-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

China auto sector Quarterly report - Pick the best among the good

Thursday, May 18, 2017  14152

14152

China auto sector Quarterly report

| Recommendation | Market Perform |

Weekly Special - 2333 Great Wall Motor

I. Situation review of auto industry in 2016 and the first quarter of 2017

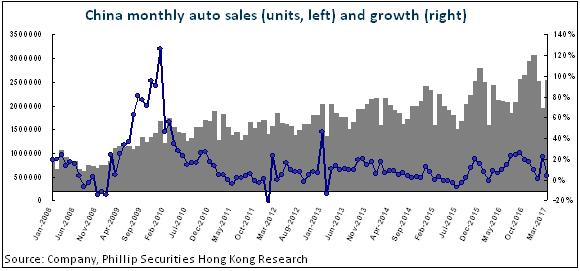

Under the guidance of policy motivation and demand preference, after two years of growth rate at single digit, China's auto market in 2016 bounced back to the growth rate of double digit. The output and sales volume reach 28.12 million and 28.03 million, respectively, a year-on-year increase of 14.5% and 13.7%, respectively, making a new historical record.

Passenger vehicle increases to 24.38million units, up 14.9% yoy, mainly affected by halving low-emission purchase tax and SUV consuming trend.The privilege range of purchase tax in 2017 decreases from 1/2 to 1/4, which weakens the stimulus effect of the privilege. Besides, the hot auto market in 2016 partly overdrew the demand in the next year and the cardinal number increases. As a result, the growth rate of sales volume in the first quarter of 2017 slowed down to 5.1%, 5.95million units, a relatively low growth rate in recent years.

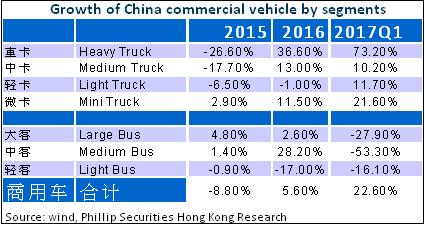

With the pull of trucks, the growth rate of commercial vehicle in 2016 bounced back by 13.4 ppts, from 9% down in 2015 to 5.8% up, with the sales volume of 3.65 million units. The significant growth in commercial vehicle is mainly pulled by medium-heavy truck. The reasons are: 1. the new emission standard of medium-heavy truck will be carried out; 2. The implementation of new rules against overloading increases demand for medium-heavy trucks; 3. The rebound of bulk commodity such as coal brings more transport demand.

The favourable factors of medium and heavy trucks are continuing in 2017. Under the influence of low cardinal number, the growth rate of commercial vehicles in the first quarter exceeded that of passenger vehicles, up 22.6% yoy to 1.05million units.

II. Industry competition analysis and industry prospect

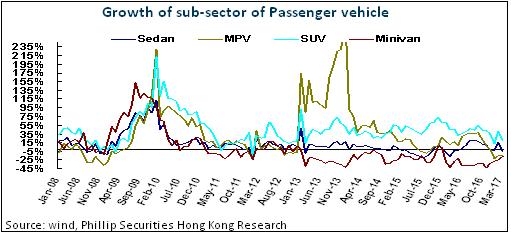

1. Passenger vehicle SUV is upsurging

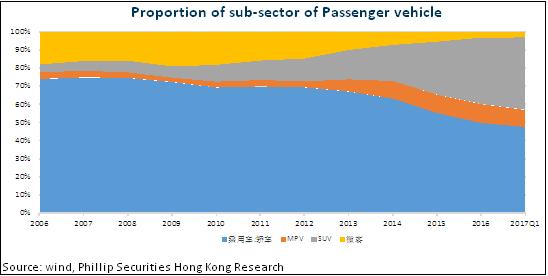

The consuming upsurge of SUV is continuing, with yearly sales volume in 2016 grew by 45% to nearly 8.94 million units. The sales percentage of SUV in passenger vehicle increases from 10% in 2010 to 37%. In the first quarter of 2017, the percentage increases to 40%. The sales volume of sedan in 2016 was about 12.14 million units, up 3.8% yoy. The growth rate turned positive, up by 8.6 ppts, but the proportion in passenger vehicle market decreases gradually from 68% in 2010 to 50%. Cross-type passenger vehicle decreases by 34% yoy to 720,000 units. The percentage of cross-type passenger vehicle decreases year by year to 3%. The sales volume of MPV is about 2.5 million.

