-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

DONGJIANG ENV (895.HK) - Focuses on its Main Business of Hazardous Waste Treatment and Shows a Steady Improvement in Profitability

Monday, May 15, 2017  18214

18214

DONGJIANG ENV(895)

| Recommendation | Buy |

| Price on Recommendation Date | $12.160 |

| Target Price | $14.800 |

Weekly Special - 3306 JNBY Design Limited

Focusing on the main business of hazardous waste treatment and showing a steady improvement in profitability

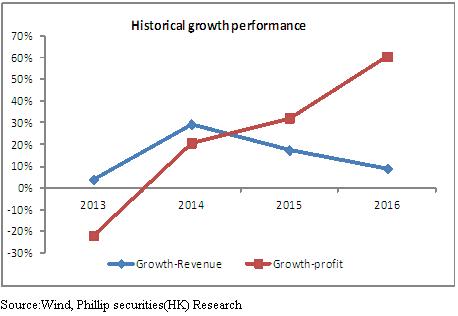

In 2016, Dongjiang Environmental Co., Ltd. recorded an operating revenue of RMB2.62 billion, representing a modest increase of 8.9% YoY which was mainly due to the influence of active adjustment of business structures. At the same time, Dongjiang achieved net profits attributable to shareholders of RMB534 million, up by 60.53% YoY, and net profits attributable to the parent company after deduction of non-recurring profit and loss of RMB379 million, up by 27.4% YoY.

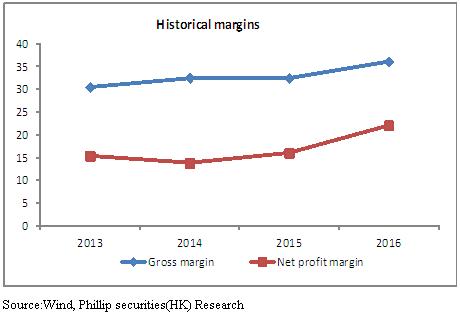

In terms of profitability, thanks to the steady growth of business, the strict control of cost, and the income from investment, the company's gross profit margin was 36.12%, up by 3.7% YoY. Its net profit margin was 22.05%, up by 6.0% YoY. The strategy of focusing on main business and expansion started to pay off. The company predicted that in H1 of 2017, the growth of profits would be between 20% and 40%.

In terms of business structure, its business of harmless treatment of industrial waste, with the highest gross margin, was the main income source of the company. This business recorded a revenue of RMB843 million, up by 43.65% YoY, accounting for 32.3% in the total revenue of the company. The gross margin of this business was 49.98%, down by 1.59% YoY. The business of recycling treatment to industrial waste recorded a revenue of RMB791 million, up by 2.34% YoY, accounting for 30.23% in the total revenue of the company. The gross margin of this business was 32.92%, up by 2.49% YoY. The revenue from the business of environmental engineering and service and from the business of municipal waste treatment increased by 22.7% YoY and 12.2% YoY, respectively. In order to better focus on the main business of industrial waste treatment, the company has sold out part of its household appliances dismantling assets, which dragged down the revenue from the business of dismantling electronic waste to RMB221 million, down by 44% YoY. However, we hold that selling out part of the business of dismantling electronic waste, which showed a low gross margin, would help the company gather strength to accelerate expansion of the business of hazardous waste treatment and improve the competitiveness and profitability of the business.

Leading in the capacity of treating hazardous waste, improving the national layout of the company

In the period, capacity release of the company has achieved remarkable results. A total number of 66,900 ton of projects have been put into operation and 135,000 tons of projects into the trial operation. The PPP project in Quanzhou city is expected to be completed by the end of 2017. Meanwhile, nearly 200,000 ton of projects of Dongjiang in Weifang city have gained the EIA approval. The company's ability to undertake environmental protection projects has improved greatly. In the period, the number of new projects of the company is up to 14, with a total investment of RMB220 million. In terms of business layout, the company consolidated the business in the Guangdong-based Pearl River Delta region, at the same time, strived to develop the business in the Jiangsu and Zhejiang-based East China region and marched into the market of Shangdong and Hehei to build up the Bohai layout.

By 2016, the company has the capacity of treating 1.5 million ton of hazardous waste, with a 50% ratio of harmless treatment capacity, owns the treatment qualification of 44 types of hazardous waste in 46 types of hazardous waste in national catalogue and retaining its leading position in hazardous waste treatment industry. By 2020, the total capacity of the company is expected to exceed 3.5 million ton and the capacity of harmless treatment will account for more than 60% and up to 2.1 million ton. At present, there exists a serious mismatch between the production of hazardous waste and its treatment capacity in our country. In 2015, the national production of hazardous waste was 42.2 million ton while the treatment capacity was 35.7 million ton. Treatment capacity gap in the market is huge. The degree of industry concentration is low. At the same time, enterprises with a full qualification of hazardous waste treatment are also extremely rare. In addition, it is estimated that during the Thirteenth Five-Year plan period, the compound growth rate of the demand of hazardous waste treatment will be more than 15%. Comparing to 2015, the room for market growth of hazardous waste treatment business will double. Therefore, in the following five years, the industry of hazardous waste treatment will continue to maintain a high degree of prosperity. Meanwhile, the company has significant advantages in qualification. Thanks to the background of state-owned enterprise, the company's leading position in waste treatment industry will continue to gain momentum. In the future, the company will be benefit greatly from strict environmental regulation, enhancement of industry concentration and expansion of market so that the revenue of the company will continue a rapid increase.

Benefits from the investment of Guangsheng have shown and the increase of new projects will accelerate.

Thanks to the support of Guangsheng, the company successfully issued green corporate bonds in 2016, with the initial size of RMB600 million and an interest of 4.9%. The company became the first listed company who issued green bonds in Shenzhen Stock Exchange. At the same time, in March 2017, the company issued successfully PPP asset-backed securities with a size of RMB320 million. PPP assets securitization landing will optimize the financial structure of the company and reduce the overall cost of financing. In addition, because the company is the focus of Guangsheng on the development of environmentally friendly platform, its financial strength will be enhanced greatly. The company will undertake more and more environmental PPP projects to consolidate and enhance its overall competitiveness further.

Valuation and rating

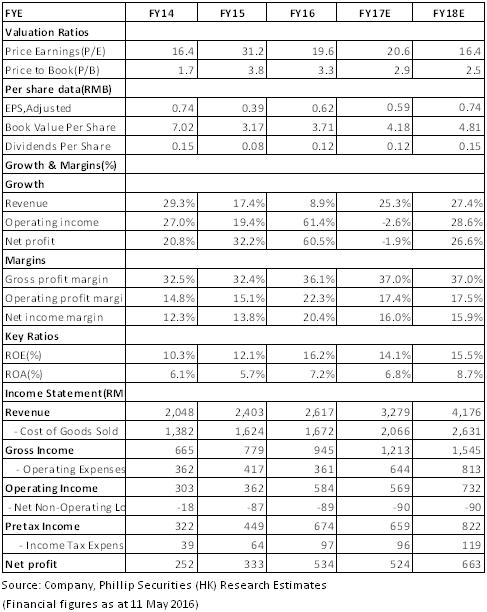

We estimate, from 2017 to 2018 the revenue will reach 3279/4176, the net profit will reach 524/663 respectively, with EPS of RMB0.59 and RMB0.74, respectively. We give a target price of HK$14.8 and the "Buy" rating is maintained. (Closing price as at 11 May 2017)

Risk warnings

The number of projects which has put into operation is less than expected;

Non - ferrous metal prices continue to fall.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()