-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

HC INTERNATIONAL (2280.HK) - Positive profit alert in falling stock price, a buying opportunity

Thursday, November 6, 2014  13592

13592

HC INTERNATIONAL(2280)

| Recommendation | Buy |

| Price on Recommendation Date | $8.800 |

| Target Price | $14.920 |

Weekly Special - 2333 Great Wall Motor

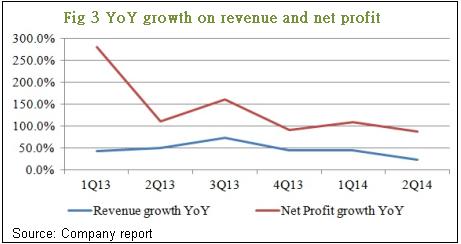

-HC Intl issued positive profit alert for its 3Q results, which net profit and revenue for the first nine months were expected to grow over 50% yoy and 20% yoy respectively.

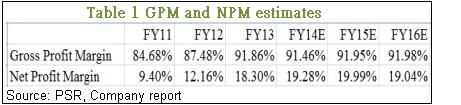

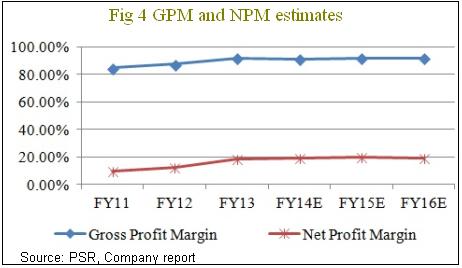

-Both the GPM and NPM increased steady from 84.7% and 9.4% in 2011 to 94.7% and 22% in 1H14.

-Stock price dropped since the first quarter, the current price is about the same as of one year ago when forecasted profit growth is 37%, implied attractive valuation.

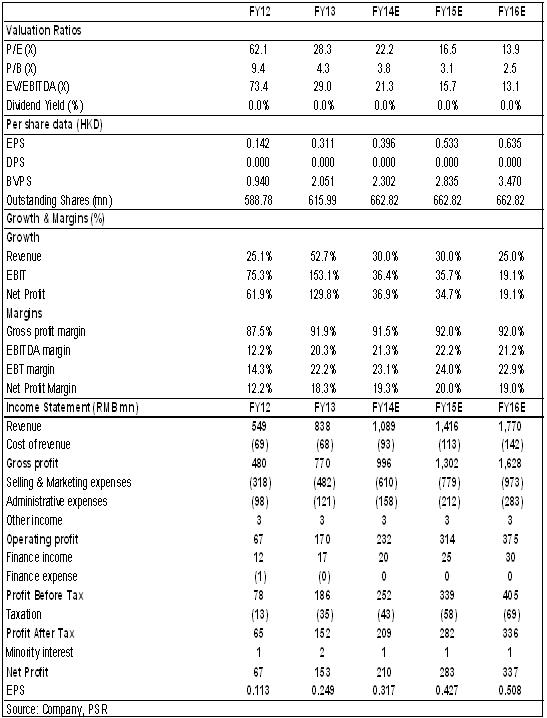

-We initiate the rating of HC Intl as “Buy” with target price of HK$ 14.92, equivalent to 37.7x/28x of 2014 and 2015 forecasted EPS.

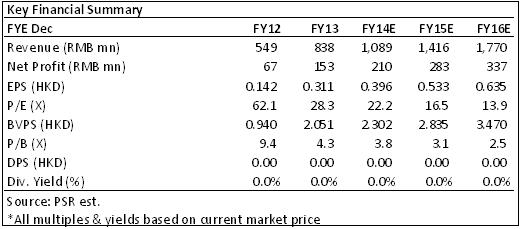

Financial Highlights

HC International had issued positive profit alert for its 3Q results, which net profit and revenue for the first nine months were expected to grow over 50% yoy and 20% yoy respectively. The growth seemed slowing down from the interim results of which profit and revenue up 95.8% yoy and 30% yoy respectively. However, in the past few years, the gross profit margin and net profit margin increased steady from 84.7% and 9.4% in 2011 to 94.7% and 22% in 1H14, implied strongly improved profitability.

