-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

HUADIAN FUXIN (816.HK) - Profitability Improvement Driven by Wind Power and Hydropower Segments

Friday, October 7, 2016  30299

30299

HUADIAN FUXIN(816)

| Recommendation | Buy |

| Price on Recommendation Date | $1.840 |

| Target Price | $2.510 |

Weekly Special - 2333 Great Wall Motor

Steady Growth of Revenue in Line with Expectations

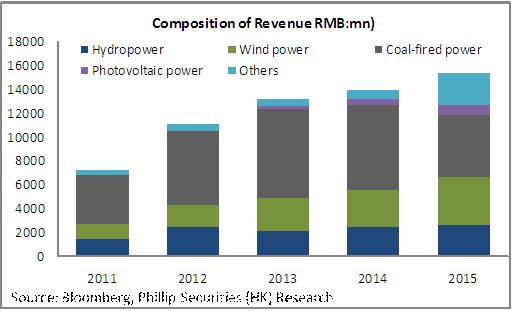

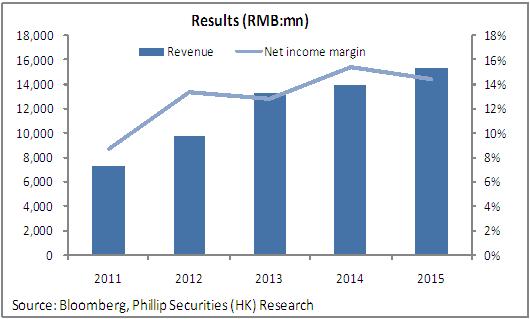

During the first half of 2016, Huadian Fuxin (816.HK) recorded revenue of RMB8.182 billion, representing a year-on-year increase of 8.7% primarily due to the year-on-year increase in electricity sales by 16.9%. Particularly, the wind power and hydropower businesses had outstanding performance. The revenue from the wind power business was increased to RMB2.82 billion with the annual growth rate of 39.5% and the annual growth rate of electricity sales of 43.5% while the revenue from the hydropower business was increased to RMB2.218 billion with the annual growth rate of 125.8% and the annual growth rate of electricity sales of 121.8%, which mainly benefited from the abundant water inflow in Fujian Province. However, the revenue from the coal-fired power business dropped to RMB1.507 billion, decreased by 48.3% year-on-year, offsetting the business growth of the above-mentioned wind power and hydropower businesses. In general, driven by the significant operating profit growth of the wind power and hydropower segments, the Company realized the profit attributable to shareholders amounting to RMB1.446 billion, increased by 23.5% year-on-year. The EPS was RMB16.51 cents, representing a year-on-year increase of 20.9%, in line with market expectations.

Substantial Growth in Wind Power Installed Capacity

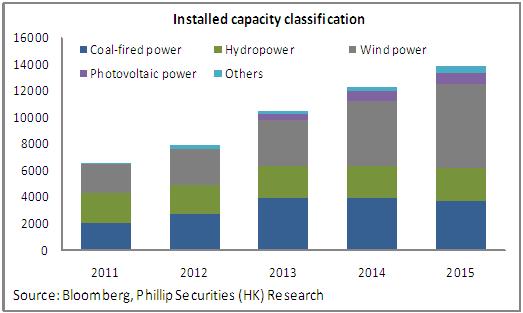

During the first half of the year, the consolidated installed capacity newly put into operation amounted to 652.9MW (consisting of 597.6MW in wind power, 47.3MW in photovoltaic power and 8MW in natural gas-fired power). The power capacity under construction was 1,196.6MW (consisting of 688.5MW in wind power, 100MW in hydropower and 408.1MW in natural gas-fired power). As at the end of the interim period, the Company's total consolidated installed capacity amounted to 14,490.1MW (consisting of 48.4% in wind power, 17.3% in hydropower, 24.8% in coal-fired power and 5.8% in solar energy), representing a year-on-year increase of 15.2% mainly due to the significant increase by 40.4% of the wind power installed capacity.

During the reporting period, the total power generation was 20,900,000MWh, representing a year-on-year increase of 13.8%. The wind power generation was increased by 32%, equivalent to 30.6% of the total power generation. The hydropower generation was increased by 121%, equivalent to 38% of the total power generation. The coal-fired power generation dropped by 43%, equivalent to 23% of the total power generation while the solar energy power generation was increased by 18.8%, equivalent to the total power generation of 2.66%. At present, the Company is dedicated itself to developing new energy projects. The Company acquired the wind power project of Concord New Energy Group in May and the solar energy power generation project of the Oriental Industrial New Energy in September in order to further improve the power generation proportion of clean energy. The Company has abundant cash on hand for acquisition of high-quality projects to accelerate the development of new energy projects.

