-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

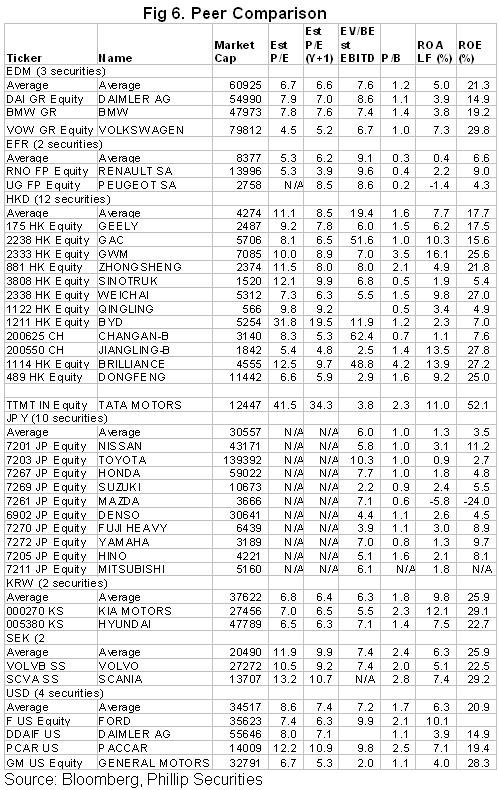

Geely (175.HK) - Stable 12H result with surged exports

Friday, August 31, 2012  14361

14361

Geely(175)

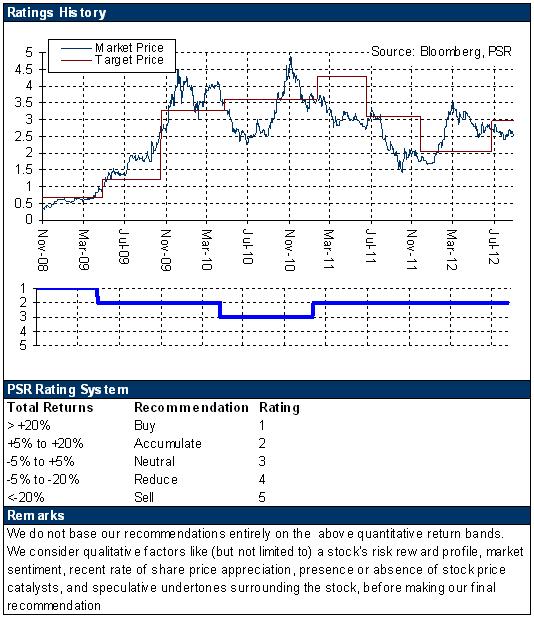

| Recommendation | Accumulate |

| Price on Recommendation Date | $2.540 |

| Target Price | $2.980 |

Weekly Special - 3306 JNBY Design Limited

Company Profile

Headquartered in Hangzhou, Geely is one of big-3 Chinese local brand car producers, with manufacture bases in Linhai, Ningbo and Luqiao, Shanghai, Lanzhou, Xiangtan, Jinan Chengdu, and a R&D center/production base from DSI in Australia. It has more than 30 car models under three sub-brands -- Emgrand, Gleagle and Englon.

Summary

-Geely releases mid-2012 report:

