-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Bank of China Hong Kong (2388.HK) - Lack of growth highlights

Wednesday, April 3, 2013  15722

15722

Bank of China Hong Kong(2388)

| Recommendation | Neutral |

| Price on Recommendation Date | $25.950 |

| Target Price | $27.050 |

Weekly Special - 3306 JNBY Design Limited

FY 2012 Summary

Growth in core business

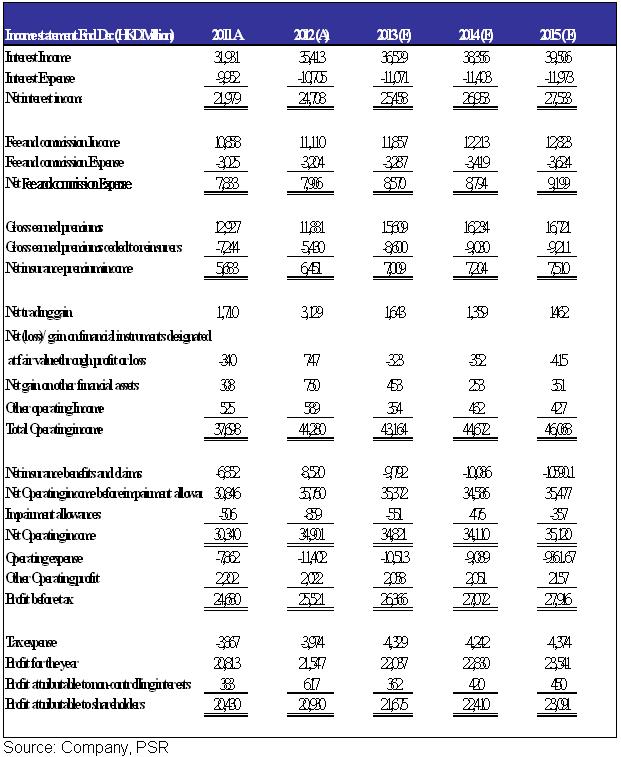

BOC HK's FY 12 performance was in line with our expectation:

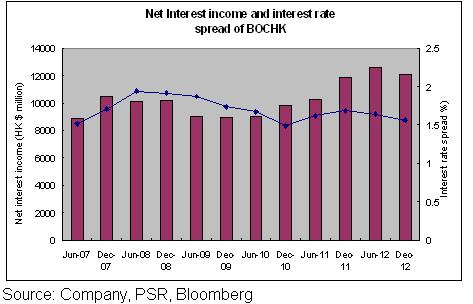

Net interest income achieved to HK $ 24.708 billion (HKD as below), up 12.4 % yoy or 27.29 billion HKD, NIM improved to 1.6%

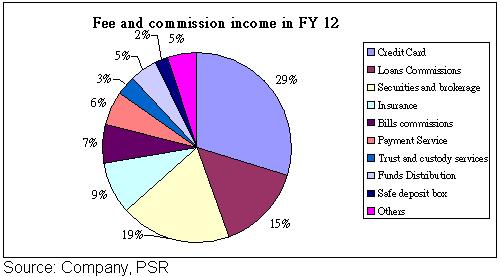

Net fees and commissions, rose 0.9 % yoy to 7.906 billion HKD,

Net trading income increased by 83% yoy to 3.129 billion HKD, mainly due to net trading income of the foreign exchange trading and related products, driven by an increase of 558 million HKD, or 39% yoy. The interest rate instruments and items under fair hedge rose by 74 times yoy to 900 millions. Accounted for the vast growth of the trading business.

Profit before tax reached 25.521 billion, an increase of 3.41% yoy.

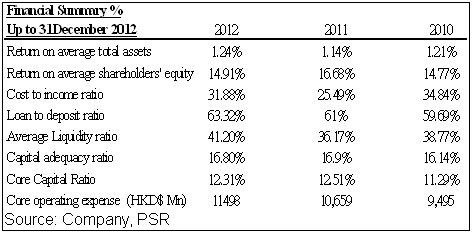

Due to the Lehman Brothers mini-bonds related expense, total operating expenses increased by 45% yoy to 11.402 billion, core operating expenses rose 7.9%, or 839 million.

