-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Harmonicare (1509.HK) - Recent Correction Provides Opportunity

Tuesday, January 17, 2017  21714

21714

Harmonicare(1509)

| Recommendation | Buy |

| Price on Recommendation Date | $4.450 |

| Target Price | $5.530 |

Weekly Special - 3306 JNBY Design Limited

We had a conference call with Mofei Xiao, Deputy Director of Securities Department to conduct research on Harmonicare on 11 Jan,2016.

Company Overview

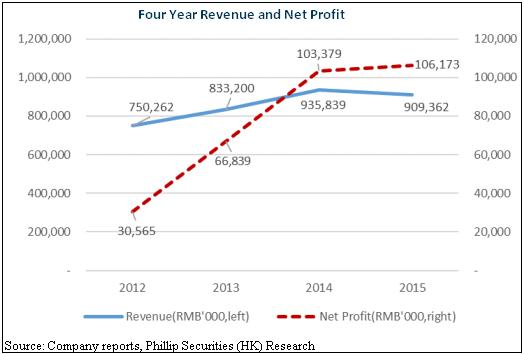

Harmonicare has two businesses: provision of hospital services segment and supply of pharmaceuticals and medical devices segment. Revenue from the provision of hospital services segment reached RMB874.2 million in FY15, accounted for 96.1% of the total revenue. And the Group's revenue from the supply of pharmaceuticals and medical devices was RMB35.13 million. This business segment accounted for 3.9% of the total revenue. Revenue from the provision of hospital services segment accounted for over 94% for the last three years. Revenue and profit and total comprehensive income attributable to equity holders of the company increased at CAGR of 6.6% and 51.4% respectively from FY12 to FY15.

The businesses of provision of hospital services segment include Obstetrics services, Gynecology services and Other healthcare services.

Obstetrics services: The company provides comprehensive prenatal, delivery and postpartum care services to mothers. They also provide diagnostic and preventive medical care to newborns. In addition, the obstetrics services include ancillary services such as pelvic floor rehabilitation, postnatal care and breast feeding support.

Gynecology services: The gynecology services cover gynecologic inflammation, gynecologic oncology, female reproductive system disorder treatment, endometriosis, female reproductive tract abnormalities, pelvic floor dysfunction in aged women and other common gynecologic diseases. They also offer birth control management, infertility testing and treatment, menopausal care and health screening services.

Other healthcare services: Some of the Group's hospitals also provide pediatrics services for common diseases, dental care and medical aesthetic services.

The Group was successfully listed on the main board of Hong Kong Stock Exchange on 7 July 2015. The offer price was HK$7.55. CDH, Honeycare, Harmony Care and Mighty Sky respectively entered into sale and purchase agreements to sell approximately 10.37%, 8.23%, 1.77% and 6.07% of the total issued shares at an average price of HK$6.54 per share to Taikang Insurance Group Inc. in November 2016.

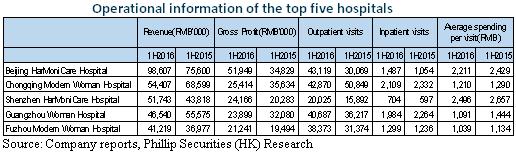

Operational Information of the Top Five Hospitals

By the end of June 2016, the Group owned 11 hospitals in seven core cities such as Beijing, Shenzhen, Guangzhou and Chongqing. And the company announced the acquisition of Heilongjiang HarMoniCare Hospital on 21 Dec 2016. The following table sets forth the revenue, gross profit and key operational information of the top five hospitals for 1H2016.

Target Customers

The customers are primarily female patients who receive medical care and related services at the Group's hospitals. Their target customers are patients that generally have an annual household income of above RMB200,000.

1H2016 Business Overview

During 1H2016, the Group recorded a revenue of RMB429.8 million with a decrease of 3.4% YoY. The revenue from the provision of hospital services accounted for 98.3% of the total revenue in 1H2016. The gross profit margin dropped to 48.0% (1H2015:50.6%). The net profit attributable to equity holders of the Company was RMB40.3 million, representing an increase of 5.0% YoY. The increase in the net profit attributable to equity holders of the Company was primarily due to the substantial increase in profit of Beijing HarMoniCare Hospital, while the increase in interest income and foreign exchange gain partly offset the decrease in the profit of other hospitals.

