-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

KERRY LOG NET (636.HK) - Regional Leading Property Enterprise Grows against Trend

Wednesday, May 18, 2016  13310

13310

KERRY LOG NET(636)

| Recommendation | No Rating |

| Price on Recommendation Date | $10.780 |

Weekly Special - 3306 JNBY Design Limited

Business Overview:

Kerry Logistics is a third-party logistics provider based in Asia. It manages a logistics facility portfolio of 45 million square feet in twelve Asian countries and regions, of which 24 million square feet are self-owned. Among the facilities managed by the Company, approximately 64% are located in the Great China Region, approximately 28% in ASEAN countries, and the remaining 8% are mainly located in South Asia, Australia and Europe. The main business activities of the Company are asset-heavy integrated logistics comprising logistics operations and Hong Kong warehousing business, as well as international freight forwarding operating under an asset-light strategy.

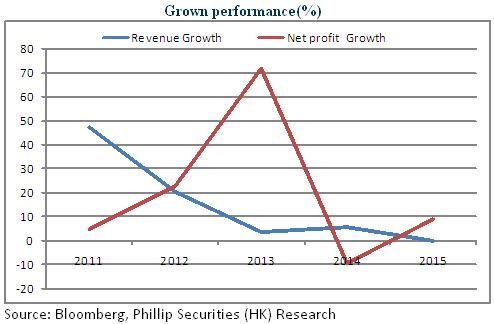

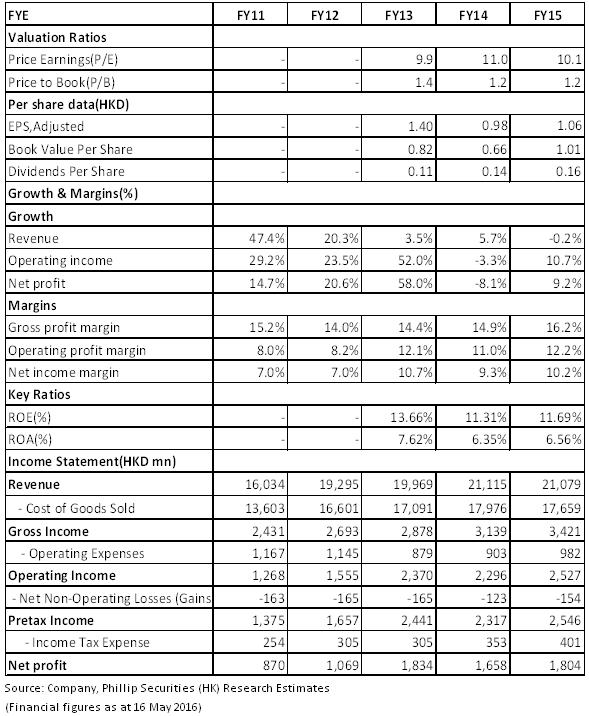

Turnover of the Company was maintained at HK$21,079 million in 2015, profit attributable to the shareholders recorded a 9% growth to HK$1,805 million, and gross profit rose by 8.96% year-on-year to HK$3,421 million. Earnings per share were HK$1.07, with total dividend paid of 16 HK cents for the year. The improvement in profit was due mainly to the Company's focus placed on strengthening service and profitability, as well as on its efforts made in cost control.

