-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Inner Mongolia Yili Industrial Group (600887.CH) - Solid leading position maintained

Tuesday, December 8, 2015  13156

13156

Inner Mongolia Yili Industrial Group(600887)

| Recommendation | BUY |

| Price on Recommendation Date | $15.080 |

| Target Price | $20.000 |

Weekly Special - 3306 JNBY Design Limited

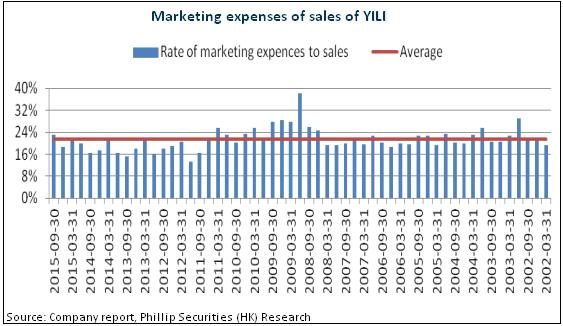

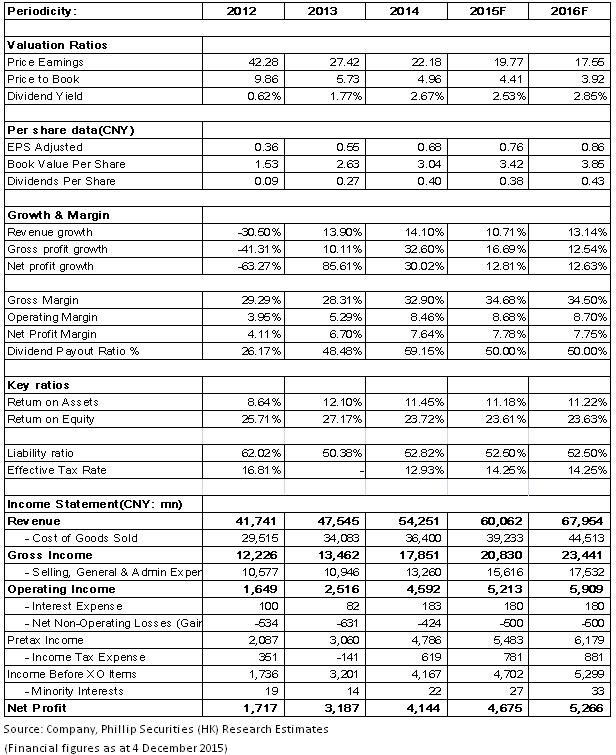

In the first three quarters of 2015, Yili recorded a total revenue of RMB 45.88 billion, which increased by 9.1% yoy; net profit attributable to shareholders reached RMB 3.64 billion, which grew by 2.2% yoy, and thus earnings per share reached 0.59 yuan. The performance less than expected was mainly due to the weakening of market-end demand causing the significant yoy increase of marketing expenses and promotion expenses. The rate of marketing expenses to sales in the first three quarters rose by 3 ppts to 21.1%, which totally offset the 2.3 ppts increase in gross profit margin brought by the lowered cost of raw milk.

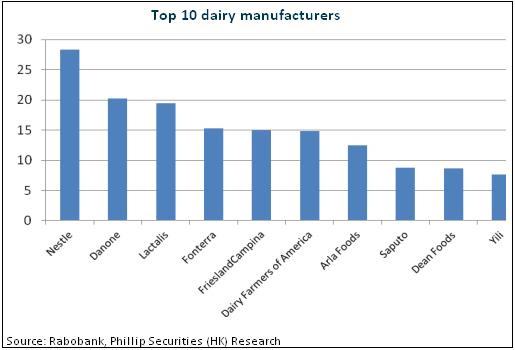

Even though the Company's business results did not meet expectation, the Company's solid leading position in the Chinese dairy products industry maintained in the first three quarters of 2015. According to the statistics by AC Nielsen, the market share of sales turnover of dairy products of Yili rose by 1.1 ppts yoy in the first nine months of 2015, reaching 20.4%, and kept the first rank in the industry. In addition, the Company announced in June the plan of acquiring Sanlian Dairy in Guizhou Province. Such acquisition marked the initial step of Yili's merger and restructuring, and thus future outward expansion is worth expecting. This may speed up the increase of the Company's market share, and also lead the Company to enter new growth stage.

Its profitability may improve. In Q3, the rate of marketing expenses to sales significantly increased by 6.9 ppts to 23.2%, which was the main reason for the downturn of the Company's business. However, we expect such uptrend would not persist. Since 2002, the average rate of marketing expense to sales reached 21.5%, and its hikes mainly occurred during 2008 when the global economy was under the threat of financial crisis, which was much more serious than the current economic slowdown. It is because the current round of economic structural transformation would focus more on the growth of consumption. Moreover, the price of raw milk would still keep at low level in short-/medium- term, and thus the gross profit margin of the Company would maintain at a higher level.

