-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Huahai Pharmaceutical (600521.CH) - Optimistic Export Prospect of Preparations

Friday, June 16, 2017  18841

18841

Huahai Pharmaceutical(600521)

| Recommendation | BUY |

| Price on Recommendation Date | $19.400 |

| Target Price | $24.200 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

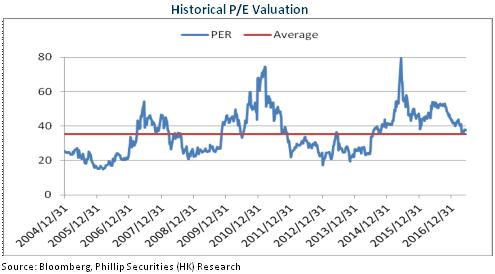

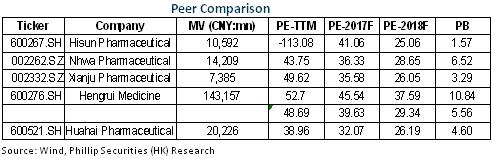

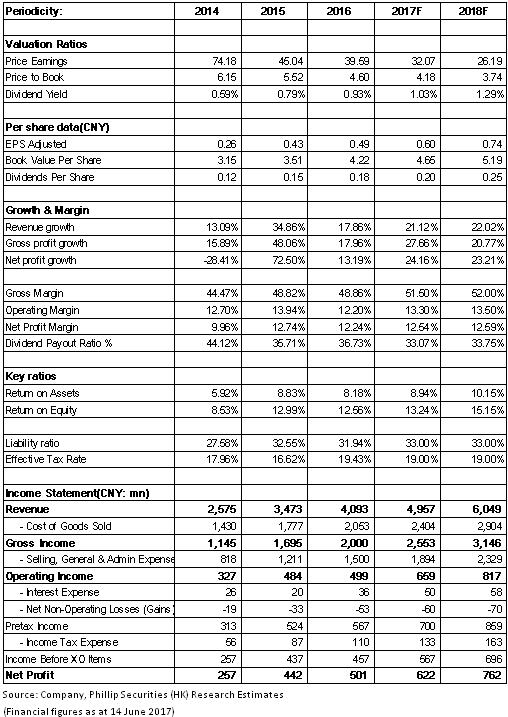

Huahai Pharmaceutical is the leading export company of domestic preparations. Since 2016, although revenue growth has met expectations, the expansion of sales channels and others increased the costs so that the company's earnings performance was below expectations. However, due to the obvious strength of the company's preparations in export, the stepping up efforts in overseas mergers and acquisitions, and a large reserve of the ANDA variety, the future prospects of the export of the preparation is still optimistic, with a tendency of faster growth in the contribution. At the same time, by virtue of "Deemed as passing the consistency evaluation" and other policy advantages, the products launched by the company in Europe and America are expected to switch to the domestic market and have priority in assessment. After the approval, it will also improve the company performance. We give an estimation of 40x EPS in 2017 and a target price of RMB24.2, with the "Buy" rating initially. (Closing price as at 14 June 2017)

Performance Below Expectation

Huahai Pharmaceutical reported a revenue of RMB4.09 billion in 2016, up 16.9% yoy. Net profit excluding non-recurring items was RMB450 million, up 10% yoy, and the earnings per share was RMB0.49. The revenue was RMB1.13 billion in 1Q17, up 16.7%. Net profit excluding non-recurring items was RMB110 million, down 7.1%, and the earnings per share was RMB0.13. Overall, the company's revenue was in line with expectations, but the profit performance was below expectations.

From the perspective of products, the company recorded RMB1.88 billion of API and intermediates, among which Pril API reported an income of RMB370 million, up 17.9% yoy in 2016, and the gross margin increased by 3.2 percentage points to 40.5%, while Sartan API achieved an income of RMB890 million, up 11.3% yoy, and the gross margin increased by 2.2 percentage points to 47.4%. The preparation business reported an income of RMB1.96 billion, up 22.4% yoy, but the gross margin decreased by 3.4percentage points yoy to 56.7%, which was mainly caused by the decline in the price of foreign products, and the increase in the costs as a result of the launch of new production lines.

