-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

A-Share Research Report

The articles are produced in Chinese only.

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Daimay (603730 CH) - Expanding Roof Business to Open More Growth Potential

Monday, December 1, 2025  2404

2404

Daimay(603730)

| Recommendation | Accumulate (Initiation) |

| Price on Recommendation Date | $8.210 |

| Target Price | $9.170 |

Investment Summary

FY2025 Q3 Remain Stable

The Company released its Q3 2025 report: In the first three quarters of 2025, the company achieved revenue/net profit/net profit excluding non-recurring items of RMB 4.794 billion/RMB 445 million/RMB 600 million, representing yoy growth of -0.19%/-28.62%/-3.09%, with a gross margin of 28.04%, a yoy decrease of -0.22 percentage points. In Q3 2025 alone, the Company achieved revenue/net profit/net profit excluding non-recurring items of RMB 1.62 billion/RMB 203 million/RMB 198 million, which represents yoy increases of +6.65%/+0.24%/+0.75%.

Fire Impact in the First Half Gradually Eliminated

Despite a challenging overseas market in Q3, the performance of Daimay remain stable: From the demand of major auto markets in Q3 2025: North American vehicle sales were 5.104 million units, down slightly by 2.16% qoq; European passenger car registrations were 3.1136 million units, down by 9.33% qoq. However, the company's Q3 revenue/net profit excluding non-recurring items showed qoq increases of +2.38%/+0.83%, reflecting its stable operations. Additionally, a fire in the second quarter at the Company's Mexican plant led to non-operating expenses of USD 33.751 million, equivalent to RMB 242 million. These damaged assets are all covered under insurance claims. Daimay has submitted a claim letter to AXA Insurance and expects the final insurance compensation to cover the actual losses.

Expanding Roof Business to Open More Growth Potential

In 2023, Daimay issued convertible bonds to expand the production of roof and roof assembly products. The project has secured customer appointments, including 300,000 sets of automotive roof system integration products and 600,000 sets of automotive roof products at the Mexican Daimei facility, and 700,000 sets of automotive roof products at the Zhoushan Yindai facility. The company's main products, such as sun visors, headrests, and central roof controllers, have an equivalent per vehicle value of RMB 588. The roof products and roof integration system products from the convertible bond project have a per vehicle value of RMB 700 and RMB 4,000, respectively. This value increase will open up growth potential for Daimay's future performance. According to the prospectus of the convertible bonds, it is estimated that once the project reaches full capacity, Daimay's revenue will increase by RMB 844 million in the first year, accounting for 16.4% of Daimay's 2022 revenue, and by RMB 2.11 billion in the third year.

On the net profit side, after the project reaches full capacity, net profit will increase by RMB 111 million in the first year, and RMB 289 million in the third year. Currently, the company's "Annual Production of 700,000 Roof Products" project has been completed, while the "Mexican Automotive Interior Parts Industrial Base Construction Project" is expected to be delayed from January 2025 to December 2026. Upon completion, it is expected to add 300,000 sets of automotive roof system integration products and 600,000 sets of automotive roof products annually. The capacity expansion will provide assurance for securing new orders from North American customers in the future.

Company profile

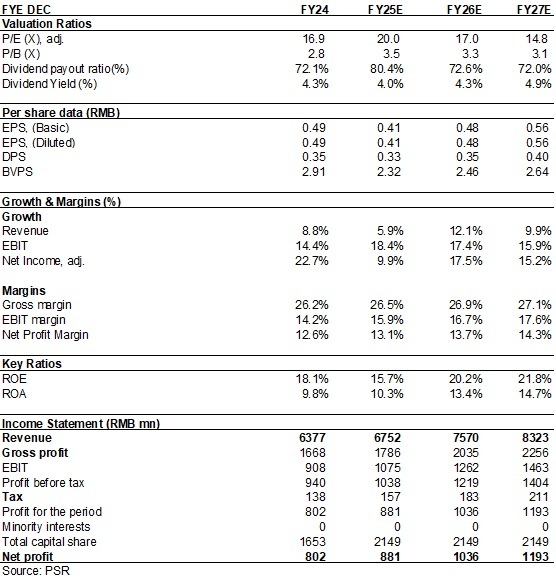

Daimay was established in 2001 and is a well-known manufacturer in the global automotive interior parts sector. Its main products include automotive interior components for roof systems and seat systems, such as sun visors, headrests, roof linings, central roof controllers, armrests, and other automotive interior products. Among these, the Company's core product, the automotive sun visor, ranks first globally in its segment, with a market share exceeding 40% in 2022. In 2024,Daimay reported a revenue of RMB 6.377 billion, a yoy increase of +8.8%, with 85.35% of the revenue coming from overseas markets. The net profit was RMB 802 million, a yoy increase of +22.66%.

Investment Thesis & Valuation

The Company's business in the automotive sector remains stable, and the projects funded by the convertible bonds are about to contribute to revenues, providing momentum for performance growth. We are optimistic about the Company's development prospects.

As analyzed above, we expected diluted EPS of the Company to RMB 0.41/0.48/0.56 of 2025/2026/2027. And we accordingly gave the target price to 9.17, respectively 19x P/E for 2026. "Accumulate" rating. (Closing price as at 25 November)

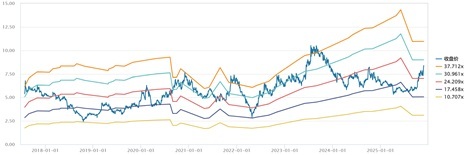

Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research

Financials

(Closing price as at 25 November 2025)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()