-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

JNBY (3306.HK) - Steady Growth with Attractive Dividend Policy

Thursday, April 13, 2017  24807

24807

JNBY(3306)

| Recommendation | Accumulate |

| Price on Recommendation Date | $5.950 |

| Target Price | $6.600 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

- The total revenue in 1HFY17 was RMB1,310.4 million, representing a YoY increase of 22.4 %. The net profit in 1HFY17 was RMB227.9 million, representing a YoY increase of 24.0%.

- The total number of retail stores globally increased to 1,498 as of 31 December 2016. JNBY is developing well globally.

- Same store sales growth rate of the retail stores reached 11.3% in 1HFY17. In FY2014, FY2015 and FY2016 the retail stores achieved same store sales growth of 0.1%, 7.1% and 8.3% respectively.

- The company upholds the natural concept when choosing materials and the products are differentiated and have high brand recognition and customer viscosity. The company puts a lot of emphasis on "Fans Economy". The company is also building a multi-brand and multi-category lifestyle platform, with expansion and imaginary potential.

- The dividend policy is attractive. The company has adopted a general annual dividend policy of declaring and paying dividends on an annual basis of no less than 75% of the total net profit attributable to the Group for any particular fiscal year.

Company Business

JNBY is a designer brand fashion house based in China. The company designs, promotes and sells contemporary apparel, footwear and accessories for women, men, children and teenagers as well as household products.

Designer brand fashion products usually feature strong designer characteristics and iconic styles that can be easily identified. China's designer brand fashion market expanded rapidly, increasing from RMB11.1 billion in 2011 to RMB28.2 billion in 2015, representing a CAGR of 26.2%.

According to CIC, there were over 300 market players in the designer brand fashion industry in China, with the top five players accounting for 29.3% of market share in terms of retail sales, including online and offline sales, in 2015. JNBY had the highest retail sales and a market share of 9.6% in 2015 among designer brand fashion companies in China.

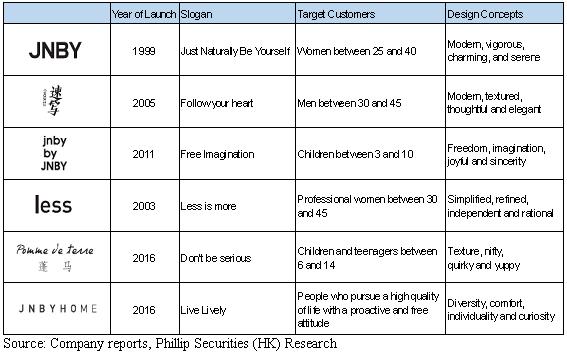

The brand portfolio currently comprises six brands — (i) JNBY, (ii)CROQUIS, (iii) jnby by JNBY, (iv) less, (v) Pomme de terre and (vi)JNBYHOME, each targeting at a distinct customer segment and having a uniquely defined design identity based on the Group's universal brand philosophy — “Just Naturally Be Yourself”.

The following table shows the description of the six brands.

The omni-channel interactive platform is important to JNBY. The omni-channel interactive platform includes retail stores, online platforms and social network platform on WeChat.

The Revenue

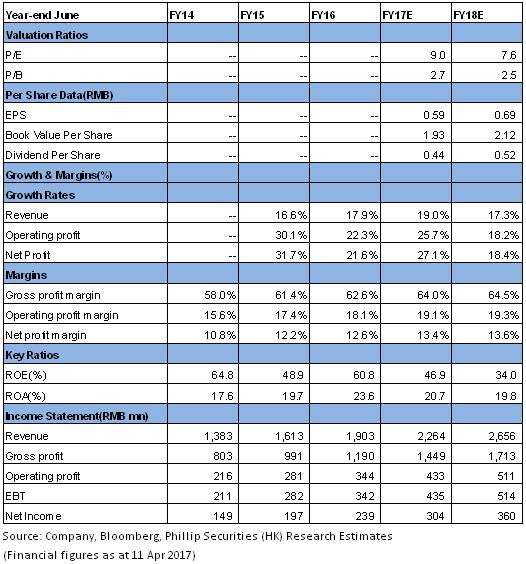

The revenue increased from RMB1,383.4 million in FY2014 to RMB1,902.6 million in FY2016, representing a CAGR of 17.3%. The net profit increased from RMB149.9 million in FY2014 to RMB239.3 million in FY2016, representing a CAGR of 26.5%.