Affected by the “Wei Zexi Incident”, the number of inpatient visits at the 11 hospitals was 11,280, representing a decrease of 8.4% as compared with 12,309 in 1H2015. However, hospitals which specialize in high-end obstetrics services maintained steady growth. Beijing HarMoniCare Hospital, in particular, recorded significant growth in revenue and profit in 1H2016, with a revenue growth of 30.4%, a gross profit growth of 49.2% and a net profit growth of 73.8% YoY.

Industry Overview

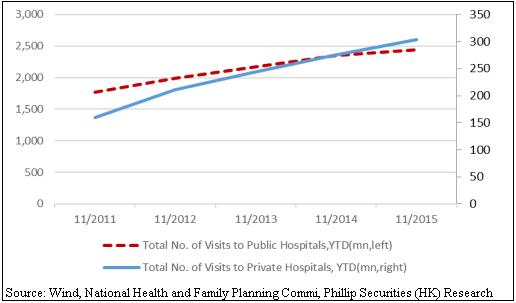

The CAGR of the total No. of visits to private hospitals and public hospitals from January to November was 17.5% and 8.4% respectively from 2011 to 2015.

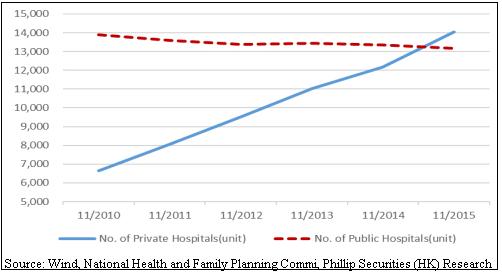

The number of private hospitals increased from 6,644 at the end of November 2010 to 14,449 at the end of November 2015 at a CAGR of 16.2%, while the number of public hospitals decreased from 13,904 at the end of November 2010 to 13,177 at the end of November 2015.

The National Health and Family Planning Commission of PRC pointed out in the relevant explanation of China Health and Family Planning Statistics Bulletin" that in 2015 the private hospitals accounted for 52.6% of the total number of hospitals (increased by 4.1% from last year) and non-public medical institutions accounted for 22.3% of the total outpatient volume, with an increase of 0.2% compared with previous year. Pluralistic medical pattern is forming.

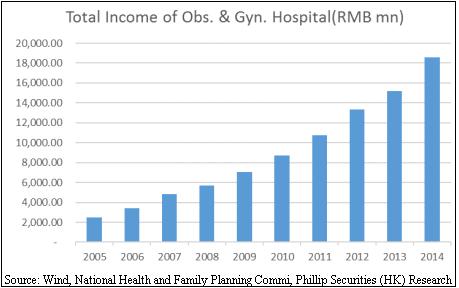

The total income of obstetrics and gynecology hospitals increased at a CAGR of 25.0% from 2005 to 2014.

The Key Drivers of the Private Obstetrics and Gynecology Specialty Healthcare Services Market in China

The future of the private obstetrics and gynecology specialty healthcare services market in China is optimistic for the following reasons:

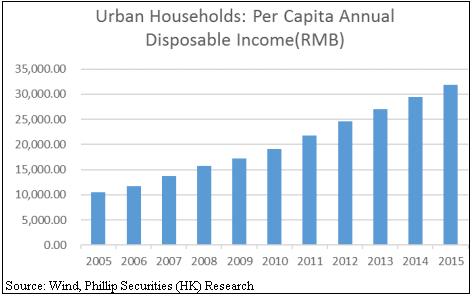

Disposable income is increasing: From 2005 to 2015, per capita annual disposable income of urban households increased from 10493.03RMB to 31790.30RMB in 2015 with a CAGR of about 11.7%.

The implementation of two-child policy: In November 2011 China allowed couples to have two children if both of the parents are an only child; in December 2013, China implemented the policy that allowed couples to have two children if one of the parents is from a single-child family; in October 2015 the universal two-child policy is proposed.

