disease spectrum and widen the Moat Effect.

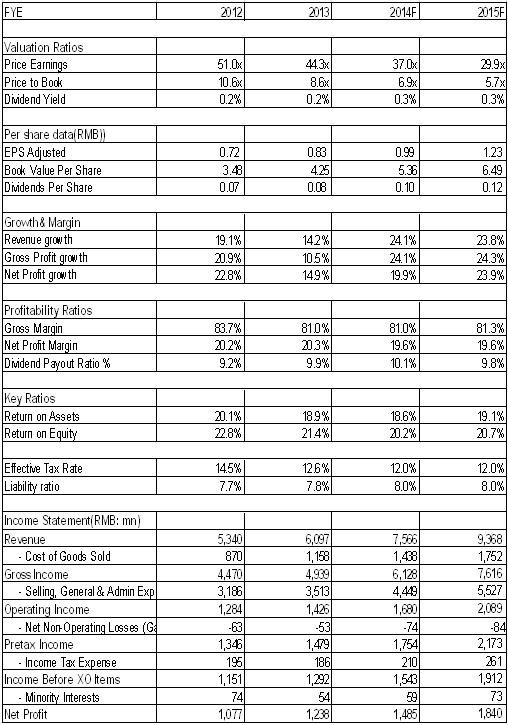

In general, the Company will form a new prospective in the future, in which the triple arrows of innovative drugs, new varieties of generic drugs and overseas sales of pharmaceutics will be shot out at the same time and thus promote the growth. Furthermore, in view of its benchmark position of innovation in Mainland China, we give the Company a corresponding P/E ratio valuation of 35 times for 2015 EPS with a 12-month target price of RMB 43.04, and grant the Company the rating of "Accumulate".

The pressure of growth inspires the strategic shift

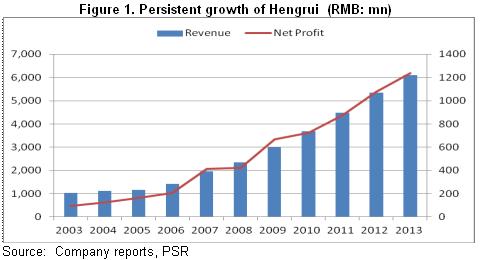

Since its launch, the performance of Hengrui has experienced the change from growing rapidly to growing steadily. From 2003 to 2008, after stripping off the low-margin packaging business and common drug business, its revenue increased from RMB 1.05 billion to RMB 2.39 billion with the CAGR of 18%, while deducting non-recurring gains and losses, the net profit increased from RMB 85 million to RMB 570 million with the CAGR as high as 46%. This mainly benefited from: sub-industries such as antitumor drugs and anaesthetics were in a rapid-growing stage, both of which kept a fast growth rate of over 30%; the Company gets hold of major varieties such as oxaliplatin, docetaxel and irinotecan, and shares the opportunities of import substitutions for the generic drugs` major varieties with limited competitors and sound competition patterns.

Since then, the performance of the Company has stepped into the period of steady growth. From 2009 to 2013, the revenue increased from RMB 3.03 billion to RMB 6.2 billion, with the CAGR of 19%; after deducting non-recurring gains and losses, the net profit increased from RMB 580 million to RMB 1.22 billion with the CAGR of 20%. Aside from being restrained by the strict approval of generic drugs, longer time to market of the new products and so on, the performance growth slowed down was also a result of the Company's over-leaning towards innovative drugs, which resulted in overlooking the varieties of the generic drugs for reserve use and thus caused a fault in the echelon of the product line.

In order to get out of such dilemma, the Company has adjusted the strategy in time, which has been shifted from "transition from genetic drugs to innovative drugs" in the past into "pay equal attention to both generic drugs and innovative drugs". Numerous new varieties of generic drugs for reserve use have been applied for approval. According to statistics, there are no less than 70 major varieties of the Company under development in recent two to three years, among which, more than 20 varieties are belong to the first class new drug, nearly 30 varieties are belong to third class new drug, and nearly 20 varieties are belong to the sixth class generic drugs. Aside from the traditional superior fields such as antitumor, anaesthesia and radiography, the product lines have also been expanded to several potential major disease fields such as diabetes, cardiovascular disease, super antibiotics and hematological system. The issue of product lines which has restricted the Company from development has been solved gradually.

