-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

SINGYES SOLA (750. HK) - Recovered Growth and Maintained Financial Soundness

Friday, October 14, 2016  31267

31267

SINGYES SOLA(750)

| Recommendation | Buy |

| Price on Recommendation Date | $4.120 |

| Target Price | $5.100 |

Weekly Special - 3306 JNBY Design Limited

Results Returned a Growth Track

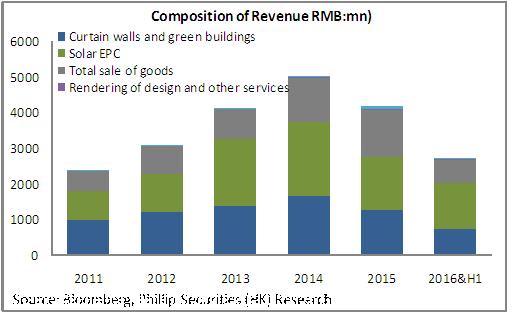

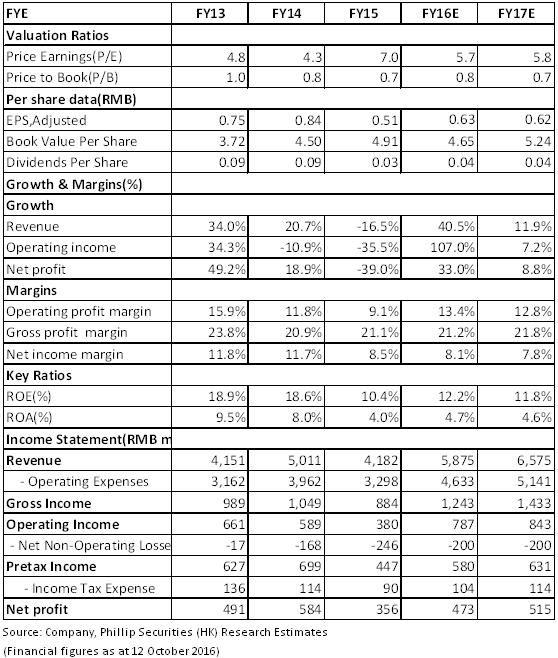

Operation revenue of China Singyes Solar Technologies stood at RMB2.756 billion in H12016 (including RMB37.6 million tariff adjustment), representing a year-on-year increase of 24.8%. Its gross profit was RMB613 million, increasing by 15.2% from last year, and net profit attributable to shareholders amounted to RMB316 million, surging by 41.5% year-on-year. Besides, basic EPS was RMB0.454, jumping by 41.4% over the previous year. The significant result growth during the period was primarily attributable to the strong growth of solar EPC business and curtain wall and green building business.

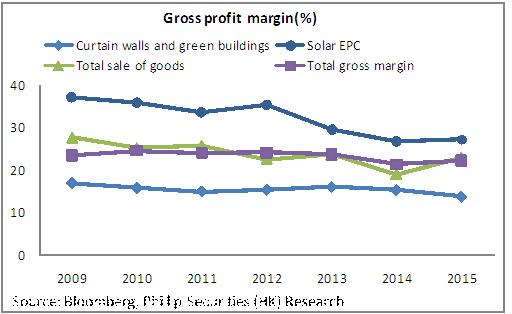

In respect of profitability, gross margin was 22.2%, down by 2 percentage points year-on-year. During the period, expense ratio was 15.15%, down by 1 percentage point over last year. The final net profit margin was 11.97%, increasing by 1.7 percentage points over 2015, because the revenue derived from the sales of 50MW photovoltaic power stations contributed to the improvements in profitability.

Steady Growth in Green Building Business

Revenue from curtain wall and green building business stood at RMB765 million, representing a year-on-year increase of 26.5%, accounting for 27.7% of the total revenue and with gross margin stabilizing at 15.9%. Specifically, increase in revenue from industrial and commercial buildings and from high-end residential buildings was dramatic, thereby offsetting the decline in revenue from the public works business. As a result of gradual recovery of the domestic construction industry and active expansion of overseas business, green building business will become the main growth point of the company's result.

Bright Prospects for Solar EPC Business

Revenue from solar EPC business amounted to RMB1.263 billion, representing a year-on-year increase of 22.2%, accounting for 45.8% of the total revenue and with a gross margin of 26.2%. During the period, 195.5 MW of solar energy power stations was connected to the grid, and 202.4 MW was to be constructed and awaited for grid connection. It is expected that 400 MW is to be completed throughout the year. Against the grim situations of abandoning photovoltaic power stations, curtailment and delay in subsidies in the northwest region in China, the company gradually disposed of its own assets of power stations in the northwest region in China. In this September, the company sold a total of 110 MW photovoltaic power stations in Xinjiang and Gansu at a consideration of HKD860 million. In the future, the development focus of solar energy business will gradually shift to the central and southern region in China with a heavy demand for electricity and without curtailment. Therefore, the future development prospects are positive.

Further Reduction in Liability Ratio

In the first half of 2016, the company maintained financial soundness. The current ratio was 2.04 and the liability/asset ratio was 68.8%, down by 6.5 percentage points from last year's 75.3%. In the coming days, the company will continue to further reduce the liability ratio to the target level of less than 50% by selling some power stations, debt restructuring and other ways.

Valuation and Rating

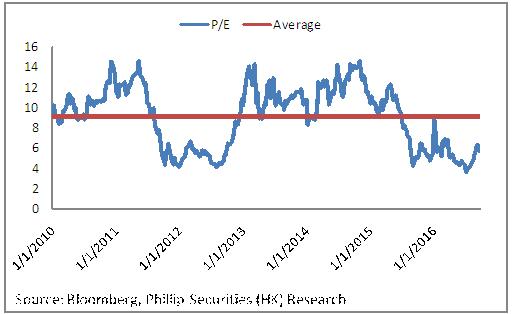

In the first half of 2016, the company recovered result growth, and its financial standing was further improved after the disposal of the power stations in the northwest region in China. Furthermore, driven by favorable policies of new energy and continued increase in electricity demand, sustained growth of company's results is guaranteed. We give the company the target price of HKD 5.10, equivalent to 7.0 X expected price/earnings ratio in 2016. The "Buy" rating is given. (Closing price as at 12 October 2016)

Risk Warnings

Poor prospects for the construction industry;

Progress EPC in business falls short of expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()