-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

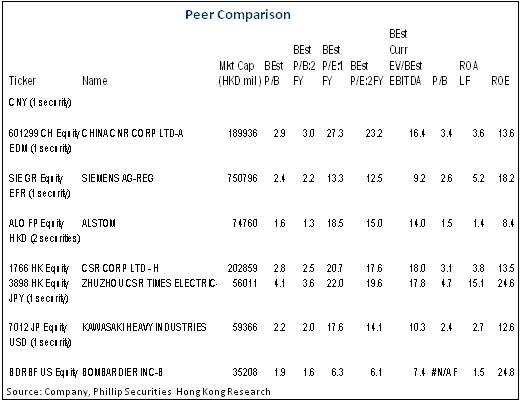

CSR (1766.HK) - Favorable factors has most reflected in the short term

Friday, January 23, 2015  17992

17992

CSR(1766)

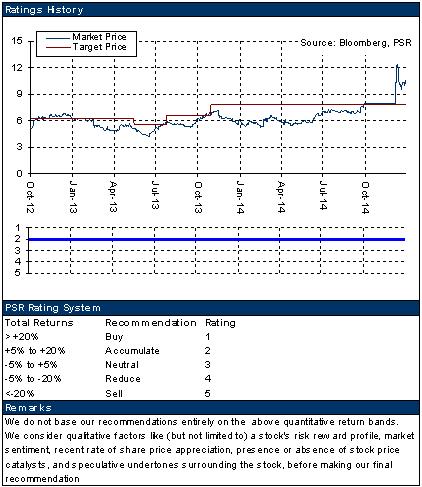

| Recommendation | Cautious Accumulate |

| Price on Recommendation Date | $10.360 |

| Target Price | $11.460 |

Weekly Special - 3306 JNBY Design Limited

The Merger plan of CSR and CNR was officially launched

China CSR made an official announcement of the Merger at the end of December, 2014, which will be conducted in the way of China CNR being absorbed and incorporated into China CSR. According to the announcement, China CNR's A/H shares will be canceled, and each China CNR share will be exchanged for 1.1 China CSR shares to be issued by CSR. Upon completion of the Merger, the Post-Merger New Company will be renamed CRRC Corporation Ltd or CRRC for short.

After the Merger, it is expected to avoid the price-cutting competition in overseas market

The previous split of CSR and CNR was an attempt of market reform of SOEs, with a purpose mainly to effectively prevent monopoly from impeding technical progress. Then in the following 14 years, the performance of both parties also proved the effect that mutual competition could promote development. But it also brought about the bad results of price battle and resource waste in the exploration of overseas market. The Merger of CSR and CNR is the outcome of the state will, which is expected to avoid the state's interest being impaired by their internal rivalry in the expansion of overseas market, and will benefit the long-term development of Chinese high-end equipment manufacture enterprises in the global market.

The Synergy Effects are expected to bring about reduction in cost after the Merger

No matter the railway and urban metro market at home or abroad, the aggrandizement of the Post-Merger business scale will also enhance the Company's negotiating ability, which will then bring about reduction in cost, and the Merger will be beneficial for the Synergy Effects to exert in staff allocation, material purchase, sales system and R&D area, so as to realize a more effective utilization of resources. In addition, the new company can share the research and development resources, make an overall planning on research and development system and product layout, to promote the company's overall competitiveness.

The bellwether of "One Road One Belt" strategy

According to the International Union of Railways (UIC), the total length of the high-speed railway in service, under construction and in planning in the world is 54.6 thousand kilometers. And the construction cost of China's high-speed railway is 1/3 to 1/2 of that of developed countries, and China can also provide package solutions of engineering design, construction, and equipment manufacturing and operation management. It can thus be seen that as the model of high-end equipment, China's high-speed railway manufacturing industry has the reason and ability to share growth bonus of the global high-speed railway market, and CRRC Corporation Limited after mergence accords with the direction of China's "Silk Road Economic Belt Region" strategy.

Investment Thesis

Nevertheless, this pre-arranged plan needs to be examined and approved by the A/H stockholders` meeting of CSR and CNR, the SASAC and the CSRC. There still exist some complicated procedures. After the consolidation by merger of any party, hundreds of billions of assets alteration and personnel disposition and arrangement can be finished after some very heavy and complicated procedures, which is just the reason for the subsequent stock price volatility.