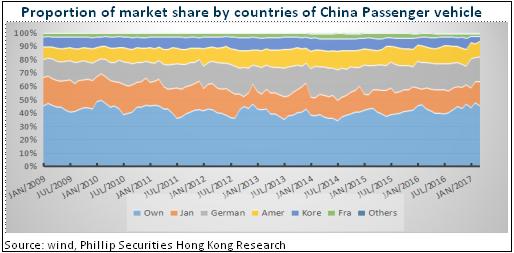

2. Self-owned brand rises with differentiation. Japanese brands revive while Korean and French brands slide down

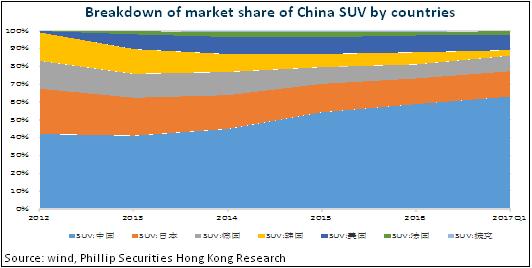

At first, self-owned brand is improving, shown in market shares, top 10 brands and profitability. In 2016, the market share of self-owned brand passenger vehicle reached 43.2%, up by 2 ppts yoy, expanding market for two years in a row. In the first quarter of 2017, the share keeps increasing to 45.7%. In the top ten auto enterprises in the passenger vehicle market, manufacturer of self-owned brand increases. From 2012 to 2014, only one self-owned brand is listed, two in 2015 and three in 2016.

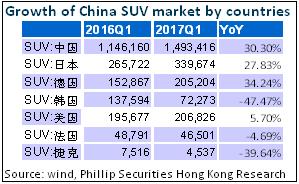

The main drive of the rise of self-owned brands is the motivation of self-owned brand SUV. 5.27million units of self-owned brand SUV were sold in 2016, up 55% yoy, accounting for 59% of overall sales volume of SUV. French brands had the slowest increase in sales volume, basically unchanged. Self-owned brand took up 6 in top 10 SUV models in sales volume in 2016, far exceeding other joint ventures. In the first quarter of 2017, self-owned SUV keeps rising, up 30% yoy.

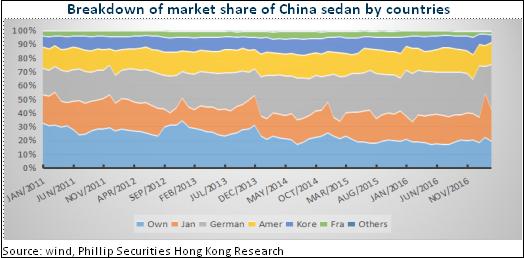

Except the popularity of SUV, self-owned brand in sedan did not perform well. Yearly sales volume in 2016 decreased by 3.7% yoy. Germany and Czech brands grew fastest (+11.5%, +18.4%), followed by American brands (+5%) and Japanese brands (3.6%). Korean brands performed worse (-3%) and French brands the worst (-16%). Another feature of such rise is the exacerbating differentiation among self-owned brands. The gap between the first tier and the second tier is increasing. Self-owned auto enterprises such as Geely (+48%), Great Wall (+29%), Changan (23%), SAIC (89%) and Trumpchi (+96%) take up higher market share. As for self-owned brands in the second tier, except for the rise of market share of Zotye, the market share of JAC, FAW Car, Haima Automobile and Chery decreases.

3. Consumption upgrade is on

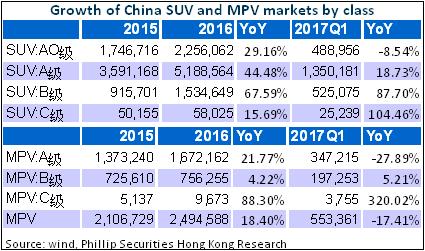

Taking SUV and MPV market as an example, the tendency of car consumption upgrade is more evident. Compared with A-level and A0-level SUV, the sales increase trend of high-level SUV is more fierce and market share increases (the market share of B-level SUV increased by 3 ppts in 2016 and 5 ppts in the first quarter of 2017; the market share of C-level SUV increased by over 100% in the first quarter of 2017), leading to less market share of low-level SUV (A0-level). The MPV market is the same. Due to the small cardinal number, C-level MPV market increases fastest and market share keeps expanding. A-level MPV is an absolute majority, but the growth rate and market share in 2017 is decreasing.

