-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Phoenix Healthcare Group (1515.HK) - Continued Shareholding of Central Enterprises may Create More External Expansion

Wednesday, July 6, 2016  23708

23708

Phoenix Healthcare Group(1515)

| Recommendation | Buy |

| Price on Recommendation Date | $11.400 |

| Target Price | $15.100 |

Weekly Special - 2333 Great Wall Motor

Unique Model Contributes to Leading Position

Phoenix Healthcare (PHG) has a wealth of mature hospital management experience and has developed a set of mature IOT public hospital trusteeship model. In other words, in addition to increasing investment in improving hardware, the company breaks away from covering hospital expenses with medicine revenue through reform of transparent doctors` income and centralized procurement via supply chain. Such model does not need additional government investment and hence is quite appealing to public hospitals.

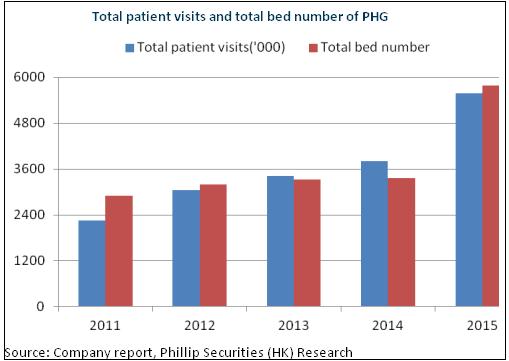

In this way, PHG has grown into the leading private hospital manager. Furthermore, business indexes of the trusted hospitals have improved year by year. For instance, the outpatient visits and inpatient visits of Jian Gong Hospital, Yan Hua Hospital and Mentougou Hospital significantly increased. Also, their bed turnover rate constantly rose and the operating efficiency was substantially enhanced. In the past five years, the compound annual growth of the company's revenue and net income reached 28.4% and 41%, respectively, far higher than the average growth rate of the healthcare industry.

Continued Shareholding of Central Enterprises may Create More External Expansion

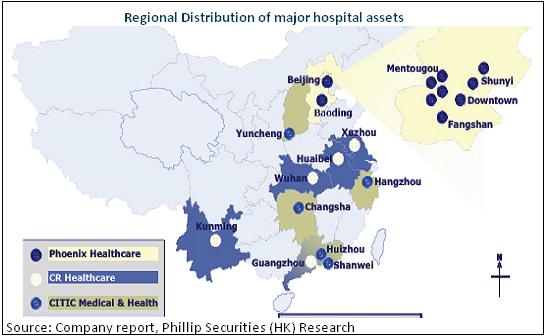

The company announced successively in April and May that CR Healthcare and CITIC Medical & Health became shareholders of PHG through assets injection. CR Healthcare will inject funds in 47 medical institutions (including 4 Grade III hospitals, 6 Grade II hospitals, 25 Grade I hospitals and 12 community service centers) and 3 old-age care institutions. Specifically, the actual available beds in medical institutions totaled nearly 6,000 and those in senior care institutions totaled 300. The combined income from medical business in 2015 of the underlying hospitals amounted to RMB2.41 billion. The assets are evaluated at HK$3.72 billion, which was exchanged for 463 million additional issued shares of PHG at HK$8.04. Finally, CR Healthcare will hold 35.7% of equity in PHG, thus becoming the controlling shareholder. Additionally, CITIC Medical & Health will inject funds in 2 Grade III hospitals and assets of 700-bed hospitals in exchange for 131 million additional issued shares of PHG at HK$9.50, equivalent to HK$1.24 billion. Finally, CR Healthcare will hold 9.15% of equity in PHG, thus becoming the second major controlling shareholder.

Therefore, PHG will develop into the largest hospital management group in Asia, covering 109 hospitals (12 of which are Grade III hospitals) and operating 12,480 beds. Its scale doubled as compared with its previous scale. Meanwhile, the company substantially blankets the whole country. Previously, PHG primarily concentrated in Beijing, Tianjin and Hebei, while CR Healthcare and CITIC Medical & Health in South China and Central China, including Guangdong, Yunnan, Hubei, Hunan, Anhui, Jiangsu, Zhejiang, etc. It is particularly important that CR Healthcare and CITIC Medical & Health are the first-grade subsidiaries of large central enterprises. Therefore, the company will have the endorsement of large central enterprises` brand and goodwill, encouraging greater willingness of local governments to cooperate with the company. Also, the expansion capacity of PHG outside Beijing is expected to significantly improve. In the meantime, the background of central enterprises may lower the company's debt financing costs, hence gaining financial advantage.

Valuation

Apart from rapid expansion, PHG also commits itself to exploring cooperative healthcare system, and constructs an integrated grading system of diagnosis and treatment. Besides, medical supply resources are allocated from large hospitals to small hospitals through multi-site practices and driving discipline development of doctor teams within the system. These efforts will constantly boost the company's competitive edge in the domain of hospital management.

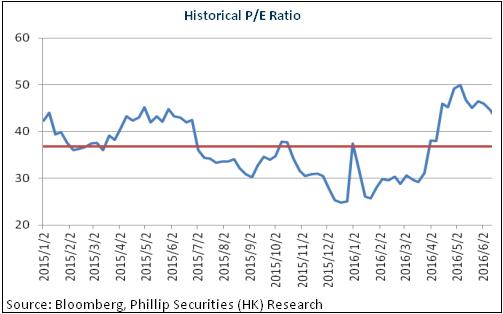

In respect of valuation, aside from shareholding of central enterprises, the company's management also acquired shares at the price of HK$9.96-10.97 / share, thereby offering adequate margin of safety. We give the company the target price of HK$15.1, equivalent to 35x 2016 EPS, with the "Buy" rating initially.

Risks

Trans-municipal and trans-provincial hospital management and integration risks;

Insufficient talent pool;

Restructuring of public hospitals falls short of expectations.

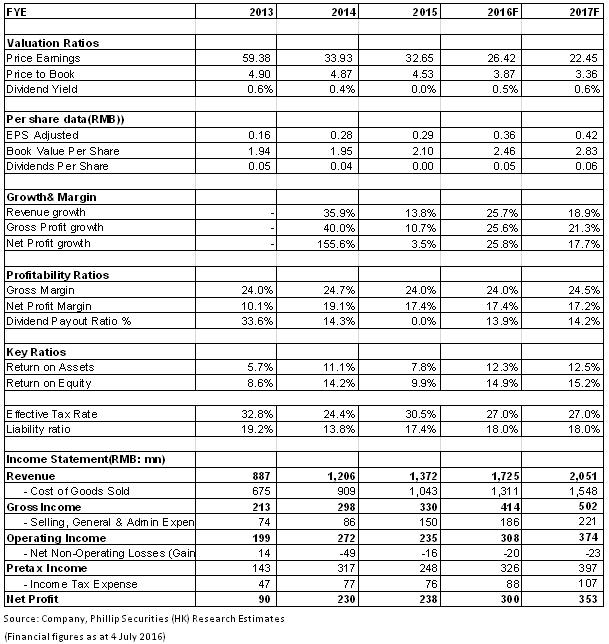

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()