The pursuit for good quality medical services by the new generation of Chinese women: According to the China Household Financial Survey (CHFS) in 2015, the number of China's middle class was around 204 million. The new generations of Chinese women pursue higher standards, higher efficiency, higher quality medical services and they have higher requirements for the comfort of medical environments, and they are willing to pay more to achieve their wishes.

Policy support for private hospitals: On June 15 2015, General Office of the State Council issued the Circular on Several Policy Measures to Accelerate the Development of Social Medical Development. It pointed out that it is necessary to promote the development of private hospitals until they are large enough and have high standards, and accelerate the pattern of public hospitals and private hospitals developing together.

Prospects for Development

The company's future strategy to build new hospitals is to focus more on high-end obstetrics. The target cities are Tier I and Tier II cities. Target customers have higher second child birth rate than the overall population. In addition, the company has high standards for its medical services, and it has pricing ability. The company is supported by the national policy, and the current cash flow is abundant without any interest-bearing loans. Future expansion and acquisitions as well as upstream and downstream industry chain extension are worth waiting. The second largest shareholder Taikang is committed to the layout of the health industry, and it also actively promotes the development of insurance, asset management and medical care. The acquisition led to the expectation on the future cooperation of the two sides.

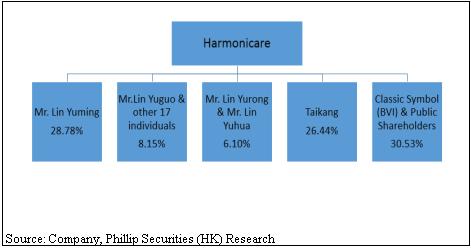

Shareholding Structure

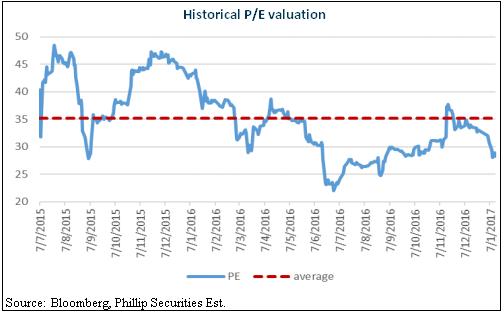

Valuation

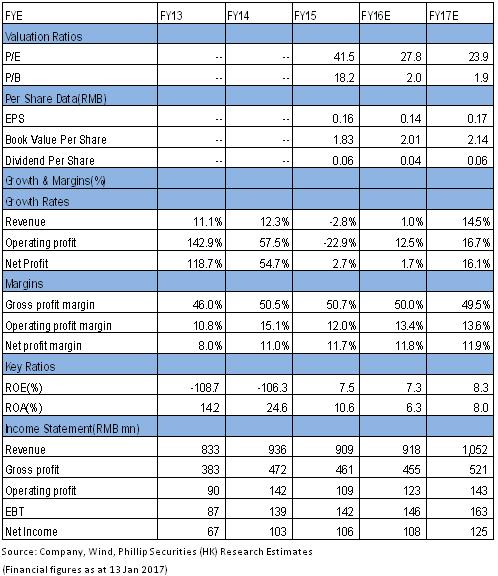

Buy Rating is given with TP of HK$5.53. We expect net profit growth of 1.7/16.1%, driven by 1.0%/14.5% revenue growth. The stock price experienced correction recently and we think the price is undervalued. Our TP of HK$5.53 represents 34.6x FY16E P/E. (Closing price as at 13 Jan 2017)

Risk

The influence of “Wei Zexi Incident”;

The impact of newly-opened hospitals on short-term financial performance.

Q&A

1、Will the company focus more on obstetrics in the future? Will the infertility business develop less because of Wei Zexi Incident?

Here's our future plan. Gynecology as a traditional department has the reason to exist, but we won`t put the main resource into this area, we won`t expand this area any more. Our future new hospitals will focus more on high-end obstetrics, which is similar to Beijing HarMoniCare. As for infertility business, we now have an overseas referral IVF business. If the customers are diagnosed to be difficult to get pregnant naturally, we can provide overseas referral. Once they are successfully pregnant overseas, they will come back for our package. We also get commission through the referral service. We haven`t obtained the IVF license yet, so the company will develop the subject of IVF by cooperating with other institutions.

2、Does the Wei Zexi Incident inpact the company less now?

