-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

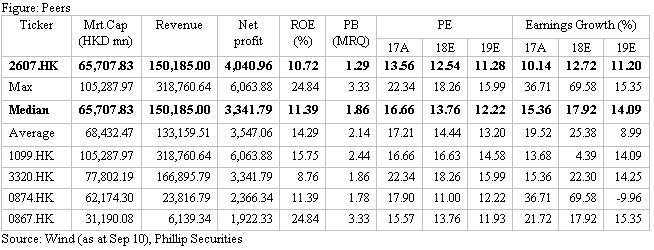

Shanghai Pharma (2607.HK) - Comment on 18H1 Results: Strong Momentum of Manufacturing and Coming Rebound of Distribution

Wednesday, September 12, 2018  9882

9882

Shanghai Pharma(2607)

| Recommendation | Accumulate |

| Price on Recommendation Date | $20.100 |

| Target Price | $24.000 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

The company publishes interim results that the manufacturing business and retail part have maintained rapid growth, and the distribution segment has maintained double-digit growth under the influence of the two-invoice system (TIS). Profitability continued to improve with rising margins. It is expected that distribution business will recover in 18H2. We maintain EPS forecasts and adjust the target price to HK$24.0 to factor into further devaluation of RMB. (Closing price at 10 Sep 2018)

Business Overview

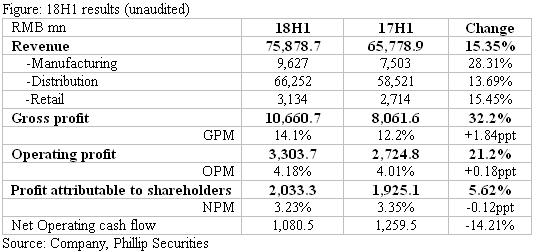

Solid 18H1 results. The company achieved topline of RMB75.87bn (+15.35% yoy) and net profit attributable to shareholders of RMB2.03bn (+5.62% yoy). Shareholding enterprises contributed RMB353mn, down by 9.74% yoy, mainly resulting from channel adjustment under TIS and some drugs experiencing price reduction after entering drug reimbursement lists. Net profit after deducting non-recurring G/L and share profit contributed by invested companies increased by 11.58% yoy. Profit margins steadily increased. Gross margin recorded 14.10%, up by 1.84 percentage points (ppt) , with the manufacturing up by 5.35ppt and the distribution up by 0.62ppt. Excluding management, sales and R & D expenses, OPM rose by 0.17ppt to 4.18%. Operating cash flow fell 14.21% yoy, which was mainly due to the high base of 17H1 according to Mgt, and dose not affect the company's current good operating conditions.

Manufacturing segment. It achieved revenue of RMB9.627bn (+28.31% yoy), GPM of 57.66% (+5.35ppt), R&D expenditure of RMB479mn (+28.29% yoy), accounting for 4.98% of manufacturing revenue. The continued high growth was mainly due to the company's focus on key products and the implementation of "one product, one policy". In 18H1, sales of 60 key products reached RMB5.158bn (+30.19% yoy) and GPM of these was 74.92% (+4.75ppt). With the accomplishment of consistency evaluation of more products, manufacturing segment is expected to continuing growing at a high speed.

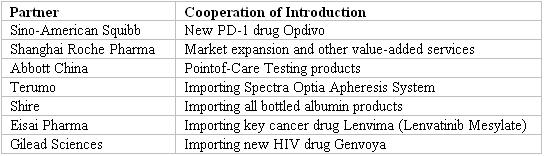

Distribution business. Its revenue reached RMB66.25bn (+13.69% yoy) and GPM was 6.68% (+0.62ppt). The company continued to improve the layout of the national network, given it finishes acquisitions of distribution business in Jiangsu, Shanghai, Liaoning, Guizhou, Sichuan, Anhui, Hainan and other provinces, and promotes the sinking of sale channels to city level from province. It progress the integration of SPH and Cardinal, with a professional team of 63 people established. We see the realization of unified management system, and the preliminary combination in terms of DTP (direct high-value drug delivery) pharmacy business and contract sales. We highlight that distribution business still maintained double-digit growth under the influence of TIS is impressive. In 18H2, the growth of distribution business will accelerate given industry recovery.

