-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

李浩然先生(Eric Li)

高級分析師

高級分析師

現任現為輝立証券持牌高級分析師,曾任職股票基金、家族辦公室及證券公司等,擁有多年的證券研究部門從業及投資經驗,並先後於香港最暢銷的財經媒體撰寫投資專欄。畢業於香港理工大學電子計算系。

Eric is currently a licensed research analyst at Phillip Securities. Prior to joining Phillip Securities, he has years of equity research and investment experiences in asset management company, family office and securities company. Meanwhile, he has written investment columns in Hong Kong`s best-selling financial media for years. He holds Bachelor of Arts in Computing from The Hong Kong Polytechnic University.

| Phone: | 22776516 | Email: | erichyli@phillip.com.hk | |

Xtep International (1368.HK) - 1H2022 Positive profit alert in line with consensus

Monday, August 8, 2022  1825

1825

Xtep International(1368)

| Recommendation | Neutral |

| Price on Recommendation Date | $12.800 |

| Target Price | $13.010 |

Weekly Special - 3306 JNBY Design Limited

1H2022 Positive profit alert in line with consensus

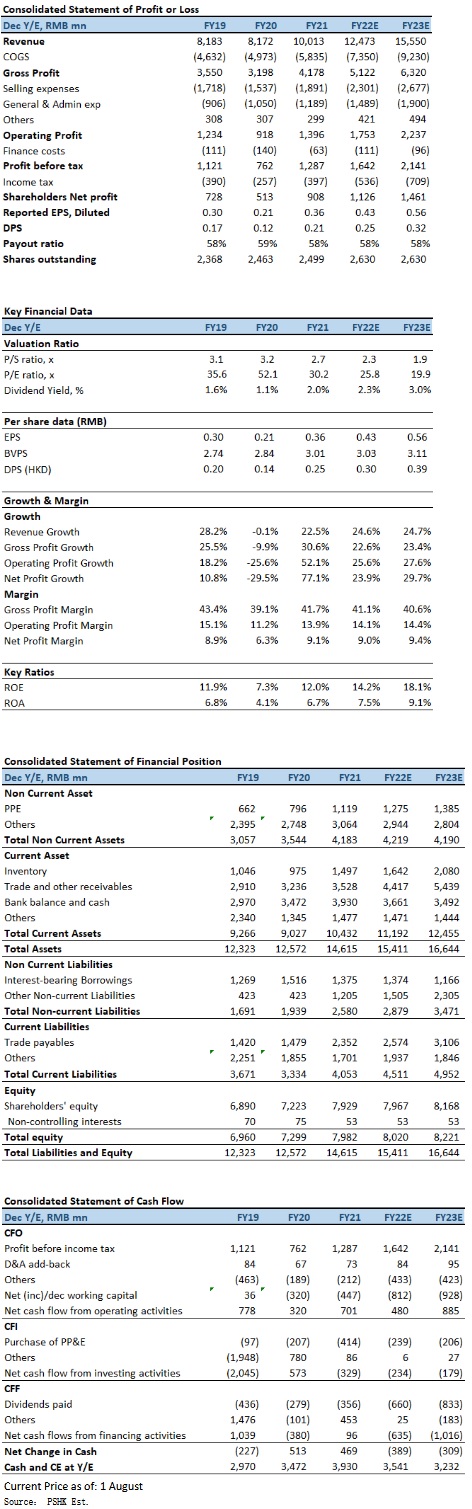

Xtep announced the operation data of 2Q2022. Xtep core brand products retail sell-through (including offline and online channels) grew by mid-teens (30 % – 35 % growth in 1Q2022), retail discount level at 25% – 30% (25% discount at 1Q2022). For the six months ended 30 June 2022, core brand products retail sell-through (including offline and online channels) grew by 20 % – 25 %, and inventory turnover was around 4.5 months (about 4 months in 1H2021, 1Q2022), estimated to be related to the impact of the COVID.

Xtep also expected to record a significant increase of not less than 35% in its unaudited consolidated profit attributable to shareholders for 1H2022 as compared to that for the corresponding period in 2021, which is also in line with market consensus. Such increase was primarily due to a not less than 35% growth in consolidated revenue mainly attributable to: (1) remarkable sales fair orders resulting from encouraging retail performance of the core Xtep brand and Xtep Kids` business driven by their breakthrough in product innovation, retail channel upgrade and increased brand awareness; and (2) an impressive YoY revenue growth of over 100% for Saucony under the professional sports segment owing to its strong retail sales particularly in its e-commerce business.

Adverse impact of COVID on the economy is fading in June, 618 sales growth 64%

The adverse impact of the latest round of COVID outbreaks on the economy is fading, and the resumption of work and production in key cities, core brand products sales are expected to gradually improve. In fact, according to the 618 Shopping Festival sales data in 2022, Xtep recorded a 64% YoY online sales growth to RMB650mn, while the online sales of the core Xtep brand surged 61% to RMB590mn and those of Xtep Kids swelled 103% to RMB75mn. Saucony's even rocketed 135%, the most among all international sports shoe brands during the Festival.

Company valuation

In 2Q2022, Xtep's core brand products retail sales growth slowed down due to the impact of the resurgence in pandemic. However, Xtep continues to cooperate with international brand distributors and launched a new store in Tangshan Rongda Shopping Mall with Pou Sheng in July. With the expansion of quality channels, which may help the sales growth of core brand and offset the impact of the COVID in the first half of the year. We adjust our FY2022E EPS forecast to RMB0.43 (down slightly compare with March 2022 report), with TP at HKD13.01, represents of 26.2x P/E (equivalent to the average P/E ratio of the past 2 years plus 1 standard deviation). We downgrade our investment rating to “Neutral”.

Risk factors

1) Resurgence in COVID in mainland; 2) Weak domestic growth and consumer spending in sportsware; 3) Intensified competition in the industry; and 4) Slower-than-expected in new brands development.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()