-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Shuanghuan Driveline(002472.CH) - Accelerated Overseas Expansion and Diversified Product Portfolio Advance in Tandem

Wednesday, July 2, 2025  1376

1376

Shuanghuan Driveline

| Recommendation | Accumulate |

| Price on Recommendation Date | $31.270 |

| Target Price | $35.000 |

Weekly Special - 002472.CH Shuanghuan Driveline

Company profile:

Shuanghuan Driveline specializes in the manufacturing of gear transmission products, with the gear business accounting for about 80% of the Company's total business. The Company has gradually shifted from traditional gear products to high-precision gears and parts. Its main products span gear products (gears for passenger vehicles, commercial vehicles, engineering machinery, motorcycles and electric tools), reducers and other products, which are mainly applied in the electric drive systems, gearboxes and axles of vehicles, as well as electric tools, rail transit, wind power, industrial robots and other sectors. The Company operates five production bases in Zhejiang, Jiangsu, Chongqing, Dalian and other places.

Investment Summary

Strong Performance in New Energy Business Drives Rapid Net Profit Growth

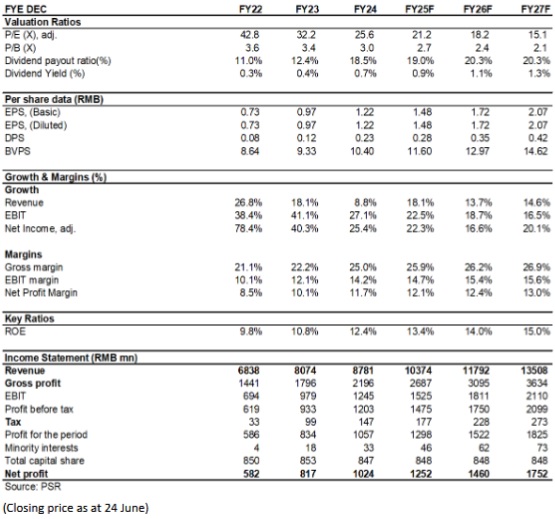

In 2024, the Company recorded revenue of RMB8,781 million (RMB, the same below), up 8.76% yoy; net profit attributable to the parent company amounted to RMB1,024 million, up 25.42% yoy; net profit attributable to the parent company excluding non-recurring items was RMB1,001 million, up 24.64% yoy. EPS was RMB1.22, with a dividend per share of RMB0.226, representing a dividend payout ratio of 18.5%.

In Q1 2025, the Company reported revenue of RMB2,065 million, down 0.47% yoy, mainly due to the contraction of the steel trading business. Excluding this impact, core business revenue grew 12.5% yoy; net profit attributable to the parent company reached RMB276 million, up 24.70% yoy; and net profit attributable to the parent company excluding non-recurring items was RMB269 million, up 28.27% yoy.

Among the various business segments, the new energy vehicle (NEV) gear business delivered standout performance. In 2024, this segment generated revenue of RMB3.37 billion, accounting for 38.38% of the Company's total revenue, up 51.21% yoy, showing a strong upward trend. In Q1 2025, this segment continued to grow at a pace exceeding that of downstream NEV sales, further increasing its share of total revenue and becoming a key driver of performance growth.

The traditional internal combustion engine (ICE) vehicle gear segment recorded revenue of RMB1,954 million in 2024, down 1.99% yoy. In Q1 2025, this segment remained stable, with a yoy decline of approximately 5%.

The intelligent actuator segment posted revenue growth of over 69% yoy in 2024 and maintained a similar growth rate in Q1 2025.

The commercial vehicle gear segment saw a revenue decline of 18.01% yoy in 2024, mainly due to a significant yoy decrease in H2 2023. However, Q1 2025 revenue data suggests a gradual recovery from the bottom, with revenue surpassing that of Q3 and Q4 2024, although still down on a yoy basis. The Company is intensifying efforts to expand its presence in the commercial vehicle market by actively targeting leading overseas clients and strategically investing in NEV e-drive gear products for commercial vehicles.

The construction machinery gear segment remained stable across all quarters of 2024 and Q1 2025, with revenue in Q1 2025 performing slightly better than that in Q3 and Q4 2024.

Improved Sales Structure Significantly Boosts Gross and Net Margins

The Company's gross margin increased from 22.24% in 2023 to 25.01% in 2024, up 2.8ppts yoy. In Q1 2025, gross margin further rose to 26.82%, up 4.17ppts yoy. This improvement was mainly due to a reduced share of low-margin steel trading and the scale effects of high value-added passenger vehicle gear business.

The Company maintained effective cost control and stable expense ratios: the period expense ratio stood at 10.59% in 2024, up 0.3ppt yoy, with selling/administration/R&D/financial expense ratios at 0.98%/3.99%/5.19%/0.43%, respectively, representing yoy changes of -0.03/-0.08/+0.44ppts/flat. In Q1 2025, the respective ratios were 1.0%/3.8%/5.4%/0.4%, up 0.06/0.1/0.6/-0.03ppts yoy, benefiting from ongoing cost reduction and efficiency enhancement measures, as well as scale effects. The Company will continue to implement such initiatives in the coming years, including smart manufacturing and big data systems. The rise in R&D expense ratio reflects sustained investment in innovation.

The Company's net profit margin reached 11.66% in 2024, up 1.55ppts yoy; and rose further to 13.37% in Q1 2025, up 2.7ppts yoy, indicating continued improvement in profitability.

Accelerated Overseas Expansion and Diversified Product Portfolio Advance in Tandem

In the high-profile NEV gear field, the Company had established an annual production capacity of 6,500 thousand sets for NEV transmission gear shafts by the end of 2024, with full capacity utilisation. The production base for NEV transmission components in Hungary is currently in the equipment commissioning phase, with capacity to be gradually released based on existing orders. As construction of the Hungary plant progresses, delivery lead times and logistics costs will be reduced, laying a solid foundation for further global market expansion.

Centred on gear technology, the Company continues to advance its diversified product layout. Looking ahead to the next two to three years, development across business segments includes: first, driven by growing sales of domestic B-class and above models, demand for high-precision, low-noise gear products is surging. As a leading player in China's NEV gear market, the Company is expected to further increase its market share by leveraging its technological advantages and optimising its sales structure. Additionally, the coaxial reducer gear (used in industrial robots) and intelligent actuator (used in robotic vacuum cleaners) segments offer vast market potential and are likely to become new growth drivers. Other segments, including commercial vehicles and construction machinery, are expected to remain generally stable over the next two years..

Investment Thesis

Shuanghuan Driveline is a pacesetter in the domestic automotive gear industry and robotic RV reducer industry. By leveraging its advantages in capacity, management, R&D and customer base, the Company has seized the opportunities for upgrading brought by gear outsourcing and high industry barriers as a result of the booming new energy vehicle industry. Looking forward, the Company is expected to continuously benefit from the boom of new energy passenger vehicles, expansion of the industrial chains of automatic gearboxes of commercial vehicles, and rapid development of robotic reducers and gears for daily use.

As for valuation, we expected diluted EPS of the Company to RMB 1.48/1.72/2.07 of 2025/2026/2027. And we accordingly gave the target price to RMB35 respectively 24/20/17x P/E for 2025/2026/2027. "Accumulate" rating. (Closing price as at 24 June)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()