-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Fuyao Glass (3606.HK) - FY2021 Q1 Review

Friday, July 2, 2021  21158

21158

Fuyao Glass(3606)

| Recommendation | Accumulate |

| Price on Recommendation Date | $55.950 |

| Target Price | $60.000 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

Results Hit a Record Q1 High in 2021Q1

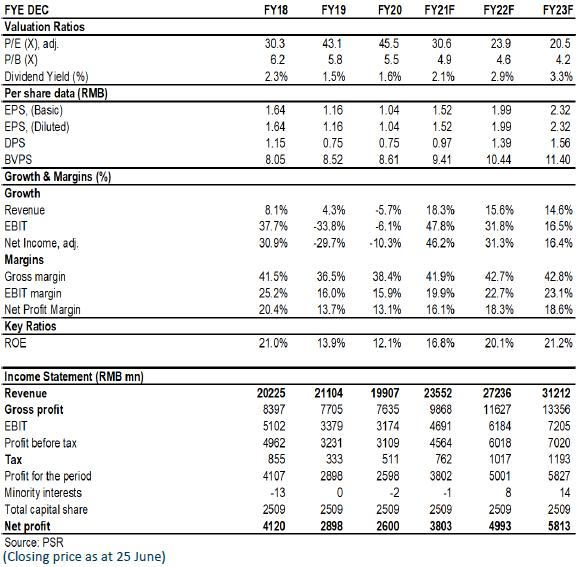

According to the results report for Q1 2021, Fuyao Glass reported revenue of RMB5,706 million in 2021Q1, up by 36.8% yoy, and down by 6.9% qoq; the net profit attributable to the parent company was RMB855 million, up by 85.9% yoy, and down by 2.6% qoq; the net profit attributable to the parent company excluding non-recurring items was RMB813 million, up by 113.8% yoy, and up by 2.4% qoq. The reason for the year-on-year increase was the low base in the same period due to the coronavirus pandemic in 2020. However, compared to the first quarter of 2019, Fuyao Glass's revenue, net profit attributable to the parent company, and net profit attributable to the parent company excluding non-recurring items still increased by 15.7%, 41% and 57%, respectively, hitting a record high in its first quarter. In addition, after deduction of the exchange gains and losses caused by the exchange rate turbulence in the first quarter, the total profit increased by 102.8% yoy, which is far higher than 67.8% before the deduction. Compared to 2020Q4, the results declined slightly in 2021Q1, mainly dragged by the shortage of chips in the automotive industry.

Rising Capacity Utilisation Rate Drove Year-on-year Increase in Gross Margin

The Company recorded a 40.6% gross margin in 2021Q1, up by 6.2 ppts yoy, and down by 2.2 ppts qoq. The significant yoy increase was mainly due to 1) the lower base caused by the low capacity utilisation rate due to the pandemic last year, and 2) the substantial year-on-year decrease in losses of the Germany-based subsidiary SAM. The qoq decline was mainly due to the shortage of chips in 2021Q1, which resulted in a lower capacity utilisation rate than in the fourth quarter of 2020.The period expense ratio was 22.3%, up by 1.6 ppts yoy. Specifically, the sales expense ratio, administration expense ratio, R&D expense ratio, and financial expense ratio was 7.3%, 8.9%, 4.1%, and 2.0%, respectively, down by 0.2 ppts, down by 2.1 ppts, up by 0.5 ppts, and up by 3.5 ppts, respectively yoy. The increase in financial expense ratio was mainly due to fluctuations in exchange gains and losses (RMB142 million), which resulted in an increase of RMB180 million in financial expenses over the same period last year.

The Smart Car Era Is Coming, and the Company Will Benefit from the Value Improvement of Single Vehicles in the Long Term

In order to promote technological upgrading and increase the added value of products, the Company has maintained a higher R&D input ratio in the industry. In the first quarter of 2021, the R&D expense ratio reached 4.13%, up by 0.5 ppts yoy. In 2020, the proportion of high value-added products, such as thermal insulation glass, head-up display glass, and dimmable glass, increased by approximately 2.64 ppts compared with the same period last year. Benefiting from the demonstration effect brought by Tesla, several automotive manufacturers began to launch new models with canopy glass in 2020. It is expected that canopy glass will be popularized rapidly from 2021. In the future, the Company's matching value of glass for single vehicles is expected to increase by 2 to 3 times, to stimulate the continued growth of follow-up results. On the other hand, in 2020, the Company signed strategic cooperation agreements with partners such as BOE and Beidou Zhilian to strengthen cooperation on smart dimming automotive glass, car window display, high-precision GNSS positioning and communication multi-mode smart antenna + automotive glass fusion solutions. The penetration rate of smart glass such as HUB glass is expected to further increase with the rapid development of automobile intelligence. The Company also raised funds to enter the field of photovoltaic glass, continuously expanded its product mix, and further established its long-term sustainable growth.

Investment Thesis

Overall, considering the steady leading position, continuous optimization of the product structure and a high dividend rate, we give the "Accumulate" rating, with a slightly revised target price to be HK$60, equivalent to 33/25.6/22x P/E for 2021/2022/2023E. (Closing price as at 25 June)

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()