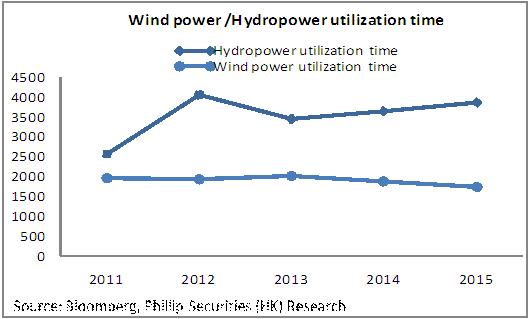

Doubled Hydropower Utilization Time

During the reporting period, the hydropower business had comparatively satisfactory performance. The average hydropower utilization time was 3,172 hours, representing a year-on-year increase of 1,705.4 hours, increased by 116.3%. The hydropower utilization time was expected to maintain the exceptional growth rate in the second half of the year. The average coal-fired power utilization time was 1,337 hours mainly due to the significant power consumption in July and August. The annual coal-fired power utilization time was expected to be over 3,000 hours. The average wind power utilization time was 936 hours, dropping by 55 hours compared to that in the same period of the previous year. It was expected that the annual wind power utilization time would be 1,800 hours. Benefited from the policy of guaranteed acquisition of the annual wind power and photovoltaic power utilization time, the Company's wind power segment was expected to be improved in respect of the utilization time and profitability.

Exceptional Financial Contribution of Wind Power and Hydropower Segments

As to financial issue, during the reporting period, the Company held the cash amounting to RMB2.54 billion on hand, increased by 24.9% compared to that at the end of 2015. The net liabilities ratio was 270.5%, basically in flat compared to that at the end of 2015. The capital expenditure was RMB2.713 billion. The management forecast that the annual capital expenditure would reach RMB10 to 11 billion. Recently, the Company issued the bonds amounting to RMB3 billion at the coupon rate of 2.97%, which served as the repayment for liabilities with interest and the supplement to working capital. It was expected that the financing cost would be further reduced in the future.

Valuation and Rating

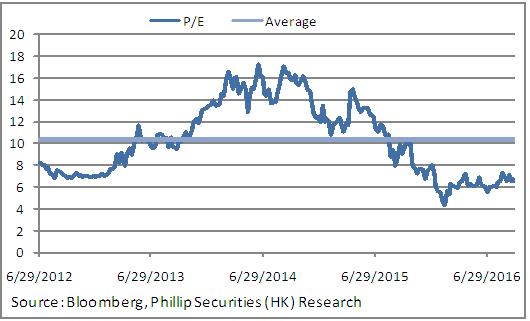

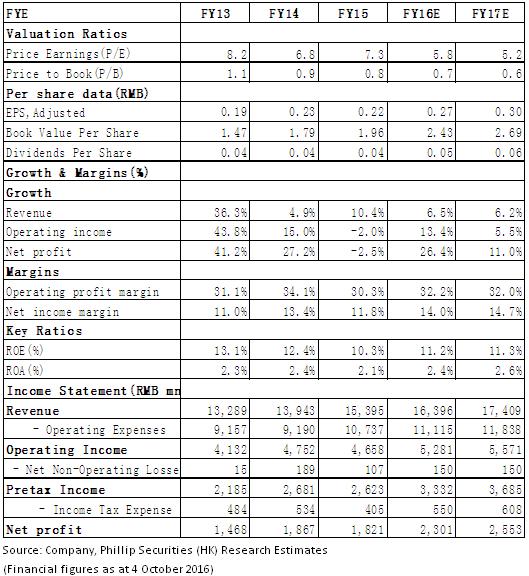

At present, the Company's business structure is transformed from the traditional thermal power to wind power, photoelectricity and hydropower that are characterized in diversification and clean power generation. However, considering the reduction of income from the thermal power segment during the first half of the year, it is believed that the Company's estimated value would be lower than expectation. With the increase in the structural proportion of clean energy, the Company's profitability would be improved and therefore, the estimated value is also expected to rise. Based on the estimated 2016/2017 EPS of 0.27/0.30, we grant the Company the target price of HK$2.51 and the "Buy" rating. (Closing price at 4 October 2016)

Risk Warnings

The implementation of policy falls short of expectations;

There is weak demand of electricity;

Industry competition has increased.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()