-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Coolpad Group (2369.HK) - Building Mobile Internet Ecosphere with Promising Future

Monday, July 6, 2015  7764

7764

Coolpad Group(2369)

| Recommendation | Buy |

| Price on Recommendation Date | $2.590 |

| Target Price | $3.590 |

Weekly Special - 3306 JNBY Design Limited

LeTV will contribute RMB 2.18 billion to hold 18% of Coolpad shares, becoming the second largest shareholder. At the end of 2014, Coolpad announced to form a joint venture with Qihoo 360. The Company's top priority is to convert itself into an Internet operator. Generally speaking, LeTV will win the mobile phone industry chain and enrich its terminal products from the cooperation, while Qihoo can obtain the access to the Internet traffic. Coolpad's varied product mixes, 40 million sets of shipment, and 6000 patents provide a basis for the mobile Internet platform. With Qihoo's security APPs, 360 OS and LeTV's video contents, the Company is no longer simply a hardware vendor. The three parties are expected to build up a mobile Internet ecosphere consisting of “terminal + APP + platform + contents”.

For the e-business channel where Coolpad is in collaboration with Qihoo, the Company will have two brands on the market, Qiku and Dazen, which will be commercially available in a few months. Importantly, the two branded mobile phones will be pre-installed with 360 OS, enabling users to clean any pre-installed software so that users can freely select the software they prefer. What's more, 360 OS will improve the system speed by three times, with standby time extending by 40% and saving traffic by 50%. Since 360 OS can overcome or mitigate Android's shortcomings, we anticipate that it will be accepted on the market. Overall, the Company will reach a total shipment of at least 4500 sets in 2015.

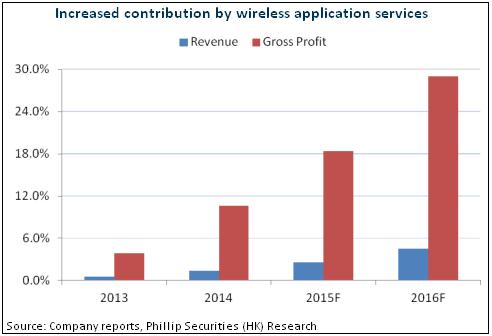

Coolpad's wireless application services will improve further by taking advantage of Qihoo's software APP and LeTV's contents and platform, and are likely to achieve a double growth in the mid-term. Considering the high profitability of the wireless application services, we anticipate that the services will become the Company's main profit source, contributing about 30% to its total profit.

Building Mobile Internet Ecosphere with Promising Future

Although its mobile phone business enjoys advantages in patent ownership, supply chain and after-sales services, Coolpad may have a hard time in the context of reduced subsidy by the operators and intense price war in the mobile phone industry. To get out of the difficult situation, the Company has carried out the cooperation with Qihoo and LeTV in order to build up the mobile Internet ecosphere, aiming to turn into an Internet operator. Meantime, its profit will come mainly from wireless application services, and it will be no longer a hardware vendor in the future.

Given this, Coolpad may face the re-valuation. Its conventional mobile phone manufacturing may face the growth bottleneck, or have the difficulty gaining profit, but the business is expected to achieve stable growth on the platform of the ecosphere. We value it as 10 times of the 2016EPS. For the emerging wireless application services, which experience a fast growth and a high profitability, we grant it 20 times of the 2016EPS. Altogether, we set a target price of HK$3.59, and give it a “Buy” rating. (Closing price as at 2 July 2015)

Coolpad Joins Hands with LeTV to Create a New Mobile Internet Ecosphere

On June 28, Coolpad announced that the controlling shareholder informed the Board of Directors that they sold 18% of the Coolpad shares to Leview Mobile HK Limited (one of the LeTV's subsidiaries). Once the transaction is completed, LeTV contributed RMB 2.18 billion to hold 18% of Coolpad shares, becoming the second largest shareholder, while Guo Deying continues to hold the remaining 20.3% of Coolpad shares, not the controlling shareholder any more. At the end of 2014, Coolpad announced to form a joint venture with Qihoo 360, with the two holding 50.5% and 49.5% of the JV shares respectively but in joint control.

In our opinion, the cooperation programs with Qihoo and LeTV were two moves Coolpad made to get out of the difficulties as the operators reduced subsidies and the price war was intensifying. Now, the Company's top priority is to convert itself into an Internet operator. Generally speaking, LeTV will win the mobile phone industry chain and enrich its terminal products from the cooperation, while Qihoo can obtain the access to the Internet traffic. Coolpad's varied product mixes, 40 million sets of shipment, and 6000 patents provide a basis for the mobile Internet platform. With Qihoo's security APPs, 360 OS and LeTV's video contents, the Company is no longer simply a hardware vendor. The three parties are expected to build up a mobile Internet ecosphere consisting of “terminal + APP + platform + contents”.

