-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

ZTE (763.HK) - Result in 1Q15 Beyond the Expectation

Wednesday, May 6, 2015  9715

9715

ZTE(763)

| Recommendation | Accumulate |

| Price on Recommendation Date | $26.050 |

| Target Price | $30.080 |

Weekly Special - 3306 JNBY Design Limited

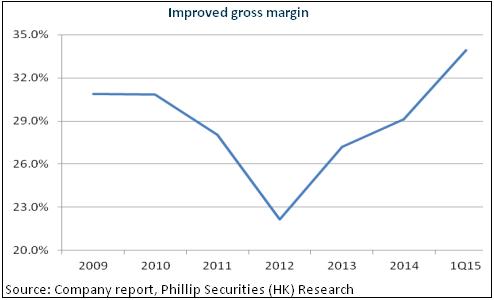

In 1Q15 ZTE recorded a revenue of 20.9 billion RMB (similarly hereinafter), up 10.2% yoy. The net profit was RMB 882 million, up 42% yoy, with EPS of RMB 0.26, surpassing slightly the market expectation. Thanks to the income growth of international videos and network terminals as well as international services, the revenue of the telecommunication software systems, services and other products of the company have increased greatly by 23.38% yoy. Moreover, the gross margin has kept growing to 35.3%, increasing by 1.8 ppts yoy.

The Premier Minister urged to boost the network speed and reduce the network cost as well as expand the construction of information infrastructure, and the Ministry of Industry and Information Technology declared that it would expand the strategic investment of broadband in China in 2015, especially the construction of 4G. We think the support of government policies may push the operators to further improve the capital expenditures. ZTE is competitive in the field of 4G. Not only its essential patents in 4G account for 13%, but also its market share keeps rising. Therefore, in 2015, operators` capital expenditure, especially the increase of 4G investment, will provide guarantee for the performance growth of the company.

Overseas business is an important market of the company and the contribution is expected to improve in future. First of all, the overseas expansion of telecom industry benefits from the national policy of "Belt and Road". Secondly, ZTE's global cooperation and technical strength are expected to strengthen the competitive position. Thirdly, the global telecom equipment giants will be reduced to 4 from 5, the slow competition pattern will help ZTE gain more shares in overseas market. Meanwhile, the possibility of fighting a price war in the future telecoms equipment field will also decrease and the profitability of ZTE is expected to be improved.

The proportion of 4G cellphone will improve continuously, and the products mix will be optimized, so that the ASP and earning capabilities might be improved. In addition, Qualcomm and NDRC agreed on the license event. ZTE owns a strong develop ability on hardware and software, and has a rich patent advantage. It can also charge patent fee from other cellphone suppliers. Therefore, ZTE will also be the major beneficiary of the agreement.

Transformation to New Businesses May Lead to the Reevaluation

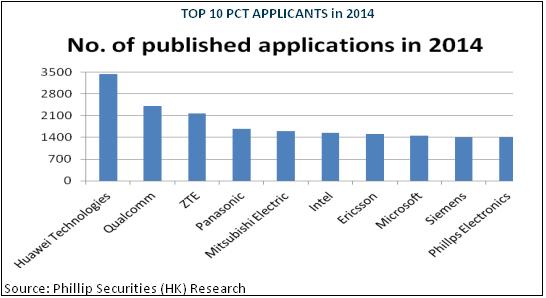

The traditional communication service of ZTE is still in the boom period, and the overseas business expansion is also expected to exceed the expectation thanks to the policy support. Meanwhile, the earning capability will continue to be improved. Moreover, the research and development ability of the company takes the leading position, which will consolidate its advantageous position in the industry competition. As of 2014, it had retained the position in the top three of PCT patent application in the world for five consecutive years. At present, it has above 60,000 global patent applications, among which 17,000 patents have been authorized.