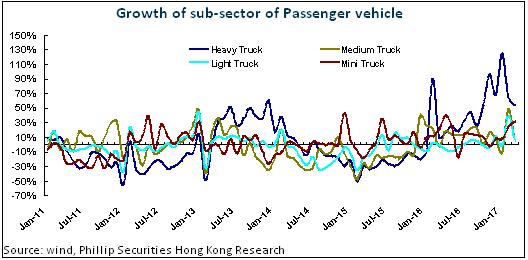

4. Heavy truck rebounds fiercely

From varieties of commercial vehicles in the market, the growth rate of truck rebounds significantly. Particularly, medium and heavy truck market rebounded in 2016 and the growth rate increases at the beginning of 2017. Overall, the competition in heavy truck market does not change much. Due to the advantage of high power traction market of FAW Group, the market share increases strongly, while other heavy truck enterprises (except Shanxi Heavy Truck and JAC) take up less market share. Passenger vehicle demand is low and decline expands: down 8.7% in 2016 and 21% in 2017 Q1 (light passenger vehicle declined most in 2016 and large and medium passenger vehicle declines evidently in 2017). New energy passenger vehicle subsidy cheat and subsidy decline mechanism affected large and medium passenger vehicle market greatly. It is expected that the passenger vehicle market will enter a round of shuffle.

5. Industry prospect

It is expected that in the second and third quarter of 2017, the growth rate of auto sales volume will keep shrinking (even zero increase may appear in some months). The exit of annual policy will accelerate the speed again. Yearly increase is about 4%-5%. Small-emission vehicle in 2018 will decline. The replacement of high-level SUV for sedan will be more evident.

III. Auto industry investment strategy: pick the best among the good

1. Segment performance and valuation analysis

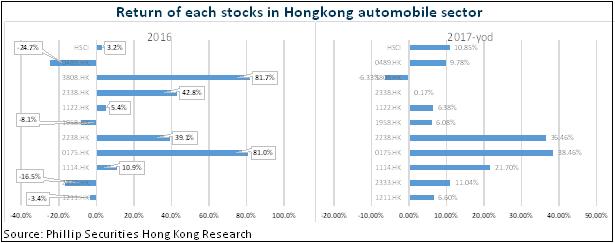

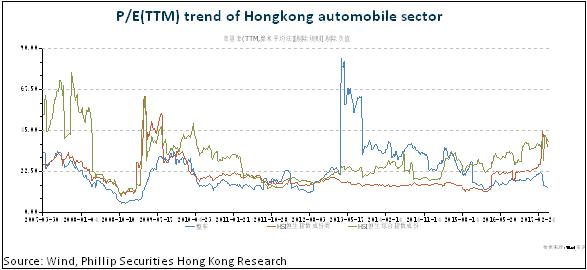

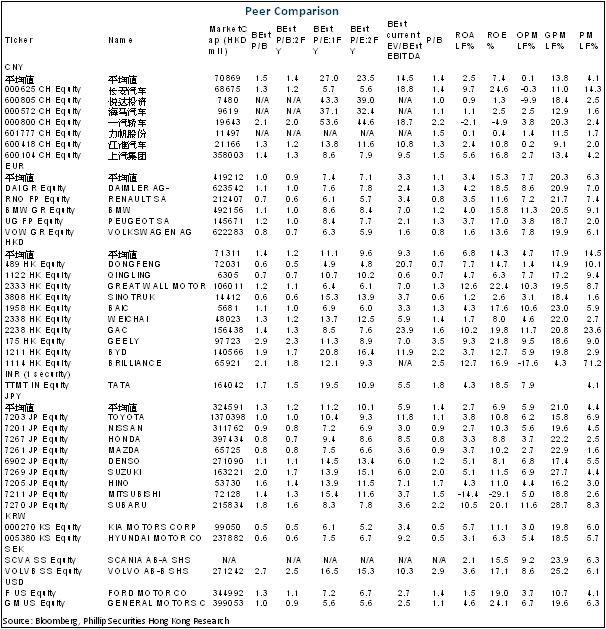

Auto segment of Hong Kong Stocks outperformed market indexes in 2016. Performance of individual shares differentiated. Up to now in 2017, especially from April with the profit taking of auto stock, the difference between stock price in auto industry and the Hang Seng Index significantly narrows. In terms of valuation indicators, in 2016, whole vehicle industry of Hong Kong Stocks rose from 13 times at the beginning of the year to 18 times at the end of the year. In the first quarter of 2017, auto valuation keeps rising to 21 times. With stock price profit taking in April, valuation falls back to 13 times. The falling space is more limited.

2. Investment strategy and enterprise selection

We think that under the guidance of policy and function of consumption preference, differentiation will be the mainstream in future development of auto industry. The sales of SUV will keep high growth rate. In particular, the demand for medium and large SUV is expected to explode. High-quality growth stock is still the direction of capital flow. It is suggested that high-quality enterprises of strong product cycle be paid attention to. We are optimistic about "Self-owned loss reduction+joint venture new SUV cycle" of SAIC and "self-rise +Japanese brand rebound" of GAC. Lyngk&co Brand that booms on accumulated strength and Geely Auto with evident product upgrade effect are recommended.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()