-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Yangtze Optical Fibre and Cable (6869.HK) - Comprehensive Technology and Complete Industry Chain Layout Help Consolidate the Leading Position

Monday, February 15, 2016  16945

16945

Yangtze Optical Fibre and Cable(6869)

| Recommendation | Buy |

| Price on Recommendation Date | $7.330 |

| Target Price | $10.000 |

Weekly Special - 3306 JNBY Design Limited

Internet Construction Leads to Short Supply of Optical Fibre

Currently, the Chinese government actively invests RMB1.14 trillion in constructing high-speed Internet and will accelerate fibre-to-the-home (FTTH) in the coming three years. Therefore, the accelerated construction of 4G network and fixed-line broadband in mainland China and the rise of IDC, cloud computing and big data business will contribute to the increased demand for transmission network expansion. Also, the United States leads the global network transmission speed to upgrade from the current 10Gbps to 40-100Gbps. Overall, these will help maintain a heavy demand for optical fibre and cable, from which the company will benefit.

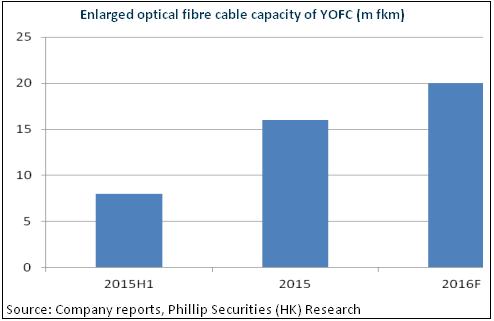

Presently, the optical fibre market has faced the predicament of short supply for the first time since FY2000. The optical fibres for tender and bid of China Mobile in 2015 to 2016 totalled 94.52 million km, a YoY increase of around 60%. Meanwhile, the tender price of all manufacturers basically grew by 5-10%. In this tender, the share of YOFC ranked the third, like 12.5% of tendered G.652D optical fibre. We believe that the company will still embrace the favorable situation of increase in both sales volume and price and that its performance will see further rapid growth.

In the meantime, in order to adapt to the national policy of "One Belt and One Road", the company plans to build a cable plant in Myanmar and Indonesia in 2015. At present, the company plans to open up opportunities of growth in Africa / South America and intends to build one million km/year of cable facilities in South Africa. The FTTH penetration rate in Africa, South America and other places is only 2.5%, resulting in vast space for development. Since optical fibre is fragile and inappropriate for transport, localized production is a more favorable choice. We believe that the strategy of YOFC will lead to its sustained growth in overseas contribution.

Comprehensive Technology and Complete Industry Chain Help Consolidate the Leading Position

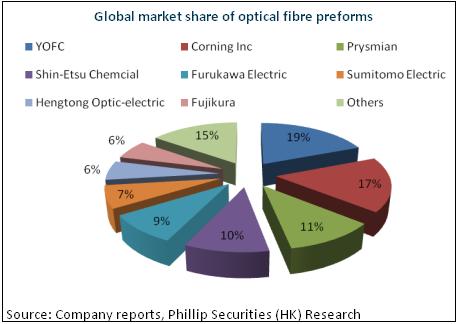

In the profit structure of optical fibre industry chain, preform accounts for about 70%, being most profitable. At present, YOFC not only owns the largest capacity in this field, but is the only enterprise mastering PCVD, VAD and OVD technologies in the world. So by integrating the advantages of these three technologies, its manufacturing of cladding and mandrel has been globally cutting-edge. Furthermore, the company will expand the capacity of Hubei Qianjiang with Phase I capacity reaching 500 tonnes. As a result, the company will continue to consolidate its leading position in the domain of the preform and increase its self-sufficiency rate to enhance profitability.

Meanwhile, the company also starts the whole industry chain layout. Downstream, the fibre coating project was officially approved, and also, the company broke into the field of integrated cabling. Currently, the domestic high-end market of data centre cabling is monopolized by imported brands with over 40% of gross margin. But in the era of big data, this demand will be immense. Upstream, the company carries the layout of key raw materials such as silicon tetrachloride and germanium tetrachloride. Overall, the company will be the one with the longest industry chain in the industry of optical fibre and cable in the globe and will keep consolidating its leading position.

Industry Leader but Undervalued

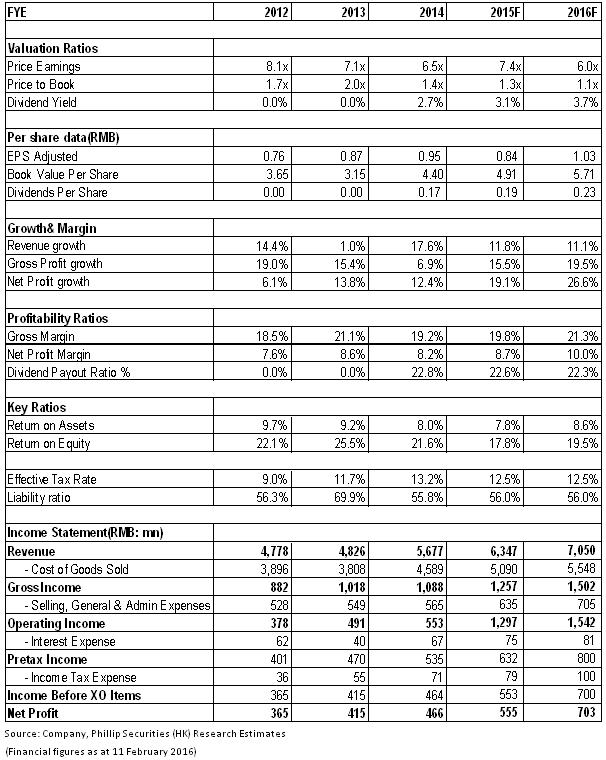

In spite of the overall excess capacity in the cable industry, the short supply of optical fibre preform and accelerated construction of "Broadband China" and "FTTH" in mainland China will significantly improve the supply and demand situation. As an industry leader, the company is equipped with technical and profitable advantages, so its sales growth is worth expecting. We take 10 times as the PE ratio valuation of EPS in 2015 and the target price can reach 10 HKD, with the "Buy" rating. (Closing price as at 11 Feb 2016)

Risk

The capital expenditure of operators` fixed-line broadband falls short of expectation.

Intense competition results in the decline in profitability.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()