-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Inovance Technology (300124.CH) - New Energy and Railway Transportation Business Helping to Drive the Second Take-off of the Company

Wednesday, July 19, 2017  14880

14880

Inovance Technology(300124)

| Recommendation | Buy |

| Price on Recommendation Date | $23.710 |

| Target Price | $32.400 |

Weekly Special - 3306 JNBY Design Limited

Company profile: Excellent Leader in the Field of Industrial Control Automation

Shenzhn Inovance Technology Co,ltd., was established in 2003 and listed on the GEM of Shenzhen Stock Exchange in 2010. Inovance Technology is a medium- and high-end equipment manufacturer focusing on the industrial automation control products. The total number of employees is 4,522. The products are widely used and the business scope covers:

1) intelligent equipment & industrial robot core components such as various variable-frequency drive, servo system, control system, industrial vision system and sensor,

2) new energy vehicle power assembly core components such as various motor controller and auxiliary power system,

3) rail transit traction and control system such as traction converter, auxiliary converter, high-voltage compartment, traction motor and TCMS,

4) industrial Internet solutions in the Auto Aftermarket such as intelligent hardware and information management platform.

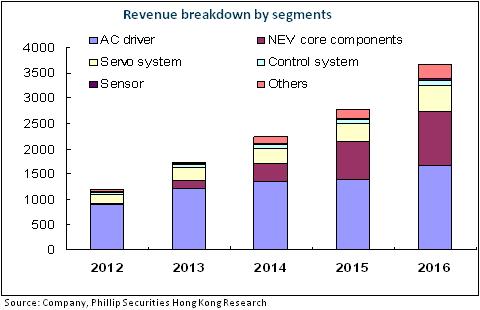

The proportions of the company's several categories of products to revenue are as follows: the inverter for 45%, the servers for 16%, the new energy products for 23%, the rail traffic for 6.3%, others for 8%.

Rapid Growth for 10 Years and the Market Share Keeping Increasing

Originally a producer of variable-frequency drive, the Company superimposed grasp of market opportunities and asset acquisitions onto the upgraded core technical strength based on the continuous R&D investment and continued to expand the business scope and the market share. The Company successively developed the general variable-frequency drive, elevator integration machine, servo drive, new energy vehicle electronic control system, rail transit traction system and the industrial robot. In the industrial automation products, the Company is the largest supplier of low- and medium-voltage inverter and servo system. The market share of the low-voltage inverter, the start-up product of the Company, rose from the 13th place (1.8%) in 2008 to the third place in 2016 (6%), only second to ABB and Siemens, and it was the leader in self-owned brands. In the elevator industry, the Company has become the leading elevator integration controller supplier; in the field of the new energy vehicles, the Company has become the leading enterprise of China's new energy vehicle motor controller and is the exclusive supplier of electronic control system of Yutong Bus.

The management of the Company attaches great importance to R&D. The high investment continues and more excellent talents are attracted in the meantime. From 2013 to 2016, the investment in R&D of the Company accounted for 9%, 10%, 9% and 11%, respectively of the revenue, and the proportion of the R&D personnel was 23%, 24%, 24% and 28%, respectively. As of the end of 2016, it owned 630 patents with certificates, including 182 patents for invention, 367 utility models and 81 design patents. Since the listing, the Company has launched three equity incentive programs, respectively granting stock options to 227, 174 and 652 people, among which the third one is of the largest range. It nearly covered all the core leaders of the middle and high level, which helped to stimulate the enthusiasm and motivation of the staff. In addition, the sales model of the Company is flexible. The distribution model is for the general products, and the direct sales model is for the important customers. The Company attaches importance to the coordination and cooperation in the sales with the local distributors.

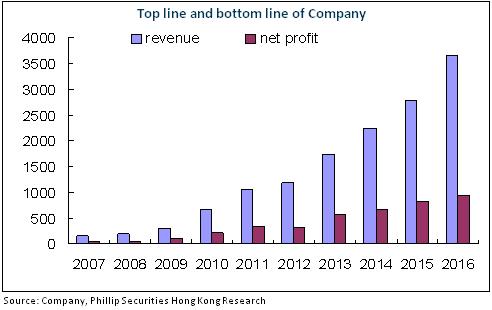

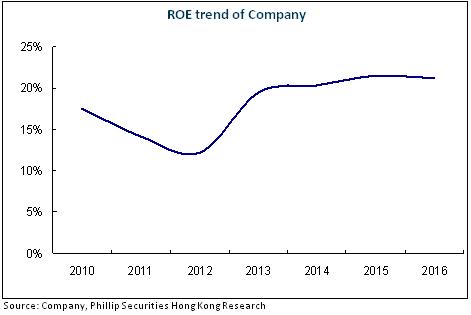

The Company maintained a compound growth rate of revenue up to 41.7% and a compound growth rate of net profit up to 39.1% from 2007 to 2016. The strength of the Company's core R&D ensured that the gross profit margin remained around at a high rate of 50% and that the net interest rate remained at around 30%; what's more, ROE increased from 9.6% in 2007 to 19.8% in 2016.Debt asset ratio of the company is 37.5% with good cash condition.

The original business has recovered and the new business turns on the high-speed channel

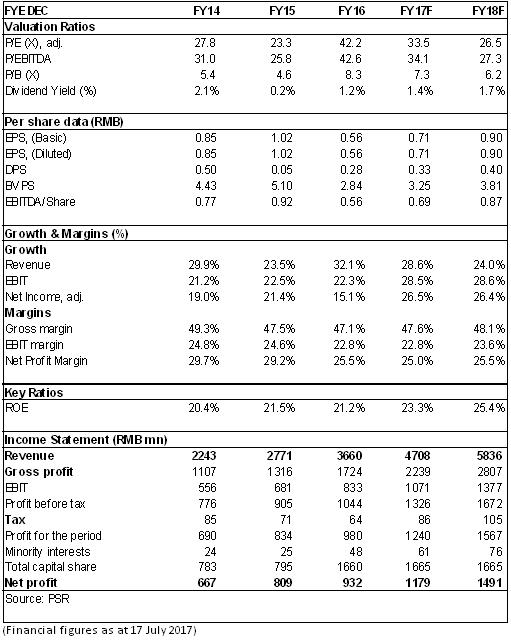

The company realized revenue of RMB3.66 billion Yuan in 2016, increasing by 32.11% over the same period of last year. The net profit attributable to the shareholders of the listed company was RMB0.923 billion, up by 15.14% year on year. The net profit growth was faster but still slower than the income growth. It lay in that the proportion of new acquisition rail transportation business of lower gross margin increased while the research and development, management and labor costs increased rapidly. The company realized an income of RMB0.782 billion in 2017, a year-on-year increase of 37.7%; net profit attribution stood at RMB0.172billion, a year-on-year increase of 23.54%. Gross profit margin fell by 1.55 percentage points to 46.6%, mainly due to China's new energy vehicle market influenced by policy interference in the first quarter.

As fluctuations in the manufacturing and real estate, the profit growth ratio of the company's original business in 2012 and 2014 slowed down, but we agreed that China's manufacturing industry began to enter into the structural pick-up cycle after years of de-stocking and adjusting structure, providing a support for structural recovery of the equipment manufacturing industry. On the other hand, the upgrading of manufacturing transformation and the increase of labor cost will lead to the growth of automation and intelligent equipment demand, thus driving the shipments of company's general automation business. In the main tone of the country striving to develop new energy vehicles and rail transit, the core technology advantages previously accumulated will bring a high-speed development space for new energy motor control products and rail transit traction products. And we believe that from the second half of 2017, factors of perturbing gross profit margin to decline brought by new business will gradually vanish. The company's performance will return to high growth

Valuation

As analyzed above, we expected diluted EPS of the Company to RMB 0.71 and 0.9 of 2017/2018. And we accordingly gave the target price to 32.4, respectively 36x P/E for 2018. "Buy" rating. (Closing price as at 17 July 2017)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()