-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Chinasoft International (354.HK) - Major Customer Strategy Supports Continued Growth

Thursday, March 17, 2016  13333

13333

Chinasoft International(354)

| Recommendation | Buy |

| Price on Recommendation Date | $2.640 |

| Target Price | $3.650 |

Weekly Special - 3306 JNBY Design Limited

Major Customer Strategy Supports Continued Growth

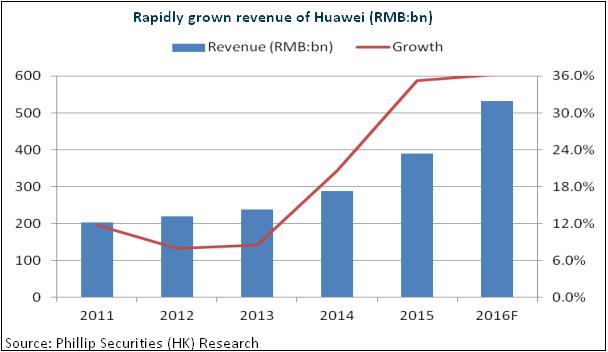

The top five customers of Chinasoft International include Huawei, Microsoft, Tencent, HSBC and Bank of Communications, contributing to around 40% of total revenues of the Company. We expect the Company will maintain a continued growth of about 20% by virtue of business expansion of major customers and Chinasoft's larger share among them. To be specific, the Company, thanks to its status of the largest outsourcing service provider, successfully issued 3.97% strategic shares to Huawei. Such a closer association is expected to help it obtain more outsourcing business share from Huawei, increasing from 40% in 2014 to 50% in 2015. Furthermore, Huawei increased the average remuneration of outsourcing labour from Chinasoft International by 10% in 2015, and accelerated the repayment of the accounts payable to the Company, showcasing the Company is highly recognized by Huawei.

In 2015, Huawei maintained a rapid growth, with its revenues skyrocketing 35.3% to US$60 billion. In accordance with the guidelines, its revenues will soar by 36.3% to US$80 billion in 2016. We believe that Chinasoft International will significantly benefit from the growth and that its ability to serve large customers is also expected to enhance its bargaining power, thereby improving its profitability. Meanwhile, the Company is also projected to expand to more industries (such as cloud services and Industrial 4.0) and more overseas markets (such as India) by virtue of global enterprise customer resources of Huawei.

JointForce Platform Rapidly Expands

The Company's JointForce Commerce Platform has been officially put into operation since June 2015, and the platform targets at IT services Taobao. As of the end of January 2016, the registered engineers of the platform reached 80,000, equivalent to three times the number of employees. Moreover, the total turnover from the platform is estimated to have exceeded RMB100 million in 2015, highlighting the rapid expansion of the platform.

Overall, the platform adopts cloud + crowd-sourcing model to achieve interconnection between related industries and to help integrate resources and boost efficiency. In the future, the Company's revenues resulting from the platform will constantly increase with the gradual improvement in functions and efficient marketing of the platform in the future. Further, the platform's business is characterized by high gross profit margin, which is hoped to enhance the Company's earning capabilities.

Institutional Investors Provides High Stock Margin of Safety

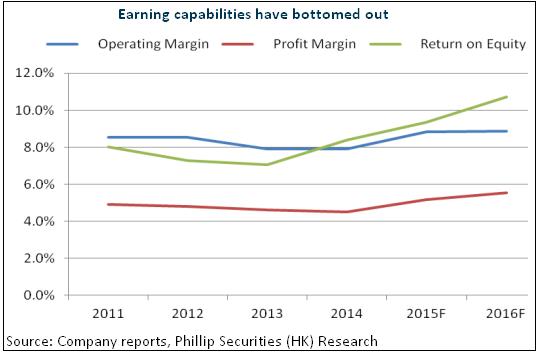

The fact that the Company has won more market shares of large customers reflects that its competitive edge in the domestic IT services is constantly improved, so we believe the Company will continuously benefit from the informatization of China, localization of IT, expanded off-shore IT outsourcing market, cloud computing in Mainland and other emerging businesses. Additionally, the improvement in the bargaining power and the efficiency of the platform will also enhance the Company's profitability, so its rapid performance growth is expectable.

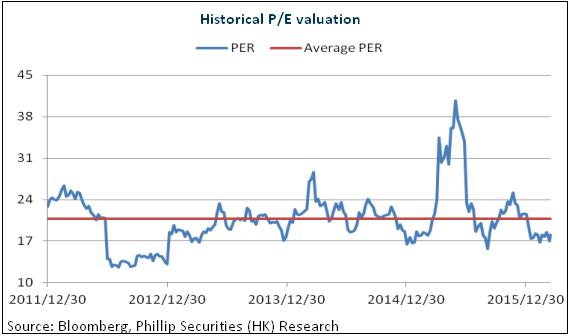

Moreover, the Company is constantly recognized by large institutional investors. In the first half of 2015, majority stake was undertaken at HK$3.68 to 3.93. In the second half of 2015, Huawei held strategic equity in the Company at HK$2.8. Recently, the Company successfully issued convertible notes worth US$70 million and due in 2019 to investors including Huarong International and Energetic Unity. The convertible new shares accounted for 7.8% of the enlarged share capital. The raised funds will improve the financial status, and what is more, the conversion price of HK$3 further demonstrates the market recognition of the Company. We grant the Company a valuation corresponding to 22x EPS in e2015, with a target price of HKD3.65, and a rating of “Buy”. (Closing price as at 15 Mar 2016)

Risks

Intensified market competition drags down profitability;

Labor cost increases too quickly;

Operation risk of Joint Force platform and cloud computing.

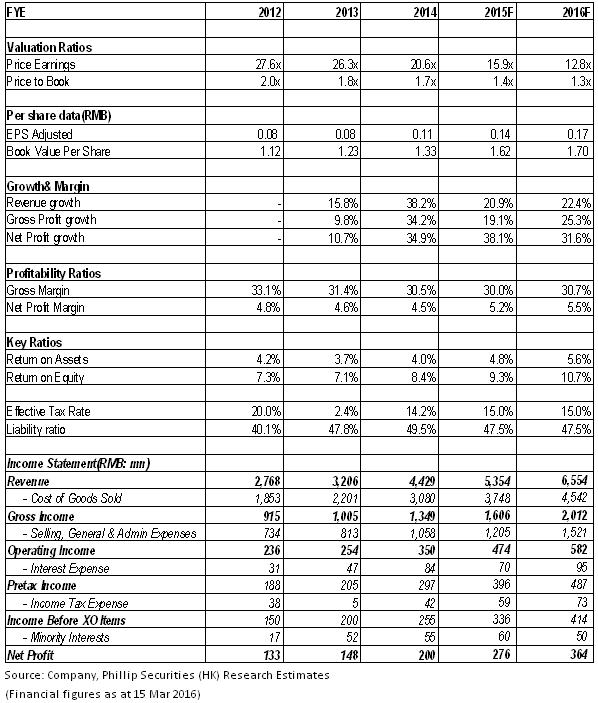

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()