-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

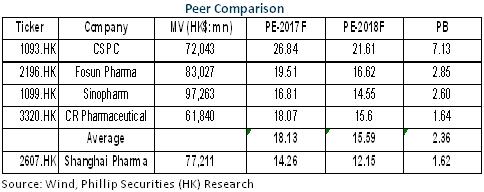

Shanghai Pharma (2607.HK) - Continuous National Layout of Distribution Business

Tuesday, July 18, 2017  15511

15511

Shanghai Pharma(2607)

| Recommendation | Accumulate |

| Price on Recommendation Date | $22.150 |

| Target Price | $26.400 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

As an industry giant in pharmaceutical circulation, with the help of the "two invoices" system promoted nationwide and the reform of replacing the business tax with a value-added tax, Shanghai Pharma's distribution business will achieve a higher growth rate than the industry average through internal and external drives, and its medium-term profit growth rate is expected to reach 15-20%. At the same time, the key variety strategy and the early layout of generic drug consistency evaluation will facilitate the stable increase of the pharmaceutical industry. In addition, the SOE reform is expected to form a catalyst. We give the company the valuation of 17x EPS in 2017, and the target price at HKD26.4, with “Accumulate" rating. (Closing price as at 13 July 2017)

Continuous Improvement in Profitability

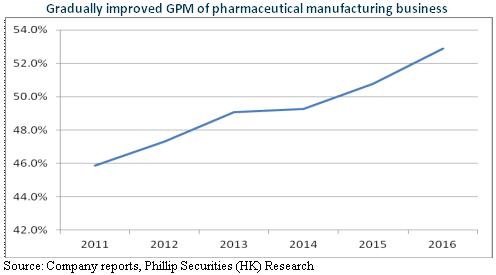

In 1Q17, Shanghai Pharma recorded a revenue of RMB33.13 billion, an annual increase of 13.2%; net profits attributable to the parent company were RMB1 billion, an annual growth of 12.4%; net profits excluding non-recurring items were RMB940 million, an annual increase of 20.8%, which was mainly benefited from higher profit margin of pharmaceutical manufacturing and distribution business.

Specifically, the company's distribution revenue grows only 12.9% for the reason that Shanghai, Shandong and other places had a high base in 1Q16 because of increased contribution of innovation business. However, the distribution business` gross profit margin increased by 0.16% to 6.15%, and the operating profit margin increased by 0.02% to 2.64%. Meanwhile, the pharmaceutical manufacturing sector income increased by 20% to RMB3.79 billion, and the internal growth rate was approximately 10% excluding the VITACO consolidated factors. The sharp growth in results was mainly benefited from the increasing price of low price drugs and scarce drugs. The operating profit margin rose by 1.33% to 14.14%. Key products income increased by 15.1% year-on-year, and the gross profit margin increased by 1.8% to 69.8%, which met the expectation.

Continuous National Layout of Distribution Business

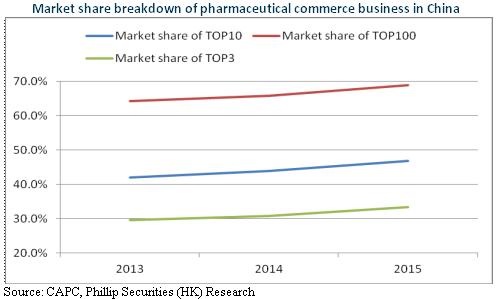

According to the NHFPC's planning program, the "two invoices" system will be carried out all over the country in 2018. At present, only six provinces including Anhui and Sichuan have implemented the "two-invoices" system, and it is expected that the concentration of distribution industry will be rapidly upgraded. The three major drug-distribution enterprises take up approximately 35% market share currently, and anticipate a rise to more than 50% within three years. As the third largest pharmaceutical distributor in China, Shanghai Pharma is expected to benefit from this trend and will become stronger.

The existing distribution network of Shanghai Pharma covers 21 provinces and is expected to expand to 28 provinces (except Qinghai, Tibet and Xinjiang). So far, the company has been implementing the M&A strategy, in which the south-west and north-east regions are the first round of key mergers and acquisitions. In 2H16, the company expanded business to Yunnan and Heilongjiang. In 1Q17, it also continued to acquire Xuzhou Pharma, Xuzhou Huaihai Pharma, both of whose income scales are approximately RMB3 billion, increase its equity ratio in Guangzhou Zhongshan Medical Pharmaceutical to 82.6%, and keep optimizing the layout in Jiangsu and Guangdong. We expect that the company's distribution business will hopefully achieve the growth in revenue and gross margin and promote the performance increase by 15-20% for the commercial sector with the help of "two invoices" system and the reform of replacing the business tax with a VAT.

Pharmaceutical Manufacturing Business May Steadily Rise

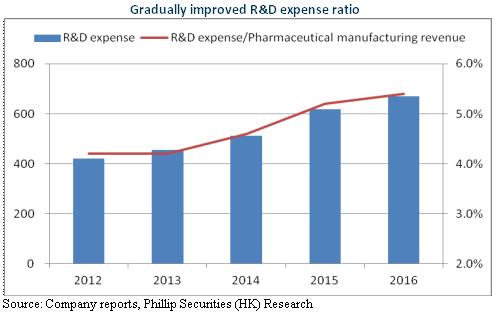

The company's pharmaceutical manufacturing business has been developing stably, and the average growth rate was approximately 7% over the past five years. But the growth is expected to increase this year. First of all, the company will adhere to the key variety strategy, whose production and marketing focus on higher profitability, greater market demands and greater potentials with more entry barriers. Now its products with sales over 100 million in 60 key varieties are up to 26.

Second, the consistency evaluation of company is expected to pull ahead. Shanghai Pharma has prepared for the policy as early as 2013. So far, related work of sixty or seventy varieties has been started. At the end of 2016, the company signed the strategic cooperation agreement with 10 Tertiary A hospitals such as Shanghai Huashan Hospital and Ruijin Hospital, and determined the cooperation intention of 32 varieties of BE (bioequivalence), so that it fully ensured the clinical base. We expect that the company's generic drug consistency evaluation will hopefully complete the overall testing at the end of 2018, and some products are expected to take the lead in completing the assessment, thereby winning greater market shares.

Risks

The national expansion of distribution business is below expectations;

The SOE reform is below expectations;

R&D expenses increases sharply.

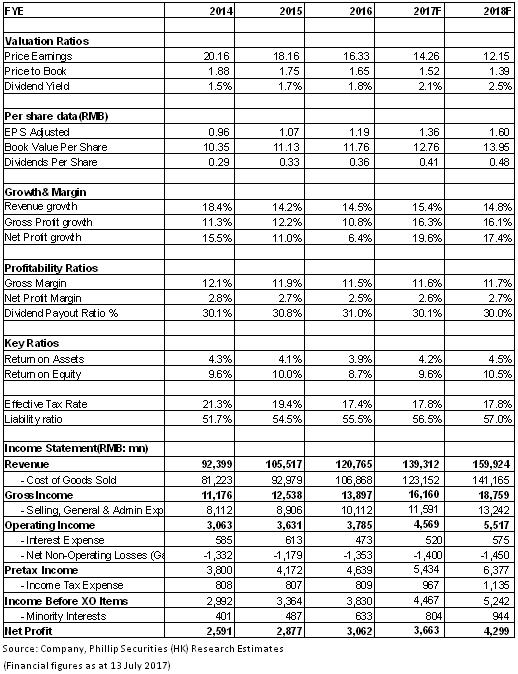

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()