-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

DONGJIANG ENV (895.HK) - Steady Connotative Growth and Well-established Leading Position

Wednesday, January 18, 2017  19409

19409

DONGJIANG ENV(895)

| Recommendation | Accumulate |

| Price on Recommendation Date | $12.680 |

| Target Price | $14.600 |

Weekly Special - 3306 JNBY Design Limited

Steady Connotative Growth and Well-established Leading Position

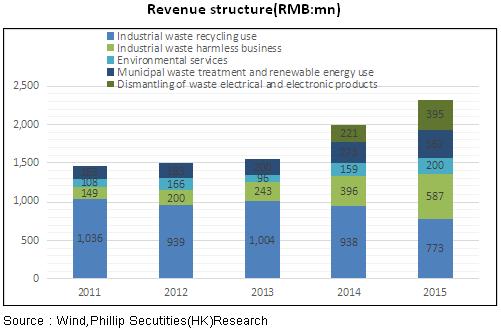

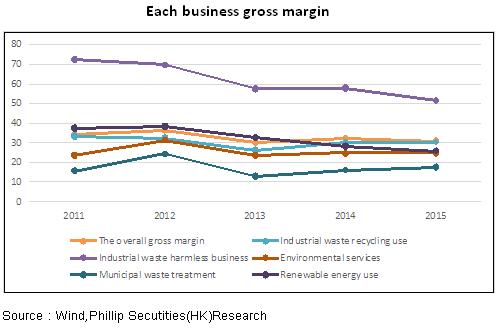

After years of connotative growth + denotative expansion, Dongjiang Environmental has developed from a hazardous waste leader in Guangdong Province to a hazardous waste leader across the country. At present, it has set up the whole industry chain business including industrial hazardous waste treatment, environmental services, municipal waste treatment and renewable energy use, and dismantling of waste electrical and electronic products. In the first three quarters of 2016, driven by steady growth in all businesses, the company's operating revenues reached RMB1.866 billion, representing a year-on-year increase of 6.6%. Its net profit attributable to shareholders of parent company amounted to RMB380 million, surging by 43.9% over the same period last year. The greater increase in the net profit attributable to shareholders of parent company than that in revenues is primarily attributed to the investment income derived from selling two subsidiaries -- Qingyuan Dongjiang and Hubei Dongjiang-- and from the adjustment in value-added tax. With regard to profitability, the gross profit margin rose by 1.15 percentage points to 34.86% over last year, which mainly resulted from the increase in the proportion of harmless business with a higher gross profit margin. In respect of expenses, the expense ratio during the period stood at 19.19%, up by 2.9 percentage points over the same period last year. Besides, the company's expense increase in denotative expansion was not too fast, showcasing its remarkable ability to control expenses.

Rapid Promotion of Projects and Continuous Focus on Harmless Business

The company has basically achieved the transformation from utilization of industrial hazardous waste resources to harmless business. The hazardous waste treatment capacity reached 1.36 million tonnes/year in 2015, wherein harmless production capacity accounted for 48% of the total capacity, and is expected to reach 1.9 million tonnes/year in 2016 and the harmless production capacity will continue to increase. Presently, the imbalance between supply and demand of the industrial hazardous waste treatment industry is serious, and the existing disposal capacity is exceedingly insufficient. In order to satisfy the rapidly growing harmless treatment market, the company vigorously promoted the development and new expansion of projects. Currently, a total of 6 industrial solid waste projects are being running or under construction, including Jiangxi Solid Waste Project, Huizhou Dongjiang Expansion Project, Yancheng Coastal Solid Waste Project and Nantong Solid Waste Project. 4 out of the six projects are estimated to be put into operation in the second half of 2016. Additionally, the environmental assessment of projects totaling 246,000 tonnes in Shandong Weifang and Hebei Hengshui made gratifying progress, and such projects are expected to completed and put into operation in 2017. Besides, the company also won the first industrial waste disposal PPP project during the period, which was also the first domestic hazardous waste disposal PPP project. The project scale reached 94,700 tonnes/year, hence helping the company to accumulate more experience in undertaking more similar projects in the future.

Investment Rating

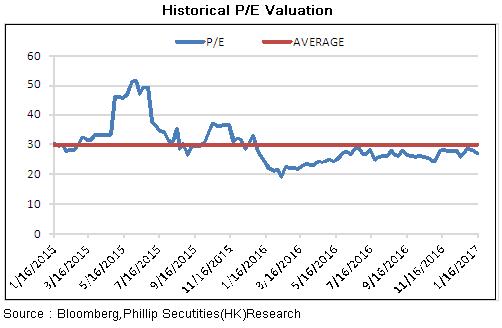

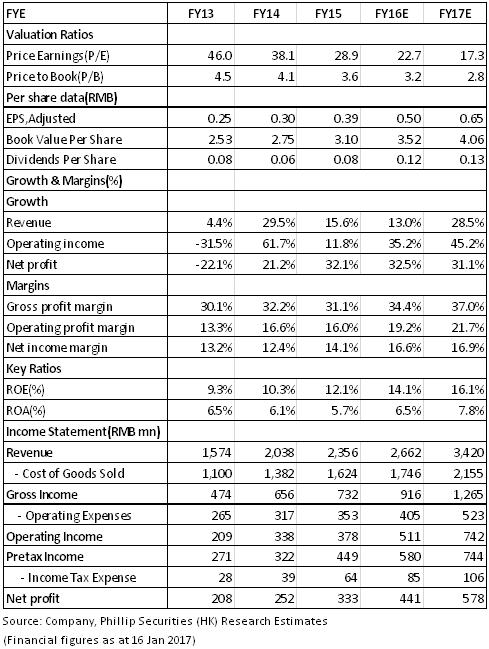

In order to avoid the obligation of general offer, the company has terminated the non-public issue of A shares at present. The termination of the private placement will neither affect the controlling shareholder status of Guangdong Rising Assets Management Co., Ltd., nor will it adversely affect the company's operation and business development. Furthermore, the company has sufficient capitals to guarantee its normal operation. We expect the company's revenues will reach RMB2662 million and RMB3420 million, respectively, in 2016 and 2017. Also, net profits will stand at RMB441 million and RMB578 million, respectively. EPS will reach RMB0.50and RMB0.65, respectively, and a target price of RMB 14.6. The "Accumulate" rating is given. (Closing price as at 16 Jan 2017)

Risk Warnings

Production of projects fails to meet expectations;

Prices of non-ferrous metals prices continue to slip;

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()