-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Semir Garment (002563.SZ) - Q1 earning in line with expectation, divestment of Kidiliz improve profitability

Thursday, July 8, 2021  6754

6754

Semir Garment

| Recommendation | Buy |

| Price on Recommendation Date | $12.290 |

| Target Price | $14.950 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

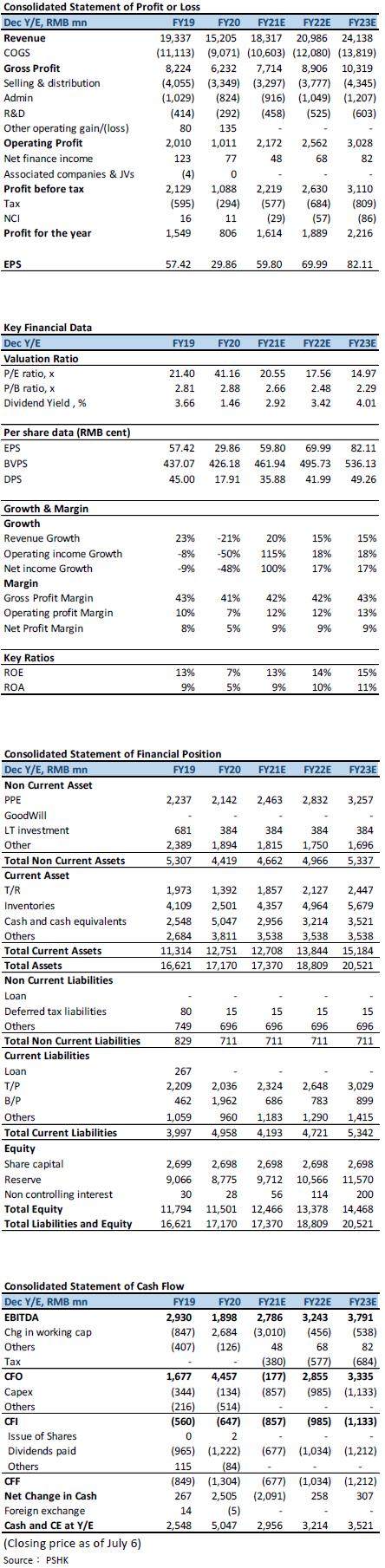

The company announced its results for 1Q21. In 1Q21, it recorded revenue of CNY 3.31 billion, an increase of 20.9%; net profit attributable to parent was approximately CNY 353 million, an increase of 1916.8% Yoy, and a 1.7% increase from the same period in 2019. Excluding the impact of Kidiliz's spin-off, the company's revenue and net profit increased by 50% and 226% respectively Yoy. After spin off Kidiliz, the company has improved its cost control, and its overall revenue and profit performance are in line with our expectations.

Divide by sales channel, the company's online retail sales volume has increased by more than 40% Yoy. Among them, children's wear and adult casual wear have recorded more than 50% and double-digit growth respectively, and the overall online sales volume of the same period in 2019 also recorded a 30% increase; Overall offline retail sales volume recorded an increase of more than 60% which children's clothing and adult casual wear recorded 60% and 70% growth respectively. In terms of business segment, the sale volume of children's wear increased by about 50%-60% Yoy, and the Sales volume of adult casual wear increased by 40%-50% Yoy, mainly due to the low base in the same period last year. If compared with the same period in 2019, the Sales volume of children's wear and adult casual wear increased by more than 20% and a reduction of about 20% respectively.

Discounts and pricing improved, company GPM and NPM increased significantly,

The company's GPM during the period was 44.0%, an increase of approximately 2.9 ppts from 41.1% in the same period in 2020, mainly due to the company's improved price markup rate and discount. From the perspective of pricing, since 2H19, the company has continued to adjust the brand. The pricing multiple of the Balabala brand has increased from 3.5-4.0x to above 4.0x, and the pricing multiple of Semir has increased from 3.0x-3.5x to approximately 3.5x. The company's overall pricing multiple is about 4.0x; from the perspective of discounts, the company's average discount level in recent years is about 70% to 80% offline and 50% online. Affected by the epidemic, the company increased its discounts last year. The discount returned to the normal at the end of 4Q20.

After spinning off Kidiliz, the company's expense ratio during the period was significantly improved. The company's sales/management/R&D expense ratio was 19.4%/5.3%/1.36%, a Yoy decrease of 7.9/1.9/0.5 ppts. With the improvement in both expense ratio and GPM, the company's profitability has improved significantly. In 1Q21, the company's NPM was 10.6%, an increase of 10.1 ppts Yoy. In 1Q21, it recorded a net profit attributable to the parent of CNY 353 million, a Yoy increase of 1916.78%. This was mainly due to the company's low profit level due to the impact of the epidemic in the same period last year, resulting in high Yoy growth under a low base.

Profit forecast and valuation

Semir Garment has secured its leading position in the domestic children's wear and casual wear market. After the divestiture of Kidiliz, the company's profitability has improved significantly on a quarterly basis. After adjusting the pricing multiple, the impact of the partial divestment of Kidiliz on the income side was offset, and the company's profitability also increased significantly. The company has a leading advantage on the children's clothing industry and is expected to bring sustained growth to the company.

The company's performance in the first quarter of 2021 is in line with our expectations. After the divestiture of Kidiliz, it will have a short-term impact on the company's children's clothing segment revenue. However, the company has its own brand Balabala in the children's clothing business. By adjusting the pricing multiple, it is expected to continue to provide growth for the children's clothing business. In addition, after the divestiture of Kidiliz, the company has improved its admin expenses and sales expenses, and its overall profitability has increased. The company's first quarter reflects the actual impact of Kidiliz's divestiture on the company. We maintain the company's earnings forecast. The company's FY21E/FY22E net profit attributable to the parent is expected to be CNY 1.61 billion/1.90 billion, corresponding to FY21E/FY22E EPS of CNY 59.80/69.99 cents, considering the improvement of the company's brand image, we revised up company's target P/E to FY21E 25.0X, and the target price is raised to CNY 14.95, corresponding to FY21E/FY22E P/E of 25.0x/21.4x.

(Current price as of July 6)

Risk

1) The impact of COVID-19 continues

2) Overlapping positioning between brands

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()