-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

FORGAME HOLDINGS (484.HK) - Actively investing in product transformation

Wednesday, April 30, 2014  7483

7483

FORGAME HOLDINGS(484)

| Recommendation | Buy |

| Price on Recommendation Date | $32.800 |

| Target Price | $44.000 |

Weekly Special - 002050 Sanhua

Company Profile

Forgame was the leading web games companies operated in PRC, it researched, published and operated web and mobile games. On October 3, 2013, the company successfully listed in Hong Kong Stock Exchange Main Board by initial public offering under the ticker symbol (484.hk). At present, most of the revenue was generated from the mainland, while it was also actively expanding its overseas markets.

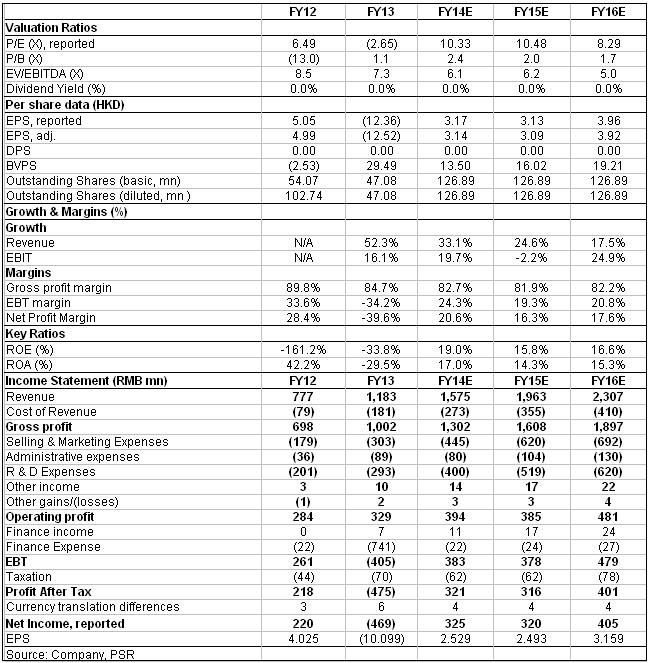

Financial Highlights: Forgame's revenue for FY13 grew by 52.3% yoy to RMB1.183 billion (same below), gross profit increased by 43.6% yoy to $1.002 billion, and operating profit reached $329 million, an increase of 16.1% yoy. However, net profit turned from profit to loss of $469 million. This was due to the company accounted for its $741 million fair value losses of the convertible redeemable preference shares in accordance with International Financial Reporting Standards, this was a one-off loss, and will not produce any expected future costs. According to company reports, after adjusting, the real growth of net profit was 35.5% to $325 million.

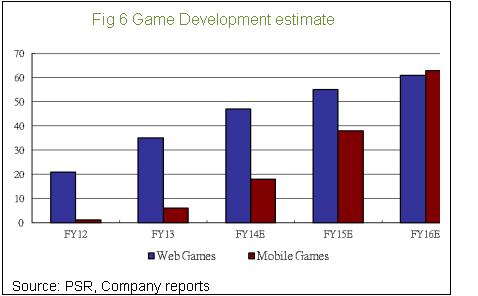

Users and revenue grew rapidly: Products of Forgame were divided into two categories, one was game development and operations. As of 2013 a total of 35 self-developed web games are in operation. It is expected to launch 12 new web games this year. On the other hand, there are 6 self-developed mobile games in operation as of 2013. It is also expected to launch 12 new mobile games this year.

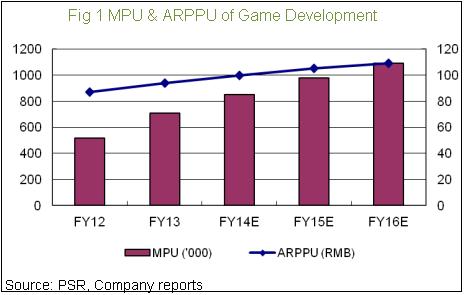

Revenue increased for game development by 47.8% to $799 million in 2013, mainly because the monthly paid users (MPU) grew from 518 thousands to 710 thousands, an increase of 37.1%. At the same time, the average revenue per paying users (ARPPU) increased 8% to $94. This was because in 2013, a number of popular new games launched, including “Conquest of the Universe” (鬥破乾坤) and “Soul Guardian Mobile Version” (凡人修真手游版) and the improved monetization ability. The MPU and ARPPU growth in next three years is expected to slow down, causing the annual revenue growth of game development slowly adjusted to 20% or less.

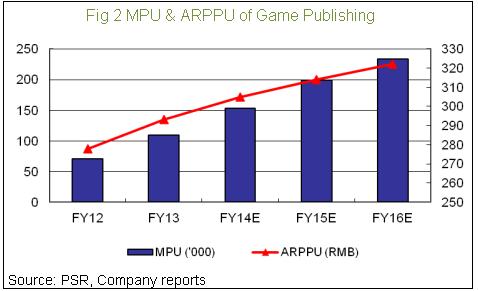

The second category was game publishing. The company launched games through the self-publishing platform 91wan. As of 2013, Forgame published a total of 105 games and attracted 207 million registered players, an increase of 46.8% yoy. Revenues increased 62.6% for game publishing to $384 million. The registered users continued to increase which made the monthly paid users (MPU) to grow from 71 thousands to 109 thousands, an increase of 53.5% yoy. The average revenue per paid users (ARPPU) increased by 5.4% to $293.