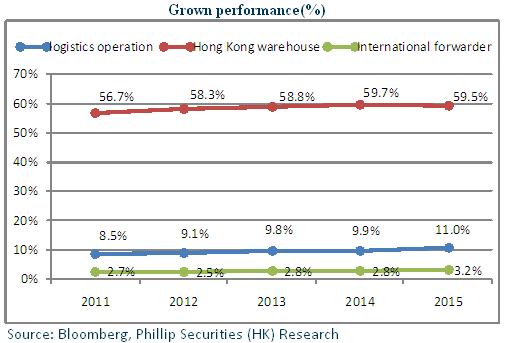

Logistics operations and Hong Kong warehousing business made substantial contributions to the performance of the Company. In 2015, logistics operations accounted for 47.5% in terms of turnover, contributing 56.3% of the profit of the Company. Profit margin rose to 11%, which was largely attributed to the expansion of the Company's integrated logistics business in Greater China and ASEAN countries. Hong Kong warehousing business accounted for 2.6% in terms of turnover, contributing 25.6% of the profit of the Company. Profit margin was maintained at 59.5%, while its occupancy was nearly full, with the renewed lease rent within the year growing at a double-digit rate. It is predicted that the business will maintain steady growth. The percentage of turnover of the international freight forwarding business reached 50.8%, with a profit contribution percentage of 18.1%. Though there was a slight decrease in the turnover due to economic imbalances in the eurozone, net profit of the international freight forwarding business still recorded a 7% growth.

Industry Conditions and Prospects:

The third-party logistics market is dependent on the global economic environment and international trade flows. Affected by the economic downturn, third-party logistics business in the European, American and other developed markets is experiencing slow growth, while the Asia-Pacific region witnesses rapid growth with low market penetration rate, so there is great room for future growth.

The new round of domestic measures to stabilize foreign trade growth will provide new support for the development of cross-border e-commerce business. Kerry Logistics plans to grow in tandem with the increasing scope and scale of the e-commerce trade. E-commerce will remain an important growth factor for the Company in the coming years. Additionally, benefiting from the strategy of "One Belt One Road", the Company is expected to achieve new growth in intra-Asian trade, trade between Asia and Europe, as well as trade between Asia and Africa.

Investment Value:

As an integrated third-party logistics enterprise with the ability to manage international transportation and provide value-added warehousing and distribution services, Kerry Logistics will be devoted to growing organically and through selective mergers and acquisitions. In the future, the Company will further expand its market shares in the Great China region and ASEAN countries, and increase its international freight forwarding capabilities through acquisition. Moreover, the Company will expand its cross-border e-commerce business into other cross-border trade pilot cities and zones, so as to provide integrated cross-border logistics for its partners.

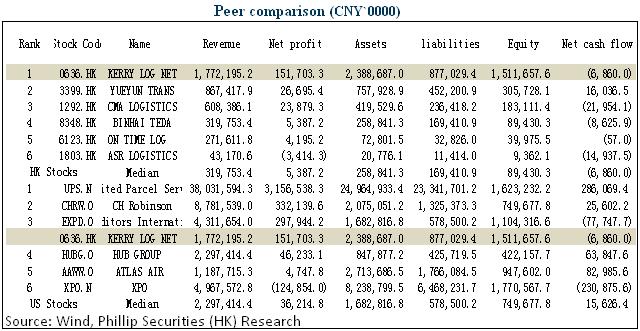

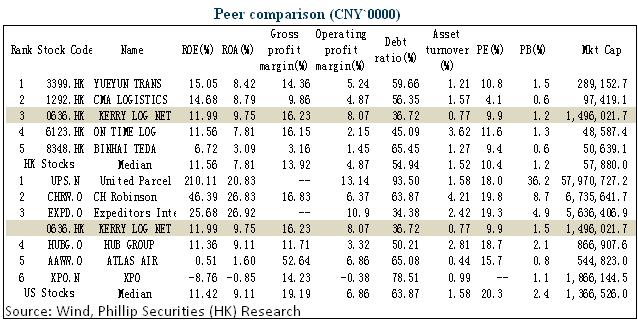

In terms of turnover, net profit and asset scale, the Company ranks first among peer companies listed on the Hong Kong stock market, and average among peer companies of the U.S. stock market. As for profitability, the Company ranks average among peer companies listed on the Hong Kong stock market, and fourth among peer companies listed on the American stock market, with both its ROE and ROA higher than the median value. In addition, the Company has a low assets-to-liabilities ratio and a low total assets turnover ratio, indicating the financial safety and soundness of the company, but the efficiency of its fund use is not high. Currently, the P/E ratio for the Company is 9.9, nearly 50 percent lower than HUB GROUP, and lower than the median value of peer companies listed on the Hong Kong stock market, so the prospect is optimistic. (Closing price as at 16 May2016)

Risk Warnings

The global macro-economy is unstable;

China's economy slows down;

European economy is imbalanced;

Exchange rates of Asian countries fluctuate;

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()