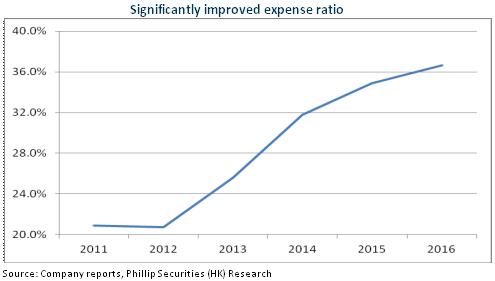

In addition, the dramatic increase in the company's expense ratio affected its performance. In 2016, Huahai US Inc., a subsidiary of the company, suffered a loss of RMB157 million, an increase of nearly RMB120 million comparing to that in 2015, as a result of the increase in R & D costs and litigation costs. Moreover, as the company made more efforts on the marketing and promotion of preparation products, the company's marketing expense ratio in 2016 also increased by 2.2 percentage points to 15%. In 1Q17, although the company's gross margin increased by 5.2 percentage points to 51%, the company's marketing expense ratio also increased by 8.3 percentage points to 18.9%.

Duloxetine was Approved in USA to Enrich Product Line

In May 2017, the Abbreviated New Drug Application (ANDA) filed by the company for duloxetine was approved. The product is administered as an enteric-coated capsule, and specifications are 20 mg, 30 mg and 60 mg. The product is mainly used for the treatment of depression and generalized anxiety. As we can see, the company's product line for mental illnesses will be more abundant, and preparations will also be updated to high-end.

In general, the company's products were concentrated in high blood pressure previously, with only risperidone, paroxetine, lamotrigine etc. for mental illnesses. This time, Duloxetine has been approved to further enrich the product line for mental illnesses, and it is expected to form a product cluster to help brand and sales development in the future. Moreover, ANDA launched by Huahai previously were ordinary tablets or controlled release formulations, and the duloxetine capsule is a breakthrough in capsules this time. At the same time, its market scale is approx. USD2 billion in the U.S., but only about RMB350 million in China, so the market is vast. Moreover, the market structure of the drug is sound, but 70% of the market share was controlled by original research manufacturers. Generic drug manufacturers such as Zhongxi Pharmaceutical, Nhwa Pharmaceutical occupies a low market share, and the specification was only 20mg. Thanks to the approval of Huahai's ANDA, the specifications become more. Additionally, the products are in line with "Priority of Review and Approval", "Deemed as passing the Consistency Evaluation" and other standards. Consequently, it is expected to accelerate to step into the market and seize the market through high performance ratio and policy advantages, so as to achieve import substitution ultimately.

Export Prospect of Preparations is Optimistic

Huahai Pharmaceutical preparations export business is in a leading position in China, and the income from export business contributes to 2/3 of the company's revenue currently. The company has built a mature high-tech solid formulations generic drug research and development, declaration and registration platform. The sales platforms also cover more than 95% of the US sales network, so we believe that the leading position of its preparations export will be consolidated.

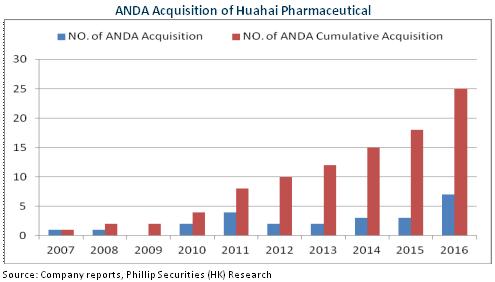

At present, the company has 29 products that have obtained an ANDA number, of which 22 products are selling in the United States. Furthermore, seven products such as Ramo triazine, ropini Nile, donepezil are in a leading position in the market. At the same time, the company has 12 products whose launch has been approved in 24 EU countries, which has proved its excellent preparation strength. It is also worth mentioning that approval of the company's ANDA has shown signs of speeding up. The variety under application reaches as high as 40. Patent challenging has also become normalized. We expect the contribution of preparation export to the company's revenue will continue to improve.

In addition, the company is intensifying its efforts in application for approval of launch in the domestic market and consistency approval for its products sold in the US and European markets. Valsartan entered the priority review in December, 2016 thanks to its overseas sales. This product is the first oral drug to be submitted for overseas-to-domestic application, and the Center for Drug Evaluation is currently exploring applicable legislation. After its launch in the future, more products may follow suit and be launched in the domestic market.

Risks

The application of domestic and foreign preparations registration are below expectations;

Fluctuations in API prices exceed expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()