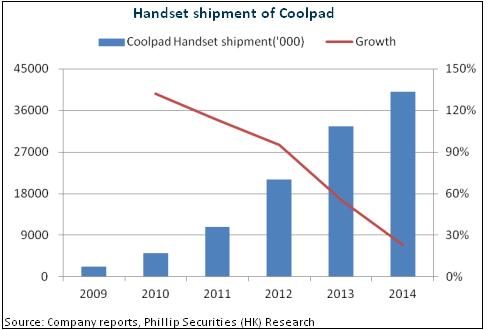

Terminal Shipments are Likely to Bottom Up

In the wake of the financial crisis, and to go with the trend of smart phones, Coolpad's mobile phone shipments and the performance have increased rapidly and peaked in 2014. But as the operators reduced their subsidy, the Company's terminal business faces the declining.

To overcome the situation, the Company has adjusted its strategies in branding and channel development. Now it has three brands, which are Coolpad, IVVI and Dazen, targeting low-end, mid-end and high-end customers and relying on operators, retailers and e-business companies respectively. Specifically, the proportion of the shipments to the operators will fall from 80%+ to 50%, and then remain stable. The brand IVVI takes the form of joint shareholding, i.e., 60% for the Company and 40% for officers and tier-one agency. The share incentives may drive the expansion of its market shares soon.

For the e-business channel where Coolpad is in collaboration with Qihoo, the Company will have two brands on the market, Qiku and Dazen, which will be commercially available in a few months. Importantly, the two branded mobile phones will be pre-installed with 360 OS, enabling users to clean any pre-installed software so that users can freely select the software they prefer. What's more, 360 OS will improve the system speed by three times, with standby time extending by 40% and saving traffic by 50%. Since 360 OS can overcome or mitigate Android's shortcomings, we anticipate that it will be accepted on the market. Overall, the Company will reach a total shipment of at least 4500 sets in 2015, and the latest Q2 data shows that the qoq improvement has already been made.

Wireless Application Services may Become the Primary Profit Driver

According to its 2014 financial report, the Company's revenue from the wireless application services grew fastest by 2.3 times to HK$349 million, consisting of software pre-installation, APP revenue sharing and ads, which contribute 40%+, 40%+ and 10%+ respectively. It is worth mentioning that the services have a gross margin of up to 90%, contributing 24% of the gross margin in H2 of 2014. Therefore, although the revenue contribution only accounted for 1.4% of the total in 2014, it was one of the primary sources of the profits.

We believe that Coolpad's wireless application services will improve further by taking advantage of Qihoo's software APP and LeTV's contents and platform, and are likely to achieve a double growth in the mid-term. Considering the high profitability of the wireless application services, we anticipate that the services will become the Company's main profit source, contributing about 30% to its total profit.

Catalyst

Monthly shipment increases better than expected;

Transformation strategy progresses smoothly, with the better-than-expected profit of wireless application services.

Risks

Mobile phone price war is intensifying.

The strategic cooperation remains at a standstill.

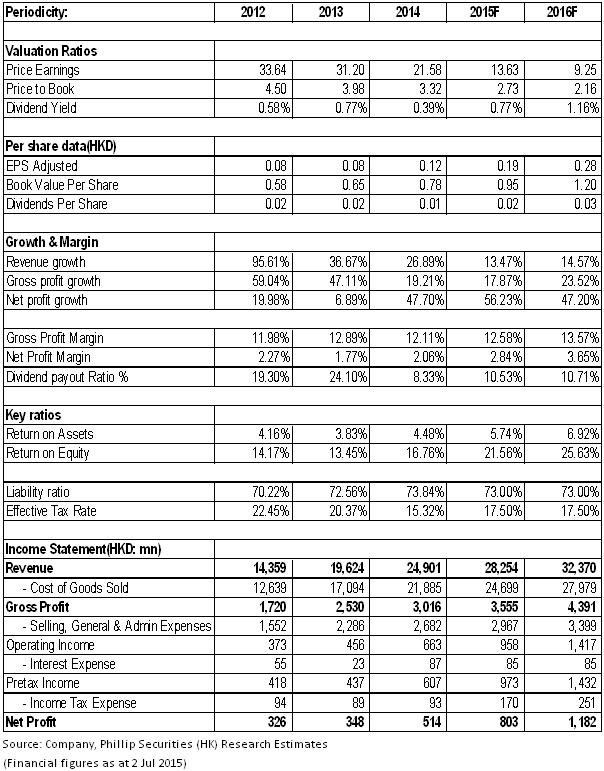

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()