Moving towards a global leader of healthy diet products

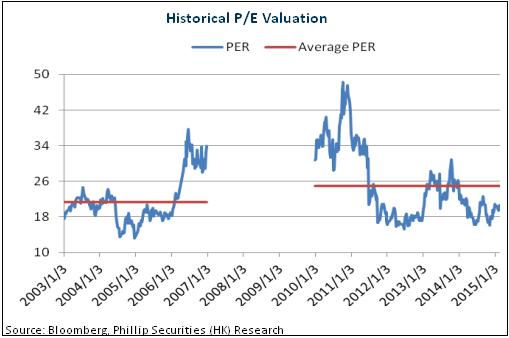

Yili has further consolidated her rank-one status in the dairy product industry in China, and the Company has comparative advantages on capital, brand name, cost control and sales channels etc. Yili will further outstrip competitors in the market, and may develop towards a global leader of healthy diet products through acquisition consolidation and globalized business arrangement. In Q3, China Securities Finance Corporation Limited has become the fourth largest shareholder of the Company and holds 3.03% of the Company's equity. Yili also constantly purchase its shares from the market, demonstrating confidence on the Company's development. We temporarily set the target price as 20 yuan based on a valuation of 26.25X of EPS in 2015e, and maintain the rating of “Buy”. (Closing price as at 4 December 2015)

Increase of expenses in Q3 dragged down business growth

In the first three quarters of 2015, Yili recorded a total revenue of RMB 45.88 billion, which increased by 9.1% yoy; net profit attributable to shareholders reached RMB 3.64 billion, which grew by 2.2% yoy, and thus earnings per share reached 0.59 yuan.

Overall, amid of economic slowdown and consumption downturn, which caused the dairy products industry in domestic Chinese market merely recorded a slight growth of 2.4%, the Company still demonstrated stable growth. This apparently showed its strength on competiveness in the market. In regard to different products of the Company, the sales turnover of room-temperature yogurt Ambrosial (An Muxi) surged 661% yoy; while the two signature brands of Yili Yoghourt: Chang Qing and Mei Yi Tian grew by 53.9% yoy and 37% yoy respectively. The high-end formula milk powder for infants, namely “Pro-Kido Premium” grew by 24% yoy, while Satine grew by 20% yoy.

In view of the Company's quarterly performance, the revenue recorded in 2015Q1, Q2 and Q3 amounted to RMB 14.99 billion, RMB 15.16 billion and RMB 15.73 billion respectively, which grew yoy by 14.4%, 5.6% and 7.7% respectively. Meanwhile, the net profit recorded in the first three quarters amounted to RMB 1.31 billion, RMB 1.36 billion and RMB 0.98 billion respectively, which grew yoy by 20.4%, 12.0% and -22.8% respectively. Based on the above data, we can conclude that the drop of profit in Q3 dragged down the Company's business growth, which is mainly due to the weakening of market-end demand causing the significant yoy increase of marketing expenses and promotion expenses. The rate of marketing expenses to sales in the first three quarters rose by 3 ppts to 21.1%, which totally offset the 2.3 ppts increase in gross profit margin brought by the lowered cost of raw milk.

Solid leading position maintained

Even though the Company's business results did not meet expectation, the Company's solid leading position in the Chinese dairy products industry maintained in the first three quarters of 2015. According to the statistics by AC Nielsen, the market share of sales turnover of dairy products of Yili rose by 1.1 ppts yoy in the first nine months of 2015, reaching 20.4%, and kept the first rank in the industry. Among Yili's products, the share of sales turnover of room-temperature liquid milk increased by 2.2 ppts yoy to 29.0%, while basic liquid milk increased by 2.1 ppts yoy to 35.9%. Both of these two products ranked the first in the industry and significantly surpassed peers. Meanwhile, sales turnover of cold drink also ranked the top in the industry for 22 consecutive years.

It is worth to note that the Company announced in June the plan of acquiring Sanlian Dairy in Guizhou Province. Such acquisition marked the initial step of Yili's merger and restructuring, and thus future outward expansion is worth expecting. This may speed up the increase of the Company's market share, and also lead the Company to enter new growth stage. In the annual report of 2014, Yili mentioned for the first time her strategic target of bidding the top five ranks of the global dairy producers, and becoming a high-end healthy food group by 2020. Being the leading dairy giant in China, Yili expands through acquisition and restructuring, which comply with both the norms of development of dairy industry as well as the state policies. In June 2014, the Chinese Government released the restructuring plan for dairy products industry: by the end of 2018, the top 10 domestic dairy brands would hold 80% of the market share.

Profitability may improve

In Q3, the rate of marketing expenses to sales significantly increased by 6.9 ppts to 23.2%, which was the main reason for the downturn of the Company's business. However, we expect such uptrend would not persist. Since 2002, the average rate of marketing expense to sales reached 21.5%, and its hikes mainly occurred during 2008 when the global economy was under the threat of financial crisis, which was much more serious than the current economic slowdown. It is because the current round of economic structural transformation would focus more on the growth of consumption.

Moreover, the price of raw milk would still keep at low level in short-/medium- term, and thus the gross profit margin of the Company would maintain at a higher level. According to the monitoring data by the Ministry of Agriculture, the current average price of fresh milk in domestic Chinese market still records a yoy decline of about 10%. In addition, the Company's product mix has been enhanced, with proportion of high-end products increase rapidly, and the profitability of high-end products is stronger. The current gross profit margin of the market-dominated room temperature liquid milk is only around 20% to 25%, but the gross profit margins of new high-end products such as Satine and Walnut milk etc was recorded as 35% or even higher than 40%.

Catalyst

More-than-expected sales of high-end products;

Faster-than-expected progress of outward expansion;

Faster-than-expected implementation of internationalized strategy.

Risks

Intensified competition among dairy product producers;

Rise of raw material cost;

Risk of food safety.

FINANCIALS

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()