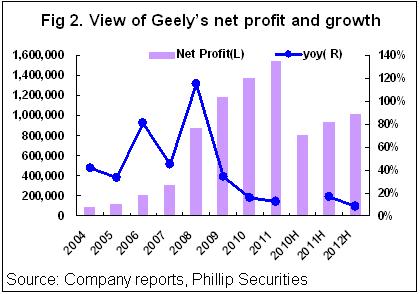

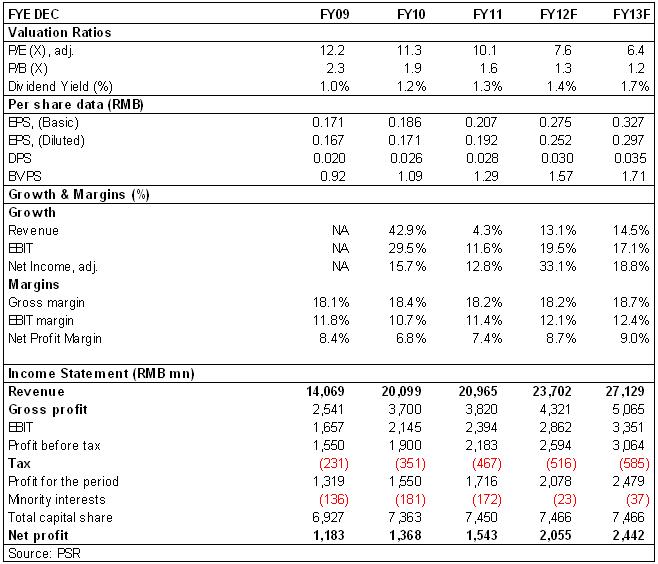

Operation Turnover increased by 6% to RMB11.177 billion from a year ago, operating cost up by 6% year-on-year, and yearly profit attributable to shareholders of the parent company reached RMB1.02 billion, up by 8.7% from the same period of previous years. The Company realized diluted EPS RMB0.125, rising by 9%, and performance was in line with the expectation. Meanwhile, interim dividends were not distributed. Main drive for performance growth was the outbreak of the export market and satisfactory demand of Emgrand brand. In addition, government subsidy income increased by 19% year-on-year to nearly RMB100 million, with much performance increase.

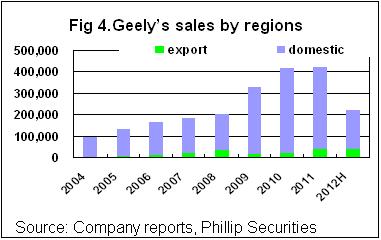

-Strong export growth is the key highlight.

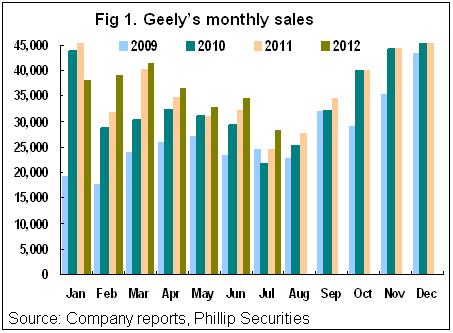

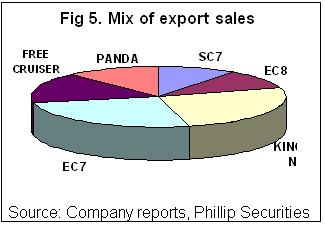

The Company H1 sold 222,000 vehicles, up by 4.2% from the same period of last year, taking 48.3% of the yearly sales goal of 460,000 units. Among them, Domestic market regression accelerated sales down by 9%, but export demand remained strong, sales up by 199% to 40,000 units, which offset the unfavorable effect of domestic sales. Geely overseas market entered rapid growth period, and yearly export is expected to break 85,000 units, up 115% year-on-year.

-Product mix continues to move up, but gross margin levels off.

Global Hawk brand which made up 36% share continued to slide, among which Free Ship and Vision brands declined by 20% and 44% from last year, while high-end Deidro Delux sales grew by 36% to 69,000 units. Driven by released capacity of Cixi factory completion, Deidro Delux EC7 model sales rose by 38%, and average monthly sales outnumbered 10,000 units, which accounted for 27% of Geely Automobile total sales. The Company ex-factory prices remained steady, while strong sales growth contributed by EC7 was offset by high favorable promotions of low-end models and cost increase leveled off gross margin to 17.4%.

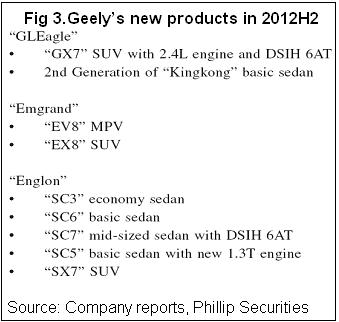

-New models and transmission gearbox 6AT are expected to improve H2 performance.

The July sales of The Company first SUV model GX7 reached 3,000 units, with good performance, and it will impact monthly sales of 5,000 units in H2. Geely plans to launch nine new models including EX8 and SC6 in H2 2012, Xiangtan factory started to mass-produce 6AT gearbox in end-June, which enabled the Company to launch more new models equipped with 6AT in H2. we predict that higher product price-performance ratio is expected to increase H2 sales and positively boost the Company gross margin.

Valuation and Rating.

After Geely successfully purchased Volvo, remarkable progress was made in safety and quality aspects, which improved the Company brand image. We believe supported by new car effect and export boom, H2 sales will be better than expected. We maintain its 12-month target price of HKD2.98, corresponding to 9.7 times and 8.2 times of diluted EPS in end-2012 and end-2013, a premium of 17% over the present price, “accumulate” rating maintained.

Risk factors.

Economic slide severely weakens car consumption demand; raw material cost substantially increases; fierce market competition and price decrease range go beyond the expectations; overseas market risk; urban congestion spreads purchase restrictions, etc.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()