-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

HC Group (2280.HK) - Sales revenue exceeding 10 billion, performing well in transition

Wednesday, February 13, 2019  10384

10384

HC Group(2280)

| Recommendation | Buy |

| Price on Recommendation Date | $4.640 |

| Target Price | $6.700 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

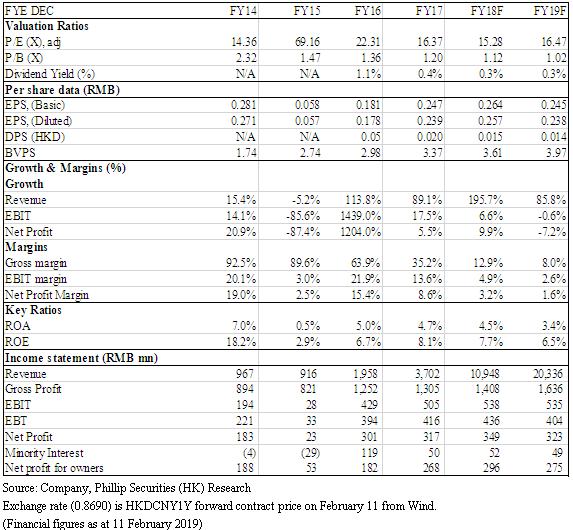

HC Group is an information and B2B e-commerce service company in China. Its main businesses include: transaction, data and information services. Assuming 2018E P/E ratio to be 22x (the average of the past five years is 24x, we think 22x is within the reasonable range), we derive the target price to be HK$6.70, and maintain a “Buy” rating with 44.4% potential upside. (Closing price at 11 Feb 2019)

Performance review

The Group announced that its sales revenue exceeded RMB 10 billion, a substantial increase of more than 170%. The Group said that the increase in sales revenue was mainly due to the initial achievements in the industrial Internet, which led to a significant increase in transaction service revenue, while data services are also rapidly developing. This figure is close to our earlier forecast (2018F sales revenue: 10.9 billion), and believe that the group's income will eventually reach our expectations.

However, this significant increase in sales revenue was mainly attributable to the transaction service segment with lower gross profit margins, so we believe that net profit growth will not be as high as sales revenue growth. We expect net profit in 2018 to be RMB 349 million, up about 10% YoY. However, we believe that the Group is in the stage of development. The primary goal is to increase the number of users and usage of the platform. Therefore, we believe that even if the net profit does not increase significantly, the significant increase in sales revenue has proved that the development strategy of the Group goes well.

Business update

New business segments

The Group has reclassified the business segment, namely New Technology Retail , the Smart Industry and Platform and Enterprise Service.

1. New Technology Retail

Relying on ZOL.com and JDHui.com, the Group takes 3C products and home appliances as an entry point. Through the SaaS solution of Rongshang, it penetrates into the operation of small and medium-sized retailers, helping retailers solve difficulties in customer acquisition, low customer repurchase rate, supply chain optimization and lack of interaction with customers and so on.

Smart Industry

The Group has vertical platforms in various industries, such as Union Cotton, China Formwork and Ibuychem. The platform will penetrate the industry to address difficulties and meet demand, and will replicate this model to other industries in the future.

Platform and Enterprise Service

The Group relies on HC360, Trading Wisdom and its own financial services to establish industrial data links and business scenarios to provide value-added services to SMEs and transform them.

Strategic cooperation with Qidian, the subsidiary of Tencent

The Group announced that it has reached a strategic cooperation with Qidian, the subsidiary of Tencent to build an industrial Internet ecosystem. The reason for this cooperation is that Tencent and HC both agree that the industrial Internet is the next stage in the internet industry, so they hope to complement each other through cooperation. They will cooperate in product cooperation and joint marketing in AI, machine learning, Internet of Things, SaaS, IM, etc., and jointly develop adaptation industry scenarios in various fields such as manufacturing, trade wholesale, and new retail.

Combing the advantages of both sides, the B2B pan-industry version of the product jointly developed by HC and Qidian will be launched this year, in order to solve the pain of information asymmetry between buyers and sellers. The new product is developed based on “慧聰友客”, a product of the Group. With the most advanced information technology, it can locate business opportunities more quickly, provide the seller with a visual communication opportunity, accurately and quickly match the needs of buyers and sellers; realize real-time monitoring of the network in the background. The status of the visitor actively initiates a session invitation to the high-intention visitor; implements mobile visitor monitoring, actively invites the visitor to negotiate; the APP message promptly reminds, and communicates with the visitor and other functions at any time and any place. In addition, Qidian provides a solution for regulating the official image of the company's external communication and communication management of business personnel for the B2B pan-industry products. It solves the real-name certification and authenticity of upstream and downstream business personnel and provides powerful. The communication and connection capabilities, customer data comprehensive protection against loss, help companies to improve the efficiency of inquiry quotation from release, discovery to analysis and processing.

Financing 450 million RMB from Construction Bank

The Group announced the issuance of RMB 350 million guaranteed and secured notes and RMB 100 million guaranteed and secured convertible bonds. The interest rate is 2.85% plus HIBOR. And, the conversion price of the convertible bonds is HK$6, and the convertible bonds will be convertible into 16,666,667 conversion shares. 50%-55% of the funds are used for transaction service support and supply chain financing; 20% for information service related technology development, including user-generated content and applications; 20% for data service related software as a service, Internet of Things and Blockchain applications; and 5%-10% for general use.

We expect that the impact of this financing on interest cost for 2018 will not be too obvious, as the notes and convertible bonds are only issued to investors on the beginning December in 2018, so it will only be accounted for one month of interest cost in 2018.

Valuation

The sales revenue of the Group was in line with our expectations, and we lift our forecast on interest cost. Assuming 2018E P/E ratio to be 22x (the average of the past five years is 24x, we think 22x is within the reasonable range), we derive the target price to be HK$6.70, and maintain a “Buy” rating, 2% higher than our previous target price, due mainly to the appreciation in RMB, with 44.4% potential upside. (HKD/CNY=0.869)

Risk

1. The presence of B2B platforms with similar functions

2. Demand for the commodity reduces due to the economic downturn

3. Suppliers refuse to cooperate with the Group

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()