The product group's sales volume will be enhanced

Hengrui is the benchmarking enterprise of innovative medicines, which so far has worked more than 10 years in the field of new drug research and development. Before then, the approval of Imrecoxib marks that the company has officially stepped into the era of innovative medicines, and the approval of Apatinib in early November marks that it has comprehensively entered into the harvest period of innovative medicines. This variety is the first micromolecule anti-angiogenesis targeted drug proved safe and effective for advanced carcinoma of stomach all over the world, and it is the only preparation taken orally in targeting therapy against gastric cancer, expected by us to be on the market in the first quarter next year. At the moment, at home, about 160 thousand people die due to advanced gastric cancer. Assuming 30% patients take Apatinib for 2 months of treatment, costing around 10 thousand per month, Apatinib's potential market's scope in the field of gastric cancer is expected to reach the level of 1 billion. Meanwhile, Apatinib liver cancer indication is in clinical trials, and among which, we do not rule out that it can become major varieties with great values above the 2-billion level for a long term. It is worth mentioning that the approval of Apatinib starts the new page of the company's innovative medicines. The following 19K, famitinib and so forth are anticipated to be approved as well.

In addition, a big amount of the company's generic drugs will also start to show its advantages. In the past 4 years, the company has declared over 70 generic drugs. Starting from the second half year of last year, generic drugs have embraced the new turn of being approved. Febuxostat Tablets for treating gout, Capecitabine Tablets for treating tumor and Palonosetron for stopping vomiting in chemotherapy have been approved, benefited from abundant varieties in developing. It is expected that in the future 5 years, Hengrui will have 3-5 generic medicines approved every year. These varieties do not have a intense market competition, and thus they will assist in enriching the product lines of the Company effectively.

The market abroad is likely to rapidly extend

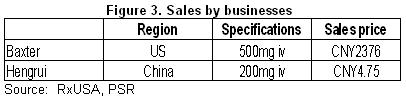

Hengrui is currently the only Chinese pharmaceutical company that has passed the FDA Injection evaluation. From 2011-2013, Irinotecan Hydrochloride for injection and Letrozol Tablets passed the FDA Certification, and Oxaliplatin for injection was brought to the market in European Union in 2012. Recently, the company's Cyclophosphamide for injection has passed America FDA Certification, and will be sold on the American market. In the future, Gabapentin Capsules, Docetaxel Injection and Sevoflurane Inhalation are expected to pass the FDA Certification.

Although Cyclophosphamide is an old variety, only Baxter sells it, so the competitive landscape is promising, and Sandoz, the company's partner in the United States, possesses a relatively mature marketing channel in the United States, sweeping off obstacles in the marketing aspect. The company is expected to rapidly make replacement and great sell with the support of its price advantages. According to the data statistics of IMSHealth, this variety's marketing in the United States reaches 420 million dollars, which can be regarded high value. The integrated anticipation is that the company's export of preparations will result in a billion Yuan in 2015.

What requires to be pointed out is that, the company's series of products passing overseas certification not only extend the market but also are good for the company to fight for a better pricing right in medicine bidding, and further defend the price system of traditional products. Besides, in recent years, most of the provinces` bidding rules are moderate in the Mainland, we predict that in the future, the company's featured products are not inclined to suffer from pressure of slashing depreciation.

Prominent competitive advantages

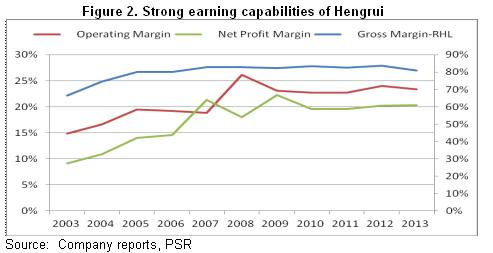

Compared with the same industries at home, the proportion of the company's annual investment spent on research and development in revenue is about 10%, which is basically comparable to multinational pharmaceutical companies. The company has established centers of research and development in Lianyungang, Shanghai, Chengdu and the United States and a clinical department of medicine, possessing over 1200 high-level professionals of all types, among which there are over 500 doctors and masters, 48 people who studied abroad and 4 are listed in the state "thousands of people plan". Thereby, when it comes to the development of innovative medicines, the company basically forms the optimum developing status of multiple investigational drugs application and 1-2 innovative drugs brought to the market every year. In general, the company poses prominent power of research and development.

Moreover, the company also has high-quality and professional marketing teams. In addition to establish complete marketing system in middle and high-end medical institutions, the corporation also actively promotes to subside marketing channels, specifically proposes to promote the marketing thinking of "three-year development plan of county-level markets" in the annual report of 2012. In the future, it will enhance its marketing and promotion strength in county hospitals and metropolises` community hospitals, in order to provide the marketing income with new points of growth.

In addition, the company also owns advantages concerning brand and quality and is ahead of others in fields of antineoplastic and medicines for operation. The company's raw and auxiliary materials meets or higher than the regulated standards of European Union and the United State's pharmacopeia. At present, all of its preparations have passed the national new GMP Certification, and 5 raw materials as well as 5 preparations passed America FDA Certification and European Union Certification, emphasizing the high standard of the company's products.

Catalyst

A series of drugs get approval;

Unexpected sales volume of innovative drugs

Risk

The bidding price get lower;

New drugs are not approved as expected.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()