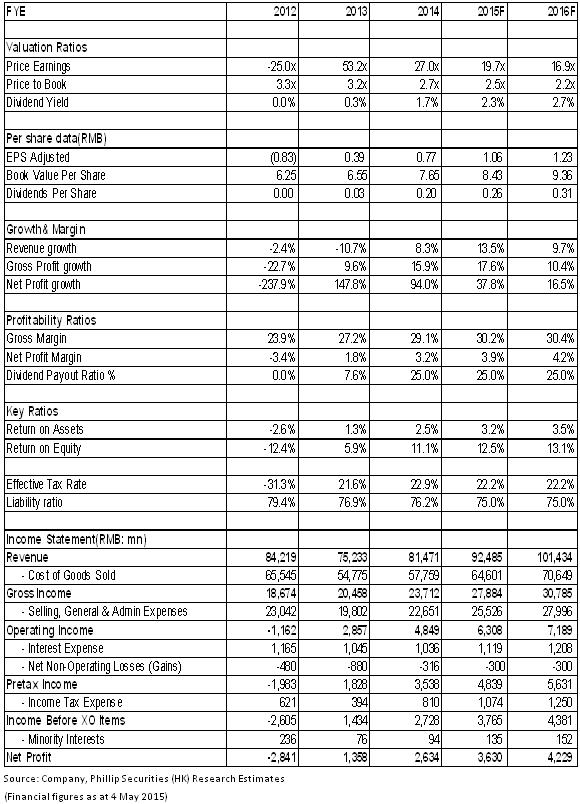

Meanwhile, the company actively lays out emerging fields by utilizing the advantages of technology, including wireless charging, smart city, big data platform, internet finance and so on. Therefore, it will not be a simple equipment supplier any more in future, and then can win the reevaluation of market. We take 22.5 times as the PE ratio valuation of EPS in 2015 and the target price can reach 30.08HKD, with the "Accumulate" rating. (Closing price as at 4 May 2015)

Result in 1Q15 Beyond the Expectation

According to the financial reports released by ZTE recently, in 1Q15 it recorded a revenue of 20.9 billion RMB (similarly hereinafter), up 10.2% yoy. The net profit was RMB 882 million, up 42% yoy, with EPS of RMB 0.26, surpassing slightly the market expectation.

On a closer look, thanks to the income growth of international videos and network terminals as well as international services, the revenue of the telecommunication software systems, services and other products of the company have increased greatly by 23.38% yoy. Moreover, the income growth of the wireless system equipment, wired switching and access systems, routers, exchange boards and other products has driven the revenue from the carriers` network to increase by 8.92% yoy, and the revenue of terminals has grown by 6.97%. What's more, the earning capability of the first two businesses is stronger. With their larger contribution, the gross margin of the company has kept growing to 35.3%, increasing by 1.8 ppts yoy.

Although the financial expenses in 1Q15 have increased greatly by 293% because of the exchange loss, amounting to RMB 600 million, the company has basically hedged against the loss through the investments of foreign exchange derivatives. It is also worth noting that the R&D investment of the company in the first quarter was RMB 2.57 billion, up 30% yoy. This quarter is the single one with the largest investment in history, which further demonstrates the determination of the company to maintain its competitiveness in the communication equipment and its layouts for the era of "Mobile Internet of Everything".

4G Continues to Support the Expansion of the carriers` network business

Recently, the Premier Minister urged to boost the network speed and reduce the network cost as well as expand the construction of information infrastructure, and the Ministry of Industry and Information Technology declared that it would expand the strategic investment of broadband in China in 2015, especially the construction of 4G. We think the support of government policies may push the operators to further improve the capital expenditures. According to the previous disclosure, the CAPEX of the three operators will be RMB 407.5 billion in total in 2015, up 9% yoy.

