-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Perfect World (002624.SZ) - Remarkable performance in mobile gaming business

Friday, August 16, 2019  24608

24608

Perfect World

| Recommendation | Buy |

| Price on Recommendation Date | $26.270 |

| Target Price | $34.370 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Perfect World engaged in Film and TV series creation as well as Gaming development in China, together with strong game development and film production capabilities. Assuming a target P/E of 23x in 2019, we derived a TP of $34.37, 0.3% higher than previous TP. We maintain a “Buy” rating, with a potential upside of 30.8%. (Closing price at 14 Aug 2019)

Interim result update

The revenue (excluding the cinema business) grew by 12.44% YoY, reaching RMB 3,656 mn. The net profit attributable to the owners was RMB 1,020 mn, up by 30.5%, while the net net profit attributable to the owners excluding the non-recurring gains and loss was RMB 973 mn, rose by 37.67%. The operating cash flow was RMB 167 mn. The gross profit margin was up from 59.6% in 18H1 to 68.6% in 19H1.

Business update

Gaming

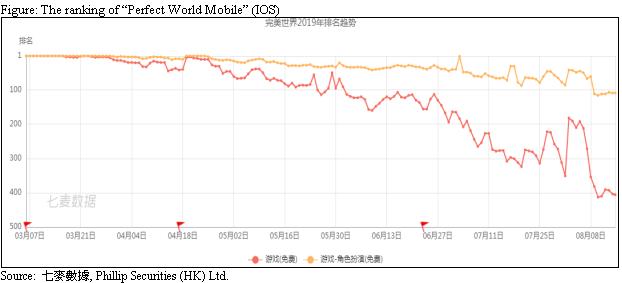

The gaming revenue reached RMB 2,878 mn, up by 8.06% YoY. In terms of PC gaming, the performance of “Perfect World”, “Zhu Xian”, “DOTA2” and “CS:GO” all remained persistent. The Group are developing a new game, called “Xin Zhu Xian Shi Jie” based on the IP of “Zhu Xian”. In terms of Mobile gaming, the revenue boosted significantly by 39.4%, thanks to the strong performance of “Perfect World Mobile” launched in this March. It ranked the first in the IOS billboard for about 20 days. The “Legend of Condor Hero Mobile” has also launched on July along with a top ranking in IOS. The Group are still developing games, such as “Wo De Qi Yuan”, “Meng Huan Xin Zhu Xian”, “Xin Shen Mo Da Lu” and etc, which will fuel the growth in mobile gaming in the next few years.

Films & dramas

The revenue from films & dramas dropped by 22.4% to RMB 779 mn, due mainly to the sales of cinema business. In terms of dramas, the Group has launched “I Will Never Let You Go”, “Qing Chun Dou”, “In Youth” and etc. “I Will Never Let You Go” went into the top 3 in weekly drama of Zhejiang Television, while “In Youth” also ranked the top based on the CSM55 ratings. In terms of films, the Group planned to maintain its strategic cooperation with Universal Pictures on film production.

Valuation

As the revenue growth in 19H1 of PC and console gaming was lower than expected, we lower the revenue in 2019F by 8.4% to 6.4%. However, we saw a significant improvement in GPM and a good cost control in both selling and administrative expenses. As a result, we only lower the net profit growth by 1.3% to 14.3%. Assuming a target P/E of 23x in 2019, we derived a TP of $34.37, 0.3% higher than previous TP due to the previous share buyback. We maintain a “Buy” rating, with a potential upside of 30.8%.

Risk

1. Lower-than-expected growth in Mobile gaming

2. Giant entering the film & drama production

3. Loss in production team

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()