Yes, it impacts less now.

3、Will the hospitals in Guangzhou and Chongqing make any adjustments? How to adjust specifically?

We will increase the proportion of high-end obstetrics by decorating wards and adding single rooms. We will also develop some high-end packages to enhance the quality of service.

4、The two-child policy was announced more than one year ago, but the number of newborns in 2016 was only about one million, way below expectation. Has the company adjusted the expectation for the policy? What does the company expect the policy would bring to the company?

The company has done some market research. Now our future plans are developing high-end obstetrics in target Tier I and Tier II cities. The target customers in such markets have more desire to have a second child than the overall population. Now people's concern about having a second child is mainly the economic factors. Our high-end obstetrics is mainly for the middle class and above, they have better economic conditions and more desire to have a second child. Beijing HarMoniCare already had a lot of second-child cases, the second child birth rate is higher than the overall market.

5、What's the revenue and net profit growth forecast in FY17?

We acquired Heilongjiang HarMoniCare, the company is expected to maintain good growth in 2017.

6、The majority of the company's net proceeds in FY15 is not used yet. Is it because of “Wei Zexi Incident” which affects the pace of expansion? What is the plan for the future use of the proceeds?

Yes, it's affected by Wei Zexi Incident. We are more cautious about acquisitions, M&A and opening new hospitals. The projects we are considering at year end may be confirmed soon. The future use of the proceeds will be almost the same as what was said in the prospectus, but the specific cities may have some changes according to our market research.

7、Is the goal of having 20 hospitals in 2018 still unchanged?

Yes, the goal is to have 20 hospitals in 2018.

8、How did Heilongjiang HarMoniCare turn losses into gains?

Because the market cultivation process takes time. In addition, the management of Heilongjiang HarMoniCare has made some positive movements in marketing, department settings, it also recruited some very good doctors. It has turned losses into gains now. The future is expected to be better, and the IVF business is expected to start soon.

9、The net assets of Heilongjiang HarMoniCare is -97.14 million, is there any concern about it? Did the company consider the factor when pricing it?

The brand value and other factors will be taken into consideration in the pricing process.

10、The company recently introduced Taikang Insurance as the main shareholder. How will the company and Taikang cooperate in the future?

Please pay attention to the announcement to see whether and how we will cooperate in the future.

11、For Baotou Modern and other hospitals which have been sold, if the businesses improve, will they be acquired back?

It's possible. But we will consider the return to shareholders first. The hospitals need to meet certain standards first.

12、Is there any room left for the market share to increase?

As the largest chain group, the company has no competitors in China now. And the company cherishes the opportunities and advantages. The company will increase the intensity to do healthcare and services steadily. Hopefully the future development will be more solid. The company has confidence to increase market share in the future, and the company is confident about existing inner growth and outer extension. Beijing HarMoniCare got the international JCI certificate last November with a high score of 99.37. It is the affirmation of the company's good services and medical quality. The Group's other hospitals are also making efforts toward this goal.

13、The national consumption upgrade brings opportunities. Is the company confident that customers of public hospitals will choose the company?

We can see the trend now. The mid-end will go to the high-end market as a result of the increasing deliveries in Beijing.

14、How's the company's pricing ability in the future?

The prices of antenatal examination and delivery packages are adjusted every year. The company adjusts prices according to the market conditions and the research of competitors. The package prices always increase from past experiences but with different amounts. The company will adjust prices according to market conditions, the prices will increase overall as the labor costs rise. Company has high pricing ability because of the market's high demand.

15、How will the gross profit margin change in FY17 compared with FY15?

In FY17 the gross profit margin is expected to maintain at about 50%.

16、How will the SG&A/revenue ratio change in the future?

It will remain stable in the future. We won`t increase expenses in Baidu, and we are gradually increasing the proportion of expert lectures and community activities. The overall selling expenses are expected to be stable, general expenses are also expected to be stable.

17、 How's the future CAPEX/ revenue ratio?

It depends on new hospitals and M&A projects. It's uncertain now.

18、Is there any guideline for future dividend payout ratio?

The company hopes to bring shareholders stable return.

19、Still don`t need any bank loans in the future?

No plan at the moment.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()