Retail segment. Sales reached RMB3.13bn (+15.45% yoy) and GPM of 15.61%, down 0.39ppt yoy. It currently operates 1,981 retail drugstores (including 1,324 self-owned ones), 50 hospital pharmacies and 77 DTP pharmacies. SPH has actively participated in the Shanghai Community Comprehensive Reform Prescription Extension Program, thus it has covered 230 community hospitals and healthcare centers in Shanghai, with a market share of nearly 70%. In 18H1, the company has obtained more than 410,000 prescriptions, with prescription volume increasing by 115.4% yoy. SPH has facilitated the B-round fund of its healthcare e-commerce platform to further expand platform scale, which has processed more than 1.3mn electronic prescriptions and connected with more than 220 hospitals already.

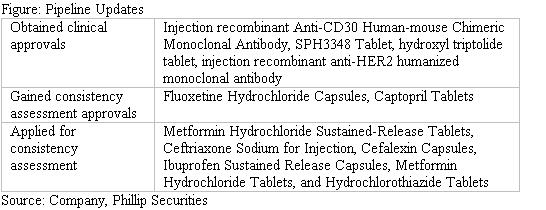

R&D updates. The company increased R&D investment, with an expenditure of RMB479mn (+28.29% yoy), accounting for 4.98% of manufacturing revenue. In 18H1, the company received six clinical approvals of innovative drugs, and promoted the consistency evaluation. It is expected to complete consistency evaluation of around 30 drugs by the end of 2018. At the same time, it focus on strengthening the R&D capability of bio-pharmaceuticals, with formally launching the San Diego R&D Center in US, and carrying out foreign cooperation and equity investment in bio-drugs, so as to enhance the overall innovation capability of bio-medicine.

Valuation and Risks

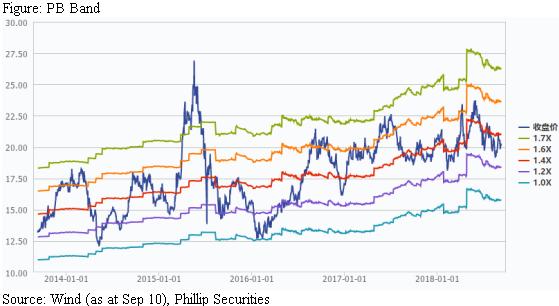

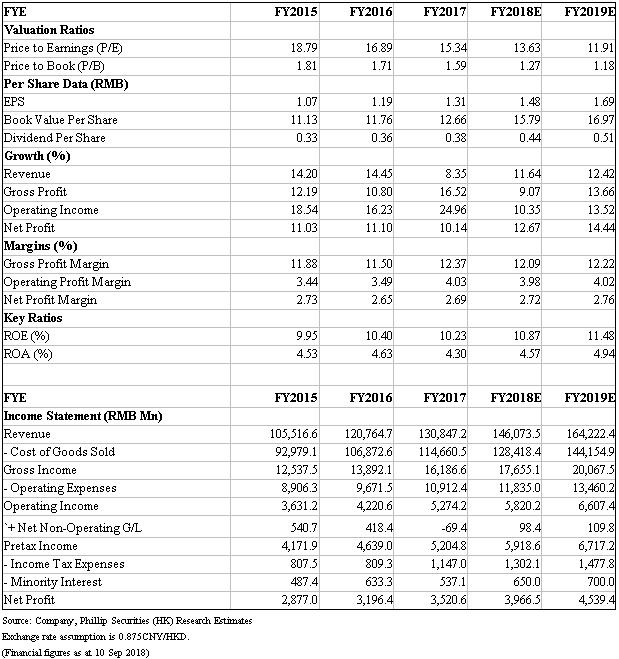

Our valuation model shows TP of HK$24.0. Based on target PE 14.25x and unchanged EPS forecast of RMB1.48, we get TP HK$24.0 (with assumption of Ex rate 0.875 RMB/HK$). Downside risks include: 1) Price reduction after inclusion in NDRL/PDRL; 2) Unfavorable progress in consistency evaluation ; 3) Policy risk.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()