-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

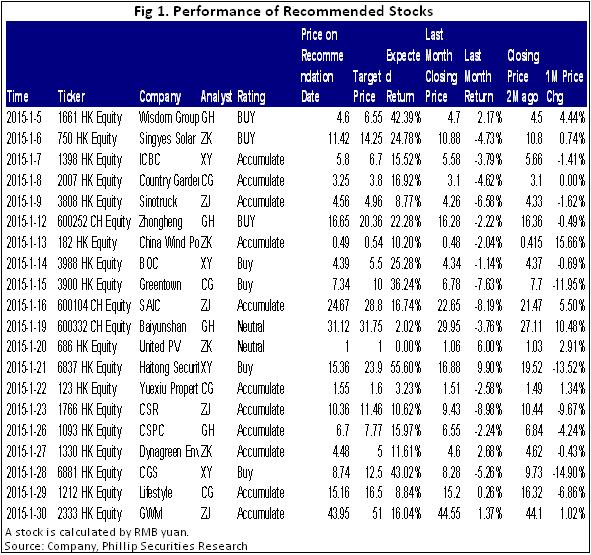

Report Review of Jan. 2015

Monday, February 2, 2015  14537

14537

Report Review of Jan. 2015

Weekly Special - 3306 JNBY Design Limited

Sectors:

Mainland financial, Utilities (Xingyu Chen), Mainland Telecom (Fanguohe),Mainland property, Oil and gas service (Chengeng), Air, Automobiles, Infrastructure (ZhangJing), New energy & Environmental Goods (Zhang Kun)

Mainland Financial (Xingyu Chen)

The market was adjusted continually in Jan 2015, and HSI trended to go up from 23,800 at the beginning of this month to 24,600 currently, increased by 3% approximately. Due to the beginning of a new year, investors` investment strategy was still conservative, and financial sectors such as the banking and insurance sectors were popular. According to the banks` performance, share prices were adjusted due to the strong growth by the end of last year, therefore they were weaker than that of HIS.

As at the end of 29th Jan, domestic listed banks` share prices decreased by 5.5% in average compared with the beginning of Jan, only CQB recorded the positive growth, and HSI increased by 3.1% during the same period of time, mainly due to the sharp increase of prices of domestic insurers. Stated-owned banks had the better performance, BOC and ICBC's prices dropped 1.8% and 2.9% respectively, but BoCom's share price decreased largely by 12.1%. Most of joint-stock commercial banks` share prices declined, of which CMB's price recorded the largest decrease as 13.2%, and both CITIC Bank and CMBC's prices also dropped over 8%.

We believe the adjustment of this month is mainly caused by a technical adjustment after the sharp growth of prices last year. According to the banks` operating performances, they maintain at the stable level, therefore the banks` performance meet our expectation, and we continue to hold the cautiously optimistic view on the banks` prices in future. Maintain the banking sector on Buy rating.

Mainland Telecom (Fan guohe)

The 4G market continues to be popular. China Mobile increased 18.83 million new 4G users in December 2014, which had an obvious growth trend comparing with previous months. The number of 4G users has a yearly net increase of 90 million. The rapid increase will create an opportunity for flow operation. China Unicom focuses on the vehicular networking business. Currently it has provided services for 3 million vehicles. China Telecom has issued Tianyi Tencent Video Phone, the biggest highlight of which is free of data fee. Overall, the flow operation will be the trend of the market, and the competition in the industry is predicted to increase.

The FDD license has not been issued in 2014. But considering of the balance of the competition pattern in the industry, we expect the license will be issued in early 2015, which may drive a new round of opportunities for investment of the industry.

Under the background of information safety, localization of telecommunication equipment will become the trend. Companies such as ZTE are predicted to have continuously growing market shares, and their performances will maintain high growth. In addition, owing to the rapid propulsion of the construction of 4G networks, the network optimization demand will start. So it is suggested to pay close attention to the leading manufacturers such as Comba Telecom. Meanwhile, benefiting from the application of new technologies and the extension of overseas applications of mobile terminals, we also look upon TCL Communication, etc. favourably.

Mainland Property & Oil/Gas service (Chen geng)

In January, 2015, I wrote four research reports on Country Garden, Greentown, Yuexiu Property and Lifestyle, which got success by unique operation model. We recommend “Lifestyle”. Recently, some changes in the fundamental aspects of Lifestyle mainly include important shareholder turnover, normal operation of SOGO Causeway Bay store in the mid-late November, as well as SOGO TST store after reopening. We think that the Lifestyle is returning to normal operation from being forced to change the address of Causeway Bay store and the "Occupying the Central" event of Hong Kong.In our opinion, Lifestyle's brand value and management team deserve a better valuation. In the future, with a better atmosphere of commercial retail in Hong Kong and Mainland China, we believe that the valuation of Lifestyle is expected to recover. Lifestyle is allowed to "Accumulate" ratings with a 12-month target price of 16.50 HKD, equivalent to 12 times of P/E in 2015.

Automobile & Air (ZhangJing)

This month we updated 4 equity reports including SAIC (600104.CH), GreatWall Motor (2333.HK), CSR (1766.HK) and Sinotruk (3808.HK). We prefer GreatWall Motor and SAIC with the more attractive future.

As for GreatWall Motor, robust growth of profitability in the fourth quarter driven by the new model effect indicated that GreatWall Motor's strategy of “focusing on SUV” had a successful start. Looking into 2015, under the expectation that the demand for H6 remains high, the newly launched H2/H1/H9 continues to increase and the upcoming new SUV model H8/H7/CoupeC and H2/H6 AT version, the ASP and single vehicle profitability of the comapny are expected to enter a new level. We accordingly revised the target price to 51, respectively 15.2/10.6/8.7x P/E and 3.7/2.9/2.4x P/B for 2014/2015/2016. We reiterate "Accumulate" rating. The latter SAIC has extremely appealing dividend payout rate and stable growth ratio, plus SOE reform expectation.

New energy & Environmental protection (ZhangKun)

We update four reports this month, they are Singyes Solar(759.HK), China Wind Power(182.HK), United PV(686.HK) and Dynagreen Env(1330.HK). We recommend Singyes Solar, The company has signed the strategic cooperation agreement with GCL New Energy that the scale of the cooperation projects in 2015 will not be less than 500MW, which are mainly the distributed power stations. The company has also won the bidding for the construction of a public utilities project in Hong Kong, with the contract amount of 200 million HKD, which will be started in February, 2015. In addition, there are a large number of orders held in the company's hands currently; the company disclosed that it had had the photovoltaic EPC orders for 350MW by October 17, 2014, of which around 50% are the distributed photovoltaic projects. Accordingly, we estimate that the company's income in 2015 will increase substantially, in addition, new policies may be published in this year and ensure the profit.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()