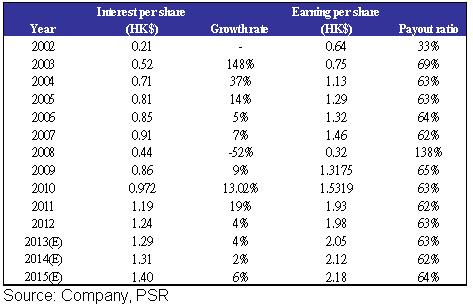

In FY 12 basic earnings per share was HK $ 1.9796, up 2.46 % yoy, dividend increased 4.2% yoy to $ 1.238, to maintain a 62.5% payout ratio as past. However, the FY 12 result of BOCHK was not impressive, thus, we downgrade the investment rating to "Neutral" and rise target price to HK$27.05.

Based on the development of RMB business and the Group's long-term advantages, coupled with stable dividend payout policy, investors can buy for long-term holding at lower price

Net Interest Income

Due to the dilutive effect of RMB business reduced, NIM rallied by 28bp in 2013

However the deposit market is increasingly competitive, the Group's loan to deposit ratio increased to 63.32%. Net interest income is still up to $ 24.708 billion, up 12.4 % yoy or 2.729 billion.。We expect a strong demand in offshore RMB lending, which let a keen competition in attracting deposit, negative effect to NIM.

Fee and commission income

Group's net fee and commission income also recorded a slight growth, up 0.9 % yoy to 7.906 billion, the growth momentum mainly driven by credit cards, insurance business, up 14.5% yoy. Securities brokerage income fell 24% yoy, due to the volatility market conditions in 2012. We expected the debt crisis in Europe will be released, market sentiments improved, and the market turnover rose, securities brokerage income is expected to rebound in 2013.

Major Risk

European sovereign debt crisis continues to worsen, affect global economy

Group's growth rate is slower than we expected

Chinese economic hard landing

Valuation

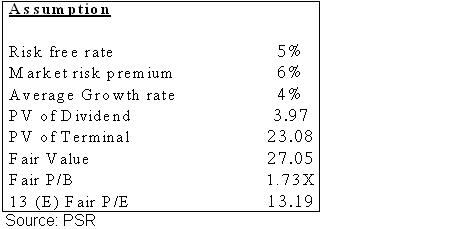

BOC Hong Kong's nine-year average P/B is about 2 times, while the current price P/B is about 1.8 times. With Europe's debt crisis slightly eased, and the opportunities of Rmb internationalization, the Group's P/B is expected to back to 2 times which is near our target price $27.05.

Dividend Policy

DDM Model

Due to the trend of Rmb internationalization o, we expect that the Group will grow steadily, dividend per share will be HKD $ 1.29 in 2013. Assume the growth rate will be 4%, we use dividend discount model calculated the fair value per share is HK $ 27.05. The corresponding estimated P/B is about 1.73 times and P/E is 13.19 times.

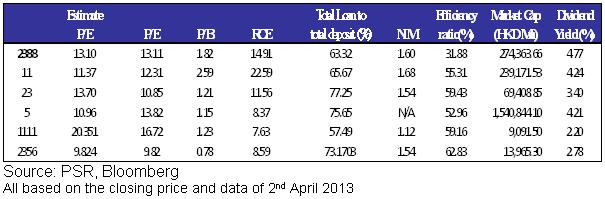

Peers Comparison

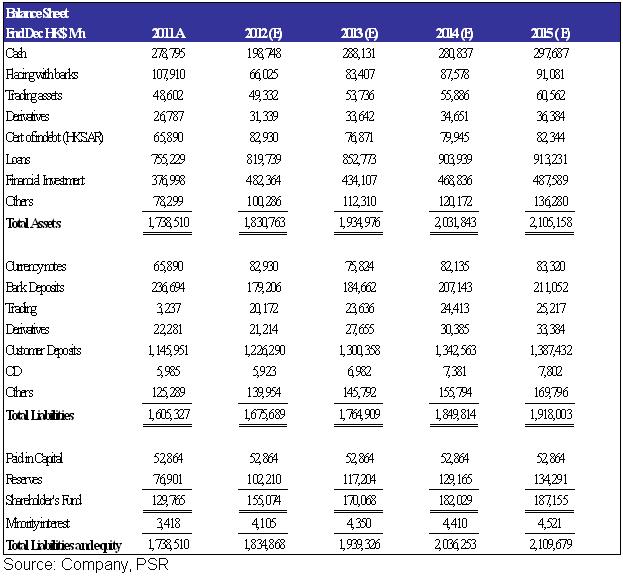

Financial Status

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()