-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Tongda Group (698.HK) - Technical Advantages Facilitate Market Expansion

Friday, February 5, 2016  15704

15704

Tongda Group(698)

| Recommendation | Buy |

| Price on Recommendation Date | $1.250 |

| Target Price | $1.640 |

Weekly Special - 002050 Sanhua

Technical Advantages Facilitate Market Expansion

Metal casing has become the major driving force for Tongda Group. Currently, few mobile phones produced in China use metal casing, accounting for only 10%. However, the newly released models more often use metal casing and the market will be in a rapid expansion. According to estimates, the proportion of Huawei mobile phones using metal casing will increase from 3% in 2014 to 20% in 2015 and 50% in 2016; that of Xiaomi mobile phones using metal casing will rise from 15% in 2015 and 25% in 2016. Also, mobile phones of other brands using metal casing are expected to soar from around 8 million in 2015 to 46 million in 2016, a five-time increase.

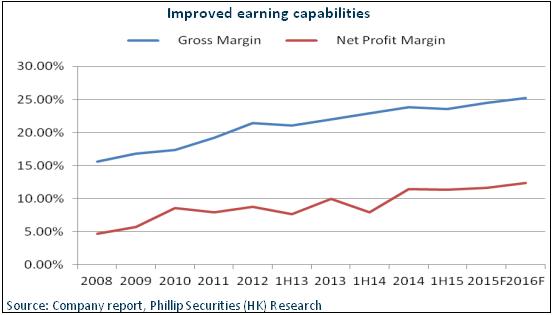

It is worth mentioning that metal casing will break into the market of mobile phones at RMB1,000. Tongda Group's technical advantage of "Composite Die-casting Technology + Nano Molding Technology (NMT) + CNC Processing" can half the time of metal casing production compared with that of competitors. Also, the overall yield of 70-80% also outperforms its peers. Meanwhile, the company's metal casing price around RMB100 is also half. Therefore, the company is more competitive in this market. Furthermore, the company will expand its CNC machine from the current 1700 sets to 2000-2300. As a result, the metal casing business will sustains the company's rapid growth, and its 28-30% gross profit margin will also enhance the profitability.

Brand Users Support Emerging Business Development

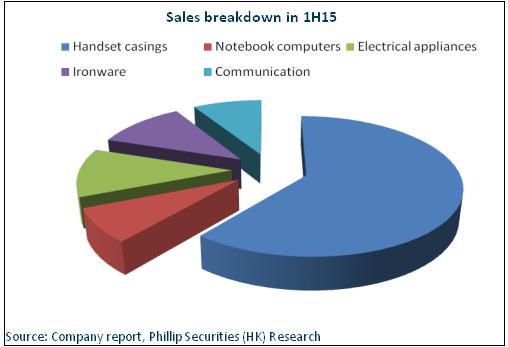

In the last decade, the diversified product mix of handsets, notebook computers and electrical appliances supported the stable growth of the Company's business. Presently, the company has already expanded business to the production of interior components for automobiles, which has been recognized by well-known clients. In addition to the existing clients such as Cisco, Decathlon, Ford and BYD, GM, Geely and Mazda have become the company's new clients since 2015. Despite the present small proportion of automotive interior components business, its market is huge with up to 30% of gross profit margin. We believe the business will become a new driver for the company.

Additionally, Tongda has been developing the rubber compression molding technology which can be used in the waterproof rubber band for smart phones and wearable devices. Moreover, Apple Inc. is likely to become the company's potential client. At present, this field is not fully competitive, and the gross profit margin can reach 30%. Once an agreement is concluded, the company's R&D strength will be further demonstrated, and the brand effect of the company will increase, laying groundwork for its further expansion. In the meantime, the agreement is also expected to contribute to performance growth of 1-3 percentage points.

Increase of Shareholder Equity Holdings that Highlight Confidence in Development

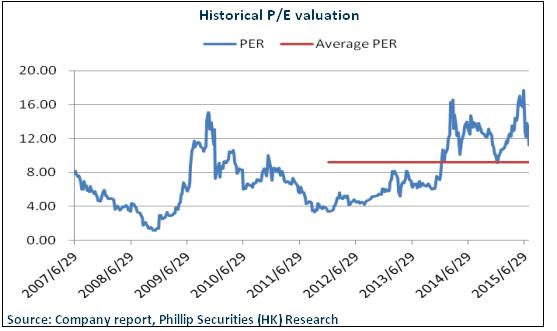

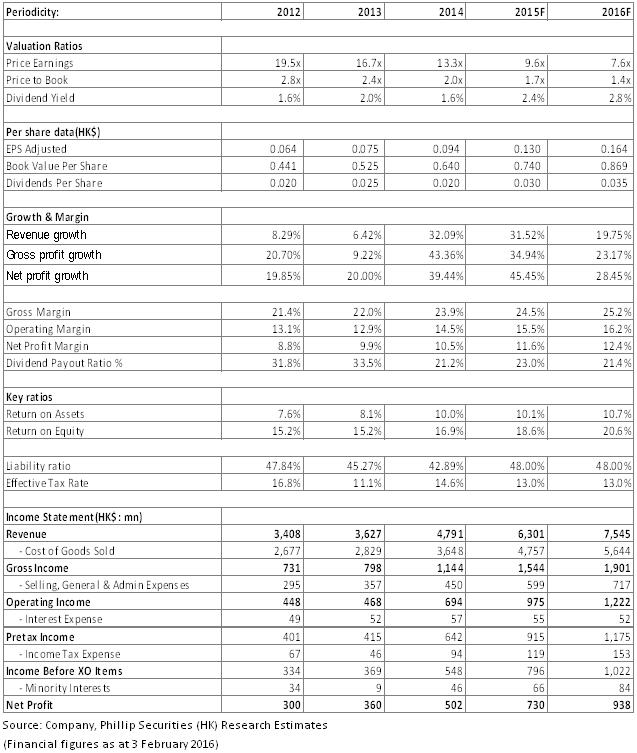

Since the end of last year, Wang Yanan, the actual controller of the company has increased his holdings from 40.92% to 41.4%. And the acquisition price has dropped from the previous HK$1.4 to the current HK$1.25. This demonstrates his confidence in the company's development. We believe that Tongda Group equips itself with the core competitive technologies in all segments that constantly win the recognition of well-known clients. Also, the new businesses such as metal casing will not only support the Company's growth, but will improve its profitability as well. We grant it 10x P/E corresponding to 2016 EPS and the price target is HK$ 1.64, with the "Buy" rating maintained. (Closing price as at 3 Feb 2016)

Risk

Intense competition in the smart phone market that will result in price wars;

The new capacity cannot be put into production as expected.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

E-Check

Login

![]()

![]()

![]()

![]()