-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Haohai Biological Technology (6826.HK) - Epitaxial Acquisition Leads New Impetus to the Development of Ophthalmic Business

Tuesday, July 11, 2017  16326

16326

Haohai Biological Technology(6826)

| Recommendation | Buy |

| Price on Recommendation Date | $41.600 |

| Target Price | $51.200 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

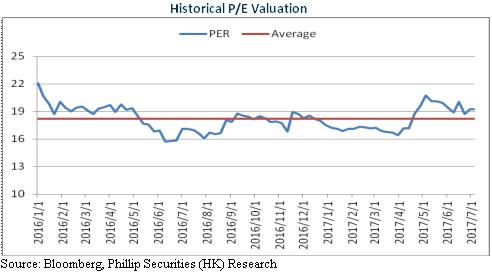

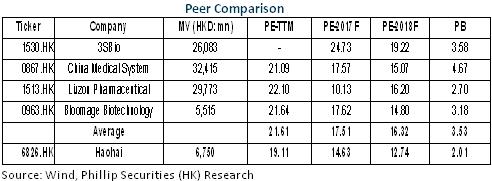

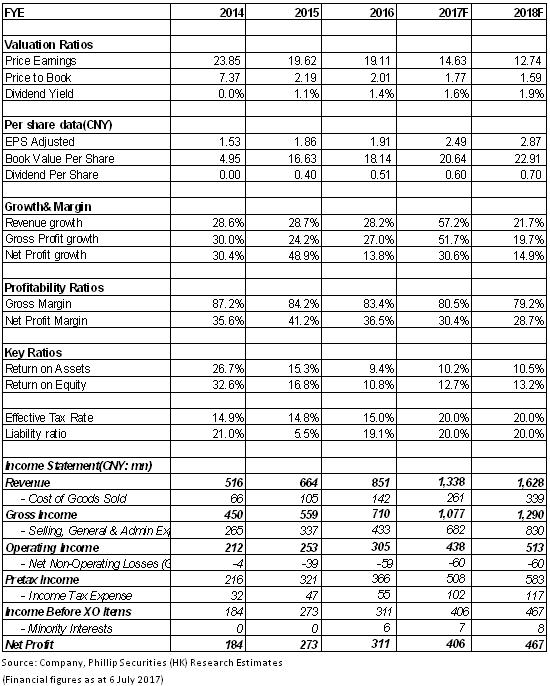

Overall speaking, Haohai's core products take leading positions in the market. Relying on broad market in medical cosmetology, ophthalmology and other fields, the company is expected to maintain fast growth. With R & D strengths, the company gains a momentum of sustainable development. With over RMB2 billion in cash, it also enjoys a promising prospect for the expansion and M&A. We offer the company an estimation of 18x EPS in 2017, with a target price of HKD51.2, to maintain "Buy" rating. (Closing price as at 6 July 2017)

Rapid Development of Major Business in 2016

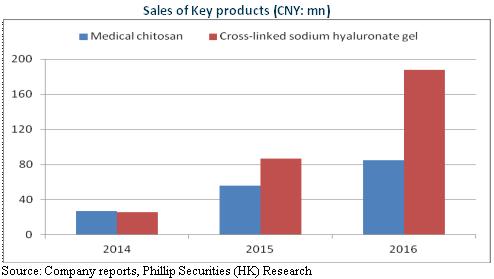

The revenue and net profit of Haohai Biological Technologies in 2016 reached RMB850 million and RMB310 million, respectively, representing year-on-year increase of 28.2% and 11.5%, respectively. Although the company's performance growth is slower than that of revenue, mainly due to a year-on-year drop of approximately RMB20 million in exchange gains, the major business still has achieved a rapid growth as a whole. In terms of orthopaedic products, sodium hyaluronate injection accounts for the largest proportion of the total revenue, whose revenue fell 11.2%, with the proportion decreasing from 34.3% in 2015 to 23.8%, mainly because the fall in the bidding price led to a decline of more than 10% in average selling prices. Besides, the tendering work has not finished yet in many cities and provinces and dealers show inert interest in purchase. However, at present suppliers are in low inventory, and future shipments are expected to rise by single digit. On the contrary, the revenue of another orthopaedic product called medical chitosan increased by 50.9% to RMB84.88 million. As a unique product of the company, with prominent competitive advantage, it has entered into Beijing, Shanghai, Guangdong and Shandong Province, etc. Almost unaffected by tender, the current 10% proportion of the total revenue now is estimated to rise considerably in the medium term.

In terms of medical aesthetics and wound care products, as of 2016, fifteen hyaluronic acid (HA) dermal fillers had been on the market. The revenue of the star product "Haiwei" rose by 115% to RMB190 million, taking up 22% of total from 13.1% in 2015. Moreover, developed independently by the company, the second-generation Janlane has earned the Machinery Registration Certificate of CFDA in September 2016 and came into the market at the end of 2016. Haiwei applies to facial wrinkles and folds while Janlane goes for lips and cheeks. The product mix, complementary and differentiated, is hopeful to help achieve a high-speed development by over 50%.

Epitaxial Acquisition Leads New Impetus to the Development of Ophthalmic Business

In 2016, the revenue of ophthalmic products also increased by 65.9% to RMB120 million, accounting for 14.1%, up from 10.9% previously, which was attributed to the ongoing acquisitions of ophthalmic enterprises. The company successively completed the acquisition of a 60% stake in Shenzhen New Industries, Henan Universe, 100%, Zhuhai Etam, 98%, etc. and gradually moved into high-valued ophthalmic consumables business.

In April 2017, the company continued to announce a 70% stake acquisition of Contamac, a contact lens and IOL(intraocular lens) material manufacturing company in UK, with a purchase consideration of approx. HKD240 million, corresponding to 12.8x EPS in 2017. And with earlier acquisitions, the company has developed the capability of producing three types of ophthalmic viscoelastics, five intraocular lens, one eye drops as well as raw material of IOL and has basically finished the industrial chain layout of the cataract surgery industry. Cataracts are the leading cause of blindness of the public in China. At present, only 1,500 people per million people have received cataract surgery in China, falling far behind America and India, with the number of 9000 and 6000, respectively. This industry, therefore, enjoys an enormous potential for development. We expect ophthalmic business will be a new impetus to the development of the company.

New NDRL is beneficial to expand product market

In late February 2017, RHEGF (Recombinant Human Epidermal Growth Factor) was adjusted into category B drug in terms of the new NDRL(national drug reimbursement list) from the restrictions for the use of medicines in work-related injury insurance. It is the only EGF product with the same structure as natural amino acid in human body in the country. Registered as a kind of new drug in 2001, rhEGF won the second prize of National Scientific and Technological Progress Award in 2002 and with a market share of 16.2% in 2015. In the past two years, rhEGF contributed approx. RMB36 million to the company's total revenue, accounting for about 5%. We believe that the adjustment of the restrictions for the use of medicines is beneficial to expand the new market for this product. From the beginning of 2018, its contribution is expected to increase faster.

Risks

The price reduction on products exceeds expectations;

The promotion of the new products fails to meet expectations;

The performance of M&A enterprises falls short of expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()