-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Anta Sports (2020.HK) - Strong 18H1 Results with FILA Continuing Rapid Growth

Tuesday, October 23, 2018  11173

11173

Anta Sports(2020)

| Recommendation | BUY |

| Price on Recommendation Date | $31.300 |

| Target Price | $47.300 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Anta is a leading sportswear player in PRC. During previous three quarters, Anta delivered strong results and Q4 performance is expected to maintain strong, given more festival promotions and online shopping festival to boost sales. Previously, Anta announced potential acquisition of Amer Sports, a Finnish-based leading sportswear producer, together with a PE fund, which will enrich Anta's product portfolio further. We maintain TP HKD47.3. (Closing price at 19 Oct 2018)

Company Business

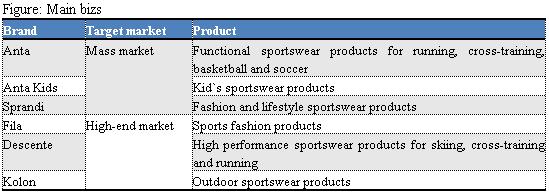

Q3 results beat expectation. In Q3, retail sales of Anta biz recorded mid-teens growth, while sales of other bizs (excluding brands newly joined to the Group) recorded 90%-95% yoy growth. According to Mgt, monthly sales per Anta store increased by 10% yoy to around RMB230k and that of Anta Kids rose from RMB110k to RMB120k. For Fila, due to effective adjustment especially in large stores, monthly sales per store was up by around 20% to RMB600k in Q3. On Descente, the product mix was improved given more thin dress was provided to cater for summer needs, boosting sales.

Proposed acquisition will affect dividend paid out but enrich brand mix. In Sep, Anta issued a takeover bid to a Finnish sporting goods giant, Amer Sports, for a cash stake of EUR40 a share, in conjunction with a private equity fund Fountain Vest. Amer is a Finland-based company engaged in manufacturing, marketing and marketing of sports equipment and footwear. Its products are sold through eight major brands, including Wilson, Salomon, Precor, Atomic, Mavic, Suunto, Arc`teryx and Louisville Slugger. The company conducts international business in more than 30 countries, with US, Europe and Japan as main market areas. In 2017, Amer's net profit fell sharply, mainly because of a one-off divestiture of intangible assets. In 2018, thanks to the recovery of the North American market and the strong growth in Asia Pacific region, operation results clearly recovered. Although the acquisition is still uncertain, but once it succeeds, Anta's brand line will be further extended, and it will be an important step to enter the international sports market. However, management indicated that the next two or three years dividend paid-out may be reduced to ensure acquisition funds required, but it will recover gradually in future.

Q4 results are expected to be good. Second half is usually peak season for retail industry. Moreover, large e-commerce promotion activities and festival promotions are also expected to boost Q4 sales. We highlight that Fila launches a sub-brand Fila Youth and continuously improves its store performance, meanwhile, Descente is expected to deliver better results in winter sports season. We are optimistic about overall Q4 results.

Valuation & Risks

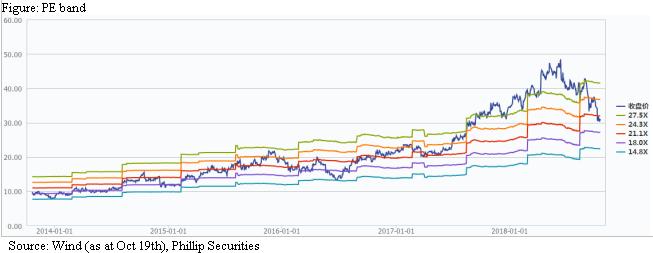

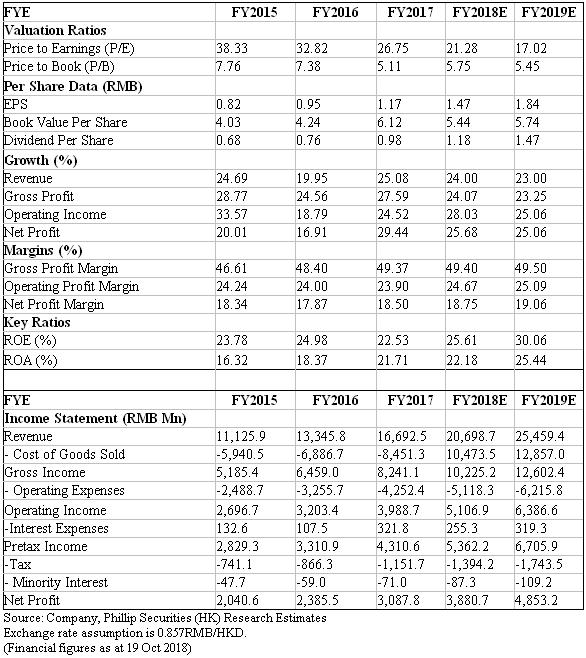

We maintain target price HKD47.3: Projected EPS is RMB1.47/1.84 in 18E/ 19E and target price is maintained as HKD47.3. Risks include: Rising selling and R&D expenses; Sluggish retail market; Inefficiency resulting from so many brands under operation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()