The total revenue in 1HFY17 was RMB1,310.4 million, representing a YoY increase of 22.4 %. The net profit in 1HFY17 was RMB227.9 million, representing a YoY increase of 24.0%.

The company gradually reduced dependence on the women's segment. The ratio to revenue was 79.8%、74.4% and 69.3% respectively in FY2014, FY2015 and FY2016. Men and Children's segments accounts for higher percentage gradually.

Revenue from online channels accounts for 7.4% in 1HFY17. Revenue from online channels accounts for 8.3%, 7.9% and 7.5% respectively in FY2014, FY2015 and FY2016.

Retail Network and Internationalization

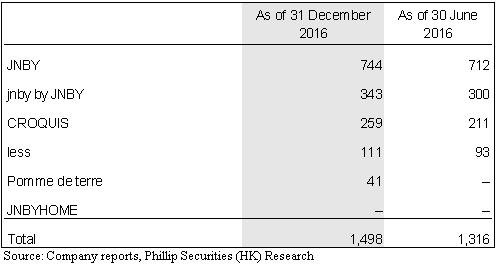

The total number of retail stores operated by JNBY globally increased from 1,316 as of 30 June 2016 to 1,498 as of 31 December 2016.

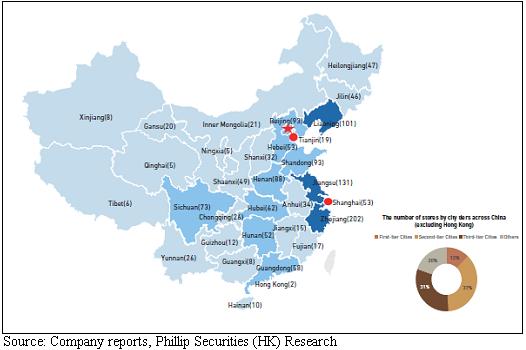

The following map shows the geographic distribution of the retail stores (including distributor-operated and self-operated stores) across China and Hong Kong as of 31 December 2016 as well as the distribution of stores by city tiers across China:

According to the prospectus, JNBY's sales also extended to 12 countries or regions overseas. JNBY operates a store in Hong Kong. In addition, the company sells their products to third parties that operate stores in 11 other countries and regions, including Japan, Russia, Taiwan, the United Arab Emirates, Canada, Georgia, Kuwait, New Zealand, Thailand, the United States and South Korea, in order to leverage the local contacts and retail experience of these third parties. As of 30 June 2014, 2015 and 2016, there were 34, 38 and 29 such overseas stores respectively.

Same Store Sales Growth

Same store sales growth rate of the retail stores reached 11.3% in 1HFY17. In FY2014, FY2015 and FY2016, the retail stores achieved same store sales growth of 0.1%, 7.1% and 8.3% respectively.

The Group's overall gross profit margin improved from 62.6% in 1HFY16 to 64.4% in 1HFY17, which was primarily attributable to the continuous increase in the sales of products of CROQUIS, jnby by JNBY and less brands and the generally higher profit margins of those products.

Advantages of the Company

The company upholds the natural concept when choosing materials and the products are differentiated and have high brand recognition and customer viscosity. The company puts a lot of emphasis on "Fans Economy". The company will also build a multi-brand and multi-category lifestyle platform, with expansion and imaginary potential. JNBYHOME is a new brand launched in 2016 with expansion potential.

As a noticeable indicator for successfully translating customer loyalty into revenue, the revenue contributed by the members as a percentage of the total retail sales increased from 40.2% in FY2014 to 46.0% in FY2015 and further to 56.7% in FY2016.

As of 31 December 2016, JNBY had over 1.6 million members (as of 30 June 2016: over 1.2 million) with more than 1.1 million WeChat accounts (as of 30 June 2016: over 720,000). The number of active members for the year 2016 was over 230,000 (FY2016: over 190,000).

The cash flow is healthy and the company has sufficient cash on hand. The dividend policy is attractive. The company has adopted a general annual dividend policy of declaring and paying dividends on an annual basis of no less than 75% of the total net profit attributable to the Group for any particular fiscal year.

Valuation

Accumulate Rating is given with TP of HK$6.60. We expect net profit growth of 27.1%/18.4% in FY2017/FY2018, driven by 19.0%/17.3% revenue growth. Our TP of HK$6.60 represents 10.0/8.4x FY2017E/FY2018E P/E. (Closing price as at 11 April)

Risk

The inventory level gets higher;

The apparel industry faces intense competition.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()