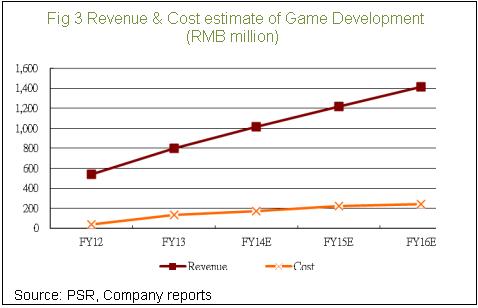

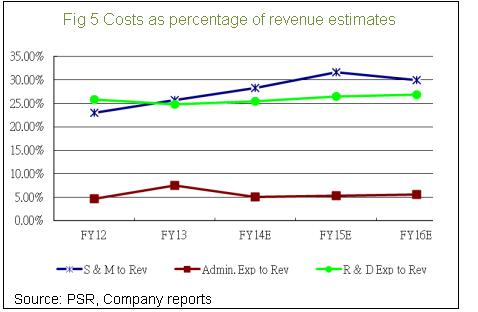

Substantial increase in the cost may be a worry: Due to increased content costs and agency fees, in addition to increase of the number of games, led to an increase of the cost of hardware, game research and development costs increased sharply by 236.1% to $136 million. Cost to income ratio rose from 7.6% to 17%, the proportion is expected to be roughly the same in the future.

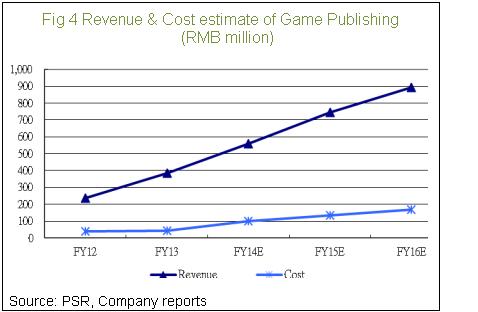

For game publishing, since the cost of technology and salary of operation team increased, costs also rose 16.5% to $45 million. Cost to income ratio fell from 16.5% to 11.7% yoy. However, the new games launching was expected to grow rapidly, leading to increased consumption of hardware, the cost was expected to rebound to previous levels.

Operating expenses also recorded significant increases. Sales and marketing expenses increased by 43.6% to $303 million, primarily due to increased marketing and advertising expenses. The company is expected to increase the advertising costs of the mobile games in the mid term future. Administrative expenses increased by 143.4% to $88.74 million, this was mainly the cost arising from the initial public offering. It is expected the spending will stabilize in 2014. Research and development expenses increased by 46.1% to $293 million, mainly because of increased no. of employee and thus their compensation expenses. It is no longer necessary to recruit a large number of R & D staff this year, spending will be stabilized.

Sufficient cash for development or mergers and acquisitions activities: Forgame successfully listed on the Main Board of Stock Exchange of Hong Kong on October 3, 2013. It issued a total of 2,039 million ordinary shares, the shareholders sold 1,569 shares and 2,906 shares of preferred stocks were fully converted into ordinary shares, resulting in $741 million of fair value losses. The company received net cash of $762 million from listing, together with operating cash flow, net cash as of the end of 2013 reached RMB1.257 billion, which is enough for the company to pay for the acquisition of 21% stake of Magic Feature Inc on March 3, 2014. The acquisition consisted of totaling USD $ 70 million and contingent consideration USD24.2 million, about RMB 438 million and RMB151 million. After the acquisition, the company still holds a large amount of cash for daily operations and looking for potential merger and acquisition target opportunities.

“Tower of Saviors” <神魔之塔>

Through the acquisition of Magic Feature Inc., Forgame could indirectly operate the mobile games “Tower of Saviors”, one of the most popular mobile games in Asia (esp in Hong Kong and Taiwan). Revenue from the game was recognized as investments in associated companies. The income was not included in the expected revenue of the company in the report, since it was difficult to estimate. However, with the visibility of “Tower of Saviors”, and compared to similar games in Japan, We believe the game can bring awareness for the company to enter the mainland mobile game industry as a flagship, thus substantial revenue.

Increase investment in mobile gaming: Company management stated in the 2014 report that they will increase investment in mobile gaming, through 1) co-founded a fund investing primarily in the mobile game contents. 2) reallocated existing web game developers to mobile game development. 3) the acquisition of Magic Feature Inc. 4) to set up a R & D centers in Taiwan, in order to use the technology and art professionals in Taiwan, focus on the development of mobile games. In medium and long term, the company expected to gradually reduce the launching of self-developed web games, so as to reallocate the resources to the development of mobile games.

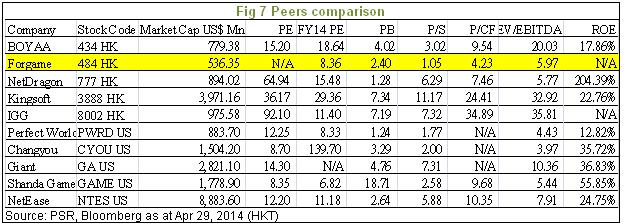

Valuation: Since the beginning of February to March this year, there are strong callback of the share price of IT software, together with the raising of valuation concerns of the U.S. regulators to technology stocks, making the the share price of the sector decline intensively, some individual stocks even dropped by more than half. The stock price of Forgame fell more than 55% from its high. However, based on fundamentals, the company is performing well. After successful transformation, mobile services can also bring considerable growth. Price relative to 2014 forecasted earnings is only 10.48x, we expect a reasonable PE of 14x as the industry average. Therefore, we give the target price of HK $ 44, as the expected PE of14x/14.2x/11.2x relative to 2014/2015/2016, rating as "buy . "

Potential Risk:

Web game revenue growth continues to decline

“Tower of Saviors” failed to bring the expected benefits

Research and development, agency and advertising costs increased more than expected

Financial Status

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()