-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

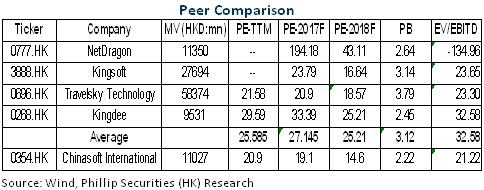

Chinasoft International Ltd (354.HK) - Sales will soon break RMB10 billion target

Monday, April 10, 2017  21059

21059

Chinasoft International Ltd(354)

| Recommendation | Buy |

| Price on Recommendation Date | $4.610 |

| Target Price | $5.800 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Chinasoft International outperformed expectations in 2016, mainly thanks to Huawei's rapidly increased contributions and decreased expense ratios. We believe that the company will continuously benefit from Mainland China's informatization, IT production localization, offshore IT outsourcing market and the strong growth of emerging businesses such as cloud computing, and the major clients` contributions will rise steadily. In addition, the enhancement of technological capacity and its self-owned IP, the improvement of the platform's efficiency and the rise of cloud services` contributions will also boost the company's profitability and enable the rapid growth of its performance. We give the company an estimation of 24x EPS in 2017 and the target price is HK$5.8, with the "Buy" rating maintained. (Closing price as at 6 Apr 2017)

2016 Results Outperformed Expectations

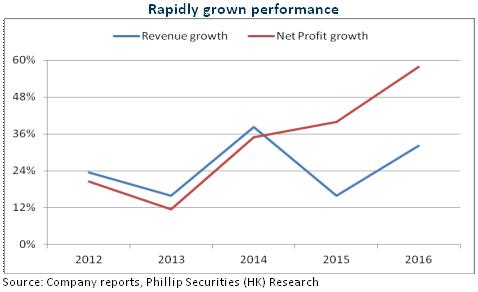

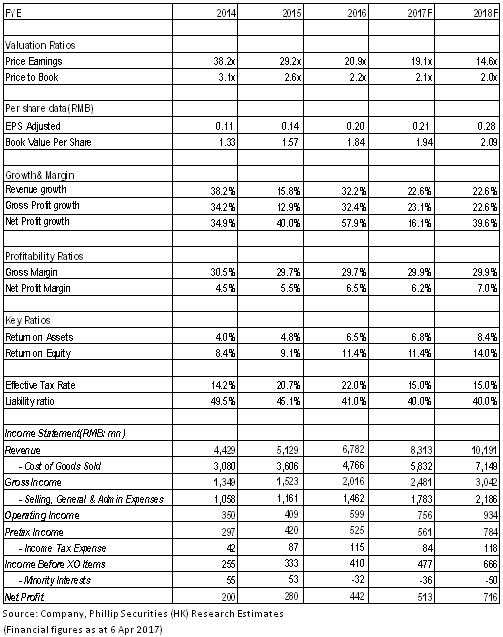

In terms of comprehensive competitiveness, Chinasoft International Ltd is ranked as one of the top ten enterprises which provide software and information technology services in China, with its main business types divided into Technical Professional Services Group (TPG) business and Internet Inquiry Scientific Services Group (IIG) business and covering telecommunication, finance and Internet and other industries. In 2016, the company's revenue increased by 32.3% to RMB6.78 billion. The net profit attributed to the parent company rose by 57.9% to RMB440 million and after adjustment, the net profit attributed to the parent company soared by 96.2% to RMB490 million. Both exceeded market expectations.

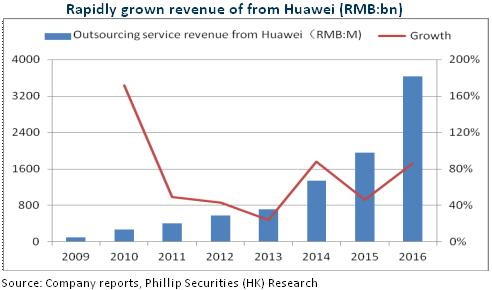

The increase in revenue mainly came from TPG's raised income which rose by 45% to RMB5.48 billion because Huawei's boosted contributions nearly doubled. With regard to profitability, although the gross margin of 29.7% remained the same year over year, the company's TPG business continued to focus on major clients and large industries` offline IT business and enabled continuous decrease in the sales expense ratio and administrative expense ratio which dropped from last year's 3.5% and 12.2% to 3.2% and 11.9% respectively. Furthermore, the company was exempted from partial consideration payment in the acquisition of an American subsidiary company because the conditions of the valuation adjustment mechanism were not met. There was also increase in its subsidiary income and other incomes which went up by 52.7% to RMB43.72 million. All these factors contributed to the rise of the company's profit rate from 8% to 9.7%.

Key Customer Strategy Supports Continued Growth

The company has increasingly focused on certain clients and the business with Huawei retains the main drive of growth. 53.6% of the company's revenue in 2016 was contributed by Huawei, increasing from 38.1% of 2015. We believe that Huawei's business will continuously rise steadily. First of all, the company and Huawei have cooperated to deploy public clouds and big data platforms in over ten cities and to develop regional markets. Next, the company is responsible for overall customization and delivery in many fields, which proves its profound technological strength and helps gain more orders in the future. Additionally, through Huawei's powerful sales access at home and abroad, both companies will make more efforts to develop foreign business and this will introduce new clients to Chinasoft International. It is worth to mention that Huawei's increasing outsourcing demand will bring more bargaining advantages to Chinasoft International.

Furthermore, the company has been designated as HSBC's only strategic partner in China since 2016. It won the bid for the global project and HSBC's contributions to its revenue doubled in the same year, which shows that the company's technology is highly acknowledged. The company has also become Tencent's highest-level access cooperative partner and both of the companies will work together to build the ecological system for enterprises - "Internet+". Considering the rapid increase in research and development with the research and development expense ratio rising from 3.8% to 5.1%, we predict the continuous growth of its major clients` contributions to the revenue, thanks to the enhancement of the technology. Specifically, TPG business will retain the growth of over 20% and therefore, help the company reach the revenue milestone of RMB10 billion.

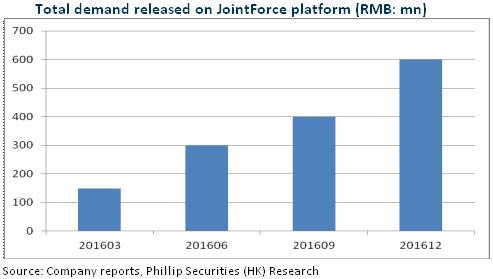

JointForce Platform Upgrades its Profit Model

With JointForce centralized, the company's online business by the end of 2016 had had over 1,000 registered development teams, nearly 3,000 contractor companies, over 130,000 contractor engineers, approximately 200,000 outsourcing companies and over RMB 600 million outsourced projects, with a trend of rapid expansion.

Moreover, the JointForce platform and Huawei Cloud have agreed on mission-level strategic cooperation. Meanwhile, the profit model of the platform has changed from a commission model to a membership model, which will promote user loyalty and all involved parties will boost the vitality of JF's ecological system. Based on these indications, the GMV of JF platform will reach RMB500-600 million in 2017 and the income will exceed RMB200 million.

Risks

Excessive Growth of Labor Costs

The implementation risk on JointForce platform and cloud computing business.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()