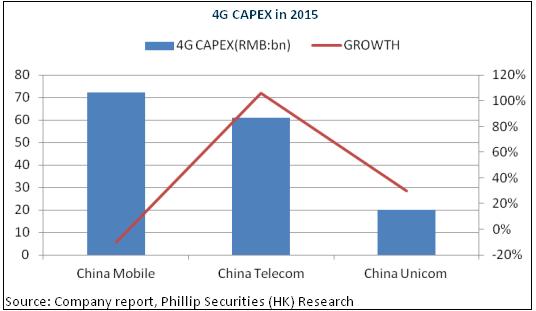

It is particularly worth mentioning that, after the issuance of FDD licenses, the 4G investment of China Telecom and China Unicom may grow substantially, and China Mobile will speed up the implementation of the three phases of constructing LTE. From the view of the full year, 4G investment may exceed RMB 150 billion, and the industry will continue booming, in which the investment of China Mobile decreased by 10% to RMB 72.2 billion, but China Telecom will increase to RMB 61 billion, up 106%, and China Unicom will grow to RMB 20 billion, up 30%.

ZTE is competitive in the field of 4G. Not only its essential patents in 4G account for 13%, but also its market share keeps rising. According to the statistics, the share of ZTE in the third concentrated purchase of China Mobile's TDD-LTE equipment was 38%, rising compared with the second period of 34% and first period of 26%. The share of ZTE in the second concentrated purchase of China Unicom's FDD-LTE equipment was 34%, rising from the first period of 25%, and the two periods of China Telecom's FDD-LTE main equipment procurement were both about 40%, which reflects operators` recognition towards ZTE. Therefore, in 2015, operators` capital expenditure, especially the increase of 4G investment, will provide guarantee for the performance growth of the company.

Overseas Expansion Becomes More Optimistic

Overseas business is an important market of the company, whose revenue accounting for more than 50%, and it is expected to improve in the future. First of all, the overseas expansion of telecom industry benefits from the policy support. The Chinese government has launched a national policy of "Belt and Road", and the prime minister has publicly promoted High-speed Rail, telecommunications and other advantageous industries to "going out".

Secondly, in the overseas markets, ZTE adheres to the strategy of large population and the global mainstream operator, and has established comprehensive cooperative relations with the global mainstream operators. Moreover, ZTE's 4G technology has a leading position in the world, and it has been the first to put forward the concept of Pre5G, in which a number of the key technologies have passed the test and demonstration. Global cooperation and technical strength are expected to strengthen the company's competitive position.

Moreover, recently Nokia has officially announced to acquire its rival Alcatel-Lucent by 15.6 billion euro. The global telecom equipment giants will be reduced to 4 from 5. As a result, the oligopoly is further strengthened. The slow competition pattern will also help ZTE gain more shares in overseas market. Meanwhile, the possibility of fighting a price war in the future telecoms equipment field will also decrease and the profitability of ZTE is expected to be improved.

The Terminals Business Will Be Continuously Improved

After experiencing the previous downturn, the Terminal Service Dept started to operate alone in 2014 and keep the quality strategy, which focuses more on generalizing by publish market channels in the mainland. The series adjustment has brought the terminals business out of downturn. In 2014, the shipment of smartphones reached 48 million, up 20% yoy. Among that, several overseas areas have reported a multiple growth, including Asia-Pacific, Latin America etc. We think that the sales of terminal business have potential to improve continuously.

Moreover, the proportion of 4G cellphone will improve continuously, and the products mix will be optimized, so that the ASP and earning capabilities might be improved. In addition, Qualcomm and NDRC agreed on the license event. ZTE owns a strong develop ability on hardware and software, and has a rich patent advantage. It can also charge patent fee from other cellphone suppliers. Therefore, ZTE will also be the major beneficiary of the agreement.

Catalysts

Large orders will keep coming from overseas;

The bidding progress of FDD-LTE;

Projects of new fields come true step by step.

Risks

Foreign exchange fluctuation will affect the performance of net profit;

New business expansion will cause more cost;

Cellphone sales and ASP are not up to the expectation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()