-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Beijing Capital Land (2868.HK) - Positive outlook in 2015

Friday, February 13, 2015  11787

11787

Beijing Capital Land(2868)

| Recommendation | Accumulate |

| Price on Recommendation Date | $3.640 |

| Target Price | $4.000 |

Weekly Special - 2333 Great Wall Motor

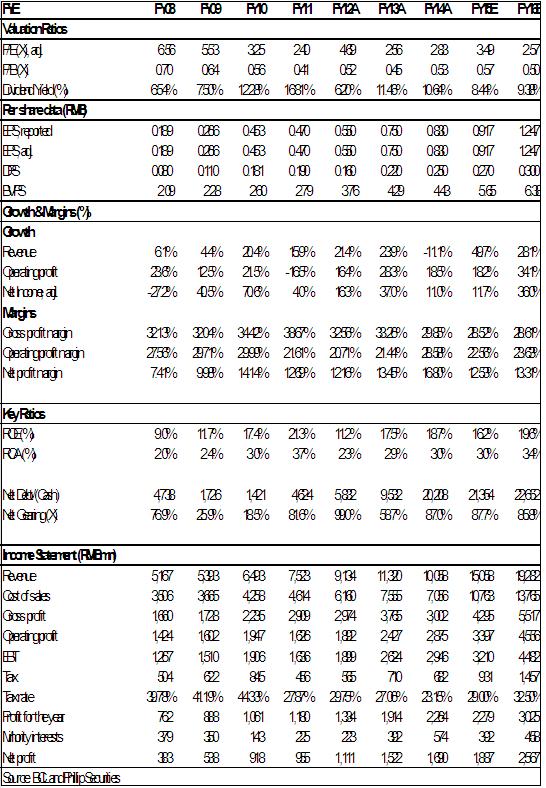

-The revenue of BCL dropped by 11% yoy and reached RMB 10.06 billion in 2014 and the net profit rose up 18.3% yoy and reached RMB 2.26 billion. During that period, the gross profit rate dropped by 3.3% and reached 24.1% while the net profit rate rose up 5.6% and reached 22.5%. The drop of the entry income and gross profit rate reflected that BCL had a weak performance in the profit and loss statement of 2014, while the obvious increase of investment income and the income of jointly operated companies promoted the double-digit increase of the profit in the end of the year.

-The contract sales of BCL rose up 26.8% yoy from 2013 to 2014 and reached RMB 24.8 billion, creating a new peak. The amounts of sales of five core cities summed up to RMB 16.8 billion, accounting for 70% of the total sales. The great surprise came from Sydney, Australia, whose sales of the whole year reached 2.2 billion, accounting for 9%.

-The land investment cost of BCL reached 19.4 billion in 2014, rising up 66% compared with that in 2013. The covered area of the lands it obtained was 2.74 million square meters, rising up 25% yoy. The lands that the Company obtained in Beijing and Shanghai were 930 and 430 thousand square meters respectively, strengthening its market share and influence in Beijing and Shanghai.

-The book cash of the Company in the end of 2014 was 13.9 billion, rising up 22.6% compared with that in 2013. The scale of the total debts increased to 32.5 billion and the scale of net debts increased to 20.2 billion with the net debts ratio of 87%, rising up 28.5% compared with that in the end of 2013. While the capital expenditure maintains tensioning, BCL well manages its balance sheet and continues broadening its financing channels.

-The three product lines of BCL continuously show its power, which are the residential sales in the core cities, the continuous expansion of Oteri J and mining the huge potential in overseas markets. We believe that the sustainable growth capacity of the three product lines is stronger, and the growth performance visibility is higher, with the capacity to drive the core performance growth.

-We believe that the prospect of BCL in 2015 is positive, the Company's product lines and development strategies can adapt to the current market situation, and the Company has stronger executive ability, which makes the visibility of its business prospects in 2015 and achieving the sales targets higher. However, we also believe that the higher capital expenditure makes the Company have more risk exposure, which reduces the attraction of the value underestimation of BCL. We give BCL the "Accumulate" rating, with the target price of 4 HKD in the next 12 months, which is equivalent to 3.5 times and 3.2 times expected P/E in 2015/2016.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()