CSR's share price rose significantly early (rose by 40% in the past three months), we think the favorable factors in the short term has most reflected, the further rise in the share price may be restricted so far, thus we downgrade rating to "Cautious Accumulate".

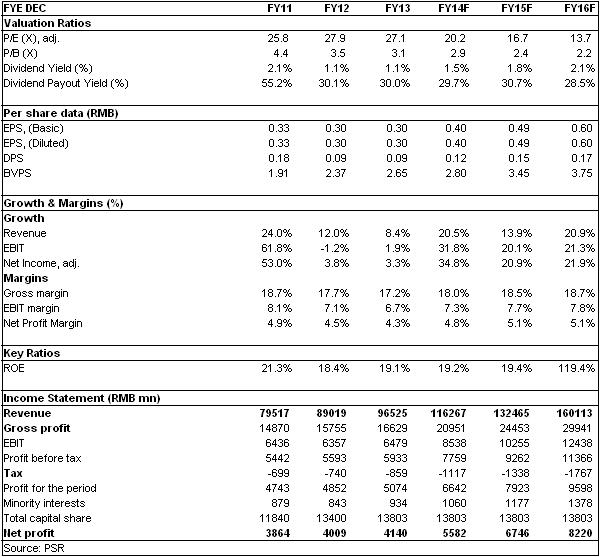

As analyzed above, we revised EPS expectation of the Company to RMB 0.404, 0.489, 0.596 of 2014/2015/2016. And we accordingly revised the target price to 11.46, respectively 22.4/18.5/15.1x P/E and 3.2/2.6/2.4x P/B for 2014/2015/2016.

The Merger plan of CSR and CNR was officially launched

China CSR made an official announcement of the Merger at the end of December, 2014, which will be conducted in the way of China CNR being absorbed and incorporated into China CSR. According to the announcement, China CNR's A/H shares will be canceled, and each China CNR share will be exchanged for 1.1 China CSR shares to be issued by CSR, which means the exchange prices of China CNR's shares are RMB6.19 and HK$8.05 per share respectively. For the dissenting shareholders, cash option is provided, with the transfer prices being respectively China CNR's A shares RMB5.92 per share, H shares HK$7.21 per share, China CSR's A shares RMB5.63 per share, H shares HK$7.32 per share. Upon completion of the Merger, the Post-Merger New Company will be renamed CRRC Corporation Ltd,. or CRRC for short.

After the Merger, it is expected to avoid the price-cutting competition in overseas market

The previous split of CSR and CNR was an attempt of market reform of SOEs, with a purpose mainly to effectively prevent monopoly from impeding technical progress. Then in the following 14 years, the performance of both parties also proved the effect that mutual competition could promote development. But it also brought about the bad results of price battle and resource waste in the exploration of overseas market. The Merger of CSR and CNR is the outcome of the state will, which is expected to avoid the state's interest being impaired by their internal rivalry in the expansion of overseas market, and will benefit the long-term development of Chinese high-end equipment manufacture enterprises in the global market.

The Synergy Effects are expected to bring about reduction in cost after the Merger

No matter the railway and urban metro market at home or abroad, the aggrandizement of the Post-Merger business scale will also enhance the Company's negotiating ability, which will then bring about reduction in cost, and the Merger will be beneficial for the Synergy Effects to exert in staff allocation, material purchase, sales system and R&D area, so as to realize a more effective utilization of resources. In addition, the new company can share the research and development resources, make an overall planning on research and development system and product layout, to promote the company's overall competitiveness

The bellwether of "One Road One Belt" strategy

According to the International Union of Railways (UIC), the total length of the high-speed railway in service, under construction and in planning in the world is 54.6 thousand kilometers. And the construction cost of China's high-speed railway is 1/3 to 1/2 of that of developed countries, and China can also provide package solutions of engineering design, construction, and equipment manufacturing and operation management. It can thus be seen that as the model of high-end equipment, China's high-speed railway manufacturing industry has the reason and ability to share growth bonus of the global high-speed railway market, and CRRC Corporation Limited after mergence accords with the direction of China's "Silk Road Economic Belt Region" strategy.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()