How we view this

HC Intl had just transferred from HKEx GEM board to the main board at Oct 10, 2014. However, the stock price suffered from serious selling pressure afterwards. We could not find the reason of price drop from its financial statements, which showed solid growth in the past few years. One of the explanations might be that investors were concerning on the slowing down of revenue and profit growth. Another reason we thought was the fund outflow in the software sector, which many of the well performing companies were suffered since the first quarter this year.

Investment Action

In our view, we believe the price drop was overreaction of the market since the current price is about the same as of one year ago, with net profit up over 50% yoy for the first three quarters. Coupled with the company’s steady performance in the past few years, we tend to believe the current price undervalued. Thus, we give an initial rating to HC Intl as “Buy” with target price of HK$ 14.92, equivalent to 37.7x/28x of 2014 and 2015 forecasted EPS.

Business

With the largest shareholder Digital China (861.HK), HC Intl was focused on the SME B2B e-commerce in the mainland, which provided transaction and business information online platform ”hc360.com”, to match its buyer and seller clients. Revenue was coming from subscription fee from paying users as well as online advertisement income.

The primarily online products included Biao-Wang Search, Mai-Mai-Tong, Cai-Gou-Tong, Micro-Portal online and HuiFuBao.

Biao-Wang Search: Cooperated with search engine service providers like Baidu, 360 Search, Sogou and Google for SMEs to promote their brand names. There was also the mobile version.

Mai-Mai-Tong: A trading platform for SMEs to display product, precisely search/ match demand quickly, tailor-made services and direct sales. There was a new version, which build up micro shops at Wechat that end clients were able to access the shops by mobile terminals.

HuiFuBao: On-line B2B transaction service, which facilitated high value payment and improved the payment security.

HC – Minsheng e-Loan Credit Card: clients could apply business credit card to Minsheng Bank for trading purpose based on their creditworthiness on hc360.com.

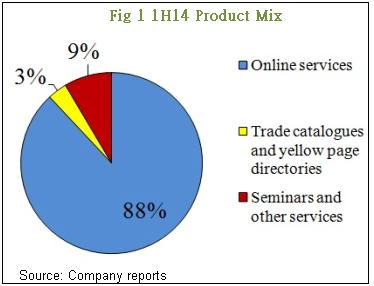

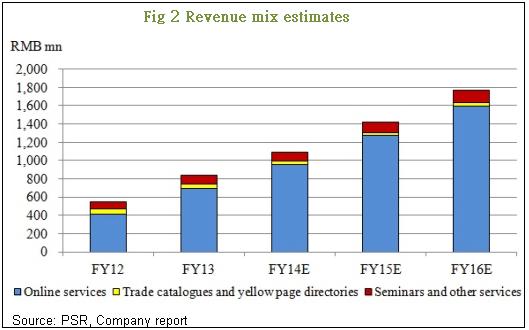

Offline products included the Trade Catalogues and Yellow Page Directories, which provided market and corporate information with its huge database, and trading fairs and seminars.

The revenue proportion of online service increased steady to 88% in 1H14, while the revenue from trade catalogues and yellow page actually fell during these years.

In the future, we expect the proportion of online service revenue continues to increase, revenue from seminars stays flat, while revenue from trade catalogues and yellow page will decline.

Growth slowed down while margins improved

From the positive profit alert, the growth on revenue and net profit for the first three quarters will reach over 20% and 50% yoy. However, the growth slowed down when compared to the 30% and 95.8% yoy in the interim results. And it became more obvious when compared to the yoy growth for the previous quarters.

Although the growth rate dropped, profitability improved which both of the gross profit margin and net profit margin increased steady. It was expected that the margin rates would become stable in the next few years.

On hand sufficient cash for further M&A activities

As at 1H14, the company held on hand over RMB 970 mn cash. After netting the current liabilities, there was still over RMB 300 mn cash for M&A activities. The company had announced at the end of September to acquire 56% stake of Panpass Information Technology with consideration of RMB 108 mn, and would establish a joint venture Zhejiang Huicong with Hui De, which principally engaging in investment in real estate.

Potential Risks

Growth online service slows faster than expected;

Increasing micro-credit loan raises the risk on doubtful loan.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()