-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Yunnan Baiyao (000538.SZ) - Recent volatility brings accumulating opportunity

Tuesday, July 3, 2018  12593

12593

Yunnan Baiyao

| Recommendation | Accumulate |

| Price on Recommendation Date | $104.030 |

| Target Price | $112.000 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

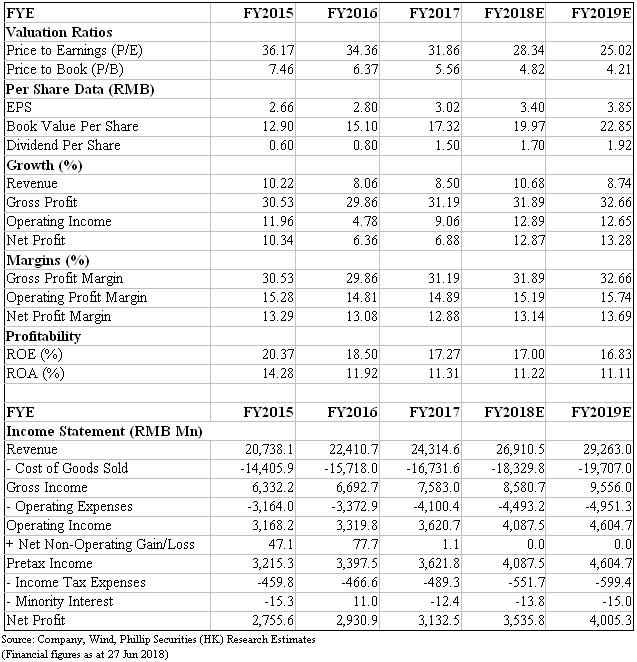

We highlight that recent market volatility brings accumulating opportunity. We restate that company fundamentals remain strong given improving salesman efficiency and solid 18Q1 results (revenue up by 7.26% YoY, NP up by 11.18% YoY and CFO up by 137.75%). We also suggest to pay attention to company's further exploration in hospital field. We maintain 18E EPS target of RMB3.4, and given 33x target PE, we give target price RMB112. (Closing price at 27 Jun 2018)

Business Overview

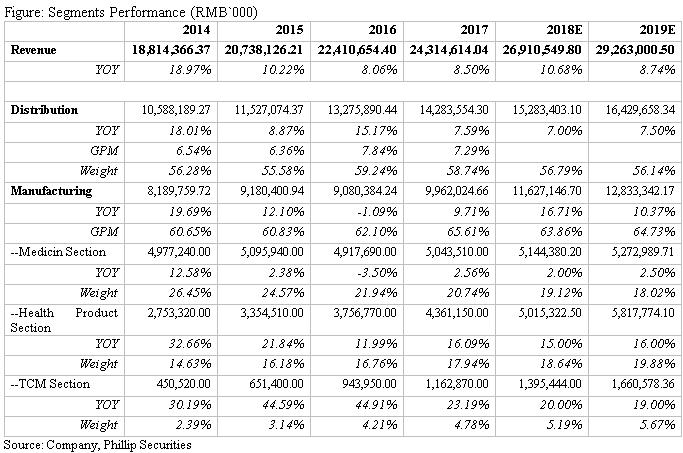

Larger gets larger. The report on drug circulation industry in 2017 issued by the Ministry of Commerce of China showed that the growth rate of pharmaceutical wholesale enterprises was slowing down, given Top 100 pharmaceutical wholesale enterprises report sales up by 8.4% YoY (dropped by 5.6 ppts compared to 2016 growth). The company reported wholesale business revenue of RMB14.5bn, ranking sixteenth among the Top 100, is a regional circulation enterprises. In future, the regional leaders are likely to accelerate expansion through more cross region M&A to increase industry concentration.

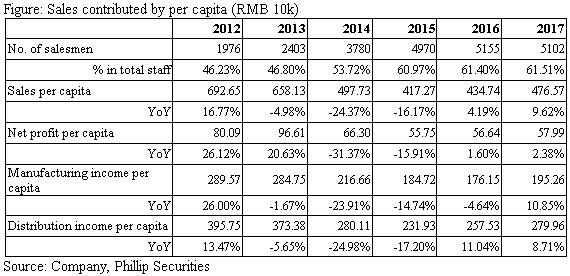

Salesman efficiency may continue to improve after the composite ownership reform. Salesman efficiency decreased during 2010 to 2016. In 2017, Yunnan Baiyao Holdings Limited (YBH) introduced New Huadu and Jiangsu Yuyue as strategic investors to diversify holding structure. We already see improving salesman efficiency in 2017, given revenue per capita was up by 9.62% YoY (2016 +4.19%) and net profit per capita up by 2.38% YoY (2016 +1.6%). We expect the company continue to improve operation efficiency.

Potential progresses of hospital business. Investor meeting summary on its website shows that the company may benefit from provincial government's favorable policies, as the government aims to build Yunnan as a healthcare center featured healthy lifestyle. The company, as a regional pharmaceutical leader, may try to cooperate with tertiary institutions and explore orthopaedics field leveraging on Baiyao's brand advantage.

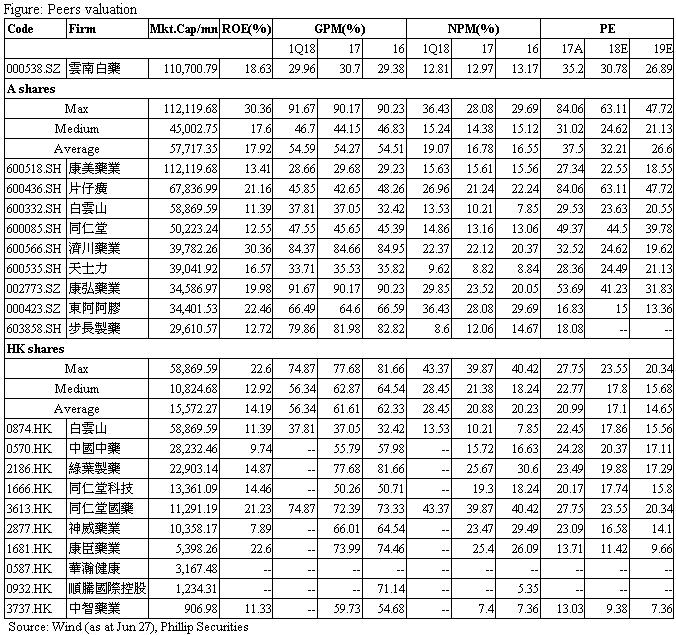

Investment Thesis, Valuation & Risk

Our model indicates a target price of RMB112.0. We estimate 2018E EPS to be RMB3.4 per share and with target PE 33x, we give 2018E Target price of RMB112.0. Risks include: Rising selling fees; Effects from Two-invoice system; Fierce competition in health product industry